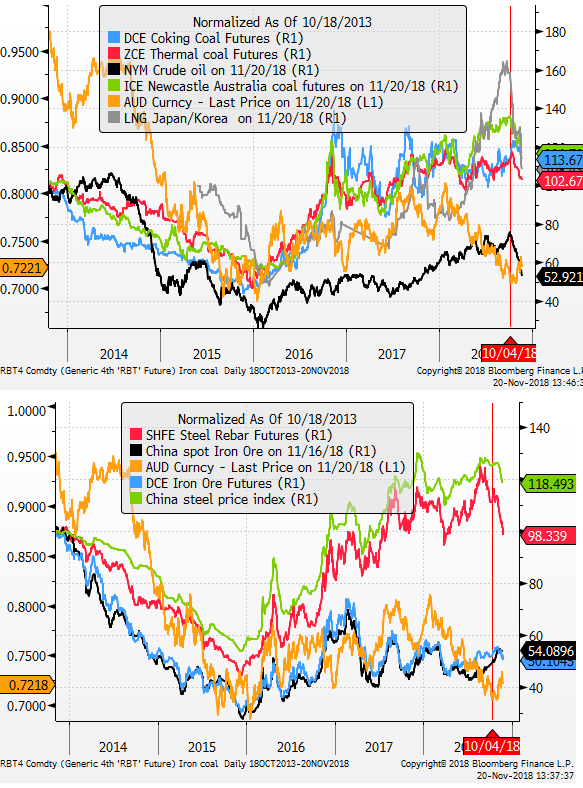

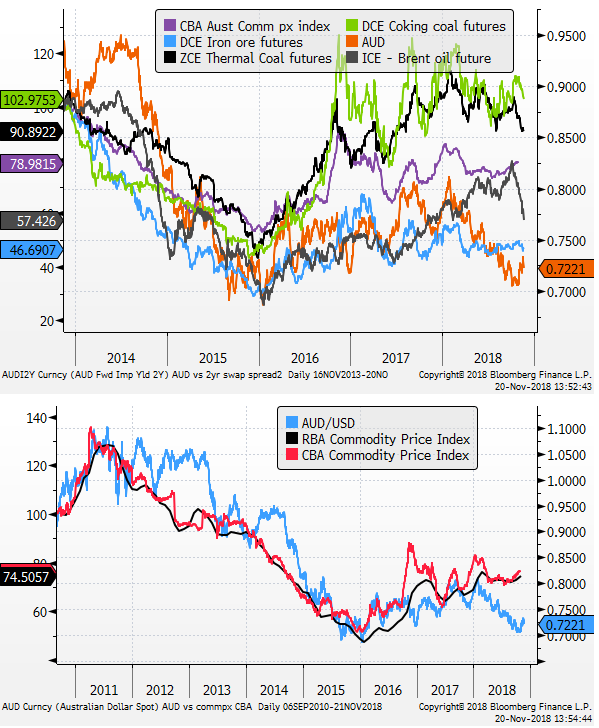

A look at AUD vs commodity prices and other snippets

Tuesday has been characterized by deep falls in commodity prices: oil 7%, copper 1.5%, aluminium 0.7%, iron ore 2.9%, steel futures 4%, coking coal 1.6%, thermal coal 0.1%, LNG futures -1.9%

Even though overall commodity prices might still seem high relative to the AUD, the falls are deep in the energy space, and steel prices have more significantly turned lower. Iron ore prices are relatively stable, but they have also turned lower recently. The AUD is likely to be taking on a higher correlation with oil prices given LNG, and to a lesser extent, thermal coal are highly correlated with oil prices.

US transportation stocks fell 5% on Tuesday? This may indicate some deeper concern over growth in the US economy.

One interesting development is that US rates and yields were little changed today despite weaker equities and commodities.

Yields are generally lower in the recent turmoil in equities and the fall in oil prices that both began around 2-October. But not yet significantly. In fact, the rise in yields initially to new highs for the year contributed to the peaking in US equities in early-October.

The stability in US rates and yields on Tuesday probably helped support the USD. EUR retreated 0.7% after rising to a high earlier in the day since 7-November.

Price action has been whippy in recent weeks and the retreat in EUR today may be technically inspired after its recent resurgence over the last week and more steady US yields on Tuesday.

With the approach of thanksgiving thinned markets, perhaps the market is not ready to embrace new directions or views around Fed policy.

However, we see the market is too wedded to the idea that the Fed will proceed with a rate hike on 19 December, and project hikes into next year.

The risk is that this hike does not occur as US equities lead the fall in global equities, credit spreads widen, and commodity prices slide. 5y5y long-term inflation breakevens have also slipped to recent lows (in several months).

The Fed claimed last week that they are no longer on auto-pilot, and are watching more closely current developments. This would seem to be an opportunity to step back from a hike and assess market and economic conditions. The problem for them is that the market has got so used to them projecting their movements months in advance it can’t contemplate a pause in December.