A more permanent rise in global risk premiums

Commodity markets are leading some recent weakness in global asset markets. Oil and iron ore are sitting near key supports and how they perform around these levels may be important for near term direction in global markets and commodity currencies. Market sentiment remains mixed and asset prices are not clearly out of line with the global economic outlook or policy developments. As such, we are adopting more short term nimble trading strategies at the moment.

Market wants to hear something dovish from the ECB

Ahead of the ECB meeting tonight, the market appears to be expecting some dovish tones in the press conference from Draghi. Most analysts expect further policy accommodation either in December or early next year. The risk is that Draghi chooses to offer few hints on the policy outlook, disappointing dovish expectations and generating modest gains in the EUR. The currency has shown little direction lately, consolidating in the 1.13s after pulling back from a test of key resistance near 1.15 early last week.

Bank of Canada see downside risk to growth

The Bank of Canada maintained a neutral policy outlook, with a hint of an easing bias creeping in. Seeing its role as balancing an inflation targeting objective and financial stability, it said, “The Bank judges that the current stance of monetary policy remains appropriate.”

Previously it said, “The Bank judges that the risks to the outlook for inflation remain within the zone for which the current stance of monetary policy is appropriate.” As such, they were less descriptive on Wednesday and arguably less committed to maintaining policy unchanged.

It noted risks to the outlook related to market volatility at its previous meeting on 9-Sep, but these were more clearly articulated on Wednesday in a lower forecast for GDP that does not see the economy returning to potential for almost two-years. It also said that in the near term, growth was “more likely to be in the lower part of the Bank’s range of estimates.”

While the BoC sees policy as accommodative with strengths in non-resource sectors and exports to the US, the risks are high that inflation undershoots its objective for the foreseeable future. It said, “The Bank judges that the underlying trend in inflation continues to be about 1.5 to 1.7 per cent.” (Below the Bank’s 2% mid-point target)

The Bank of Canada said, “Lower prices for oil and other commodities since the summer have further lowered Canada’s terms of trade and are dampening business investment and exports in the resource sector. This has led to a modest downward revision to the Bank’s growth forecast for 2016 and 2017.”

“The Bank projects real GDP will grow by just over 1 per cent in 2015 before firming to about 2 per cent in 2016 and 2 1/2 per cent in 2017. The complex economic adjustments to the decline in Canada’s terms of trade will continue to play out over the projection horizon. The weaker profile for business investment suggests that, in the near term, growth in potential output is more likely to be in the lower part of the Bank’s range of estimates. Given this judgment about potential output, the Canadian economy can be expected to return to full capacity, and inflation sustainably to target, around mid-2017.”

Governor Poloz was careful to remain balanced on the rates outlook, currency and influence of possible fiscal expansion from the new government in his press conference.

The weaker oil price trend, the downward revision in the Bank’s GDP forecasts, more risk that GDP lands in the lower half of these forecasts in the near term, and a below target core inflation trend has contributed to a weaker CAD.

Commodity market poised at key supports

Both oil and iron ore prices are at key supports and how they perform around these supports may provide an important guide to asset and currency performance in coming weeks. Equites in these sectors have also led recent falls in global markets and reports from China that a state owned steel company is delaying interest payments on its corporate bonds has contributed to downside risks.

Global markets have lifted in October after significant weakness in Q3, but have stalled in the last week. It appears that investors may seek value in times of stress, perceiving global central banks’ policy as still very accommodative, but the ‘search-for-yield’ that has been an enduring feature of global markets since 2009 appears to be more permanently diminished.

It may be the case that we are moving into another bout of weaker global asset market performance. However, we fail to see a clear theme developing. Market sentiment remains mixed and asset prices are not clearly out of line with the global economic outlook or policy developments. As such, we are adopting more short term nimble trading strategies at the moment.

West Texas oil futures contract

Iron ore futures on Dalian Commodity Exchange

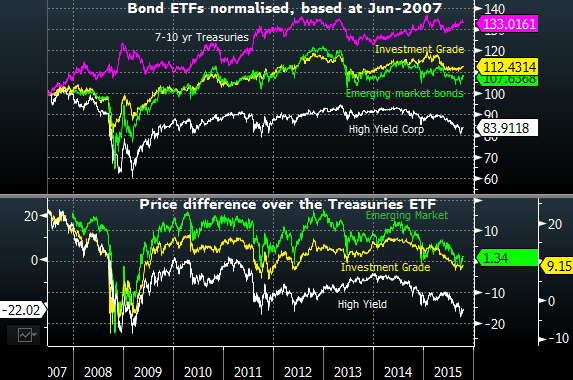

A more permanent rise in global risk premiums

The chart below of Exchange Traded Bond Funds illustrates the diverging nature of different risk segments of global bond markets. In particular high-yield corporate bond prices have been falling since mid-2014 (around the time talk of higher US interest rates and a stronger USD trend took hold).

After a period of reprieve from mid-Dec-2014 up to around June this year, high yield bond prices have fallen more rapidly in the second half of this year, at the same time as US Treasury prices have been rising (yields falling), accentuating the rising spread between the two and thus rising risk premium.

This period is noticeably different from the 2013 taper tantrum. At that time, all bond yields were rising (prices falling) and in fact high yield bonds out-performed US Treasuries. Risk premia for corporate bonds were more stable, and most of the rise in risk premia occurred in emerging market bonds.

However, since around April this year there has been increasing divergence and rising risk premia for all segments of the bond market. This has been most pronounced for high yield corporate bonds, although emerging market bonds have also experienced more significant weakness and investment grade bonds have significantly lagged Treasuries. It appears that the ‘search-for-yield’ that had been an enduring feature of the markets since 2009 has faded on a broad and persistent basis since mid-2014 and more rapidly since mid-2015.

Exchange Trade Bond Fund price performance

Source: Bloomberg

We have seen some bounce back in higher yield bond prices and narrower risk premia since around the end of September, around the time that the Fed decided to push-back its rate hike timing, but at this stage the trend in place for around 16 months has been widening risk premia and many sense that a return to the so-called ‘search-for-yield’ has suffered irreparable damage. Higher risk premia may be here to stay.

The weakness in high yield bonds has been most apparent in the commodity space, undermined by what many see now as persistently lower levels of energy and metals prices undermining fringe companies in this space or those that leveraged up too much. Higher levels of corporate and household debt ratios in emerging markets has also been highlighted by the IMF.

The ECB and Japan ramped up their QE programs in late 2014 and early this year and this may have contributed to a period of narrowing risk premia ealier this year, but the steady progress towards higher US interest rates and a stronger USD appears to have been a more powerful influence on global markets. The presumption is that since the USD is the denominator for much international financing, a rising USD had a more substantial influence on global monetary conditions.

More specifically capital outflow from China, and other emerging markets, in part a response to a stronger USD trend against these currencies, has resulted in declining FX reserves in emerging markets, essentially tightening domestic monetary conditions in these countries.

China has been easing domestic monetary policy to counter the effective tightening that may have arisen from a stronger USD and capital outflow, but its economy is suffering the consequences of its own problems of high domestic debt levels and excess capacity in industrial sectors, as such its monetary easing has had limited capacity to support global asset prices and counter the effective policy tightening in the USA.

In the news

- Samsung Engineering in Korea shares were reported to be down 16% after its earnings announcement this morning in Asia.

- Chinese steel company, Sinosteel failed to make an interest payment, raising concerns over defaults in the corporate bond market (China Defaults Seen Rising After Sinosteel Misses Payment – Bloomberg.com)

Economic news

- New Zealand job ads rose 2.1%m/m in Sep, the largest monthly increase since December-2014. However, it comes after a series of weaker results through the course of this year, falling on average by 0.7%m/m from Jan to Aug.

- The Bank of Canada were somewhat more dovish with a hint of easing bias creeping into a relatively neutral outlook.

On the Radar

- Australia RBA annual report

- Malaysia Foreign Reserves

- Eurozone ECB

- Eurozone Consumer confidence

- UK BoE Jon Cunliffe speech to BBA, international banking conference

- Canada Retail sales

- USA Chicago Fed National Activity Index, Existing Home Sales, Leading index, Kansas City Fed Mfg Index, Markit PMI flash

- China President Xi State visit to the UK

Later this week

- China 23 Oct – Property Prices

- Japan 23 Oct – PMI flash

- USA 22 Oct – Chicago Fed National Activity Index, Existing Home Sales, Leading index, Kansas City Fed Mfg Index, Markit PMI flash

- Canada 23 Oct – CPI

- Eurozone 23 Oct – PMI flash for mfg and services

- Taiwan 23 Oct – Commercial Sales & Industrial Production

- Malaysia 23 Oct – CPI

- South Korea 23 Oct – GDP Q3

- Singapore 23 Oct – CPI

- India 23/30 Oct – Eight infrastructure industries production

Further out

- Australia 28 Oct – CPI

- Australia 3 Nov – RBA rates policy

- Australia 5 Nov – RBA Governor Stevens speaks

- Australia 6 Nov – RBA Statement on Monetary Policy

- Japan 29 Oct – IP

- Japan 30 Oct – Employment, Household spending, CPI, BoJ policy and semiannual outlook report.

- Japan 4 Nov – Japan Post IPO

- China 27 Oct – Industrial profits

- China 28/31 Oct – Leading Index

- China 1 Nov – Manufacturing and Non-Manufacturing PMI

- China 2 Nov – Caixin Mfg PMI

- China 4 Nov – Caixin Services PMI

- USA 26 Oct – New Home Sales

- USA 27 Oct – Durable goods orders

- USA 28 Oct – FOMC

- USA 29 Oct – GDP Q3

- USA 3/19 Nov – Congressional Debt ceiling approach. (WSJ article)

- USA 5 Nov – Fed Vice Chair Fischer speaks at the National Economists Club

- USA 6 Nov – Payrolls

- New Zealand 27 Oct – Trade balance

- New Zealand 29 Oct – RBNZ Official Cash rate (OCR) review

- New Zealand 30 Oct – Building Permits, ANZ business survey, Credit growth

- New Zealand 2 Nov – Treasury monthly economic indicators report

- New Zealand 4 Nov – Labour report Q3

- Eurozone 30 Oct – Unemployment and CPI first estimate

Markets on the Move

- AUD fell sharply in the Asian afternoon session on Wednesday, through the lows earlier in the week around .7250, to around the lows last week near .7200 and remained lower in the offshore session. AUD/NZD was also lower on the day, but less, so and still stronger after the NZD fell on Tuesday on a lower milk price auction

- CAD also fell in the Asian afternoon, and fell much further after the BoC policy announcement and through the American afternoon, more than reversing the modest gains on Tuesday, the day after the Liberal’s decisive election win. CAD has trended lower over the last week with weaker oil prices and USD/CAD rose above highs last week at around 1.3050 to a high since 2-Oct.

- GBP has eased modestly to the low side of its range for the last week, sitting on this support

- EUR/CHF firmed, reversing gains a week ago, rising back to the bottom of its earlier range through much of September and early-October.

- Chinese currency rose in early Asian trading on Thursday, but reversed these gains in the afternoon and ended little changed, relatively stable offshore.

- Asian currencies along with most emerging markets were weaker, much of the moves in the afternoon session. THB fell relatively sharply, extending losses through European trading. USD/THB testing the highs of last week. PHP has traded relatively weakly this week, falling to its low since 5-Oct.

- Oil fell, to be down around $0.6, falling below its low last week to a low since early-October. While weakening over the last week or so, it is yet to break out of its range for the last few months and is now close to a support line joining the low in September and early-October. The oil inventory build number from the EIA was higher than expected.

- Natural Gas futures in the US fell 2.8%, below their lows in September and early-October to a new low since 2012.

- Base metals on the LME were weaker by around 1%, falling over the last week to a low since early-October

- Iron ore fell about 1.5% on Wednesday to its low since late-September. It is testing support resembling a head-and-shoulders neckline and a break of lows in late-September might be a significant blow to confidence.

- 2yr yields were down less than one bp in the US and Eurozone, they fell around 2bp in the UK. Curves flattened with a 4 to 6bp fall in 10 year government yields

- Canadian 2yr government yields fell around 2.5bp in response to softer oil prices and the BoC policy statement that included their quarterly forecast round and a downward revision to its growth outlook. 10 year Canadian yields fell 8.5bp, curve flattening in line with the majors, reversing the rise in long term yields the previous day on the election outcome.

- US equities fell 0.6%, metals and mining sector in the USA fell 2.2%, steel shares fell 2.1% and energy fell 1.0%. Auto and home-builder shares firmed.

- Chinese equities in Shanghai fell 2.9% on Wednesday, falling in the afternoon session appearing to trigger broader risk aversion in commodity and emerging market assets. Although other equities in the region were mixed and Chinese shares in Hong Kong were down only 0.4%.