AUD on the ropes

We had been reluctant to sell the AUD in anticipation of an expansionary Australian Government budget. Sure enough, the government announced an impressive plan to inject up to $75bn over 10 years. This should be an important support for overall capital investment, offsetting the diminishing drag from the mining investment downturn and potentially boosting economic confidence. In fact, business confidence and job ads suggest the economy is gaining momentum. However, the bigger threat to the Australian economy may still be the peaking housing market and high household debt. It is interesting to note that the AUD slumped on weak retail sales and building approvals data. The RBA Governor warned last week that Australians may now be more sensitive to income shocks and more interested in paying down debt than investing in housing or consumption. Households are not particularly confident, and may have retreated from spending after even small out-of-cycle mortgage rate increases in recent months. The AUD continues to trade as a proxy for financial risk in China. The recent slump in iron ore prices and weak Chinese financial markets are likely to have contributed to its recent slide. The USD is more generally firming, perhaps belatedly responding to rising US interest rates. The AUD has little to recommend it to investors, a razor thin yield advantage over the USD and sluggish equity market. Its banks’ share prices have slumped recently, not helped by a levy imposed by the government announced in the May budget. It is possible to see the AUD slump to new cyclical lows.

Infrastructure spending supports the AUD

The Australian government has failed to live up to its forecasts to return to budget surplus since it first slipped into deficit in the wake of the 2008 Global Financial Crisis. It has consistently pushed forward the date of return into surplus, losing some credibility with rating agencies and threats to lose its AAA rating.

Nevertheless, its budget position still stacks up well compared to most other developed nations. The deficit was forecast at 1.6% (underlying cash balance) in the coming fiscal year 2017/18, returning to a small surplus from 2020/21 (in three years).

Net debt is estimated at 19.5% of GDP in 2017/18, rising to a peak of 19.8% in 2018/19, projected to fall to 17.6% in 2020/21.

Net financial worth, including public retirement funds less liabilities, is estimated at -25.1% of GDP in 2017/18, improving to -22.4% in 2020/21.

However, these budget numbers do not include all of the new infrastructure spending that the government has also announced. A significant component of this is effectively off-balance sheet, recognized as a financial asset (loan) to public corporations set up to invest in infrastructure.

Not included in these budget deficit measures are loans to NBN Co (investing in the national broadband network), and new initiatives announced in this year’s budget to finance the second Sydney airport and the proposed Melbourne to Brisbane inland rail project.

The focus of governments globally on budget consolidation has weakened. The G20 has been calling on governments, where fiscal space allows, to expand infrastructure spending.

After several elections in Australia, where the major parties battled each other on fiscal responsibility, the tack has finally shifted, belatedly, but sensibly towards boosting infrastructure spending.

The Government budget talks about spending an additional $A75bn over ten years on infrastructure, 4.3% of current annual GDP of $A1.74tn. This is a significant addition to growth; adding in multiplier effects, it might contribute up to 0.5% annually over a number of years.

This is a large contribution and may be an exaggeration, with the government setting out more of a framework for increasing its support for infrastructure spending over the coming decade.

It said, “The government is establishing a 10-year allocation for funding road and rail investments, recognising that many transformational projects are planned and built over many years. This will deliver $75 billion in transport infrastructure funding and financing from 2017-18 to 2026-27.” Some of this funding relates to projects that are already underway.

More specifically, the budget says, “We have committed to fully finance the Melbourne to Brisbane Inland Rail project by a combination of an additional $8.4 billion equity investment in the Australian Rail Track Corporation and a public-private partnership for the most complex elements of the project.”

“The Government has also committed to establish a new Commonwealth-owned company, WSA Co, to deliver Western Sydney Airport. The Government is making an equity investment of up to $5.3 billion in WSA Co.”

“To develop and advise on financing solutions to deliver key government projects the Government is establishing the Infrastructure and Project Financing Agency on 1 July 2017. The Agency will work with the private sector to identify, develop and assess innovative financing options for investment in major infrastructure projects prior to Government consideration.”

Government spending may help, but investment has been in second gear

The Australian economy is stuck in second gear. It has been transitioning through the downward slide in mining investment on the back-end of a boom since 2013.

It has relied much on rapid housing investment, and a large fall in policy interest rates has fueled a dangerous further boom in household debt and house prices in the major cities. There is little juice left in the household borrowing capacity and now housing activity is peaking, and the economy needs new growth drivers.

The lower AUD has helped support non-mining industries, including solid growth in the service sector. But growth has failed to-date to rise sufficiently to generate a stable well-balanced economy.

The infrastructure spending plans by the government should be viewed as a positive for the Australian economy. The latest measures announced in the budget may take some time to ramp-up to be a significant direct contribution to GDP-growth. Nevertheless, government spending has already stepped into a higher gear over the last year. The latest announcement suggests it will continue to be a significant supportive element for the economy now for the medium term.

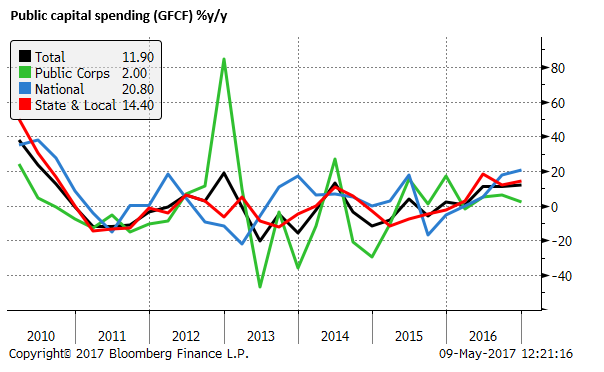

Public investment has already grown strongly over the last year, up 11.9%y/y in Q4-2016, accelerating from negligible levels in 2015, contributing 0.56%pts to annual real GDP growth.

The sustained outlook for stronger government spending on infrastructure helps alleviate the downturn in private sector investment in the mining sector. This is projected to decline for a couple of more years, but at much-diminished pace, with most of the correction from the mining boom that peaked in 2012/13 now complete.

Furthermore, as the RBA noted in its May Statement on Monetary Policy (SoMP), much of the remaining decline [in mining investment] is expected to be in LNG investment, which is import intensive and uses relatively little labour. This suggests that the flow-on effects to the domestic economy are likely to be small.”

In contrast, government spending in airports, rail, and roads, is likely to be relatively labour intensive with a bigger multiplier effect on the rest of the economy.

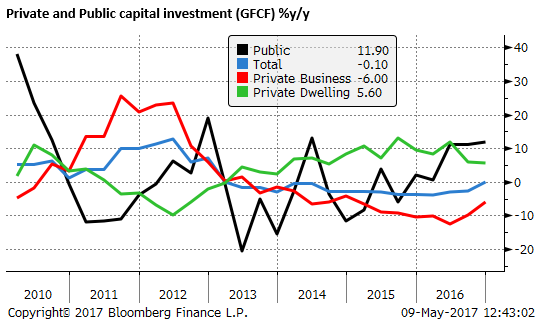

Total capital investment fell 0.1%y/y in Q4-2016, dragged down by private business investment, down 6.0%y/y, but supported by private dwelling investment, up 5.6%y/y, and public investment, as noted already, up sharply by 11.9%y/y. However, as the chart below illustrates, dwelling investment is starting to slow from its peak growth rate in 2015.

The slowing in building approvals suggests the contribution to growth from dwelling investment is expected to decline gradually from mid-2017. (according to the RBA SoMP)

An area where overall capital investment has disappointed has been in the non-mining private business sector. The RBA May SoMP said, “Non-mining business investment increased by around 3½ per cent over 2016, although it has been subdued for several years and remains low as a share of GDP.”

Despite the relatively buoyant surveys of business confidence, the quarterly Capex survey and non-residential building approvals and work-yet-to-be-done suggest non-mining business investment is “unlikely to pick-up significantly over the next year or so” (according to the RBA May SoMP). However, the Capex survey tends to under-estimate non-mining investment, as it does not capture more some of the more dynamic service sector industries.

AUD knocked down by Chinese developments

The AUD appears to have paid little attention to the recent government announcements confirmed in the budget about increased infrastructure spending. It has, however, been knocked down relatively sharply by a renewed slide in iron ore prices.

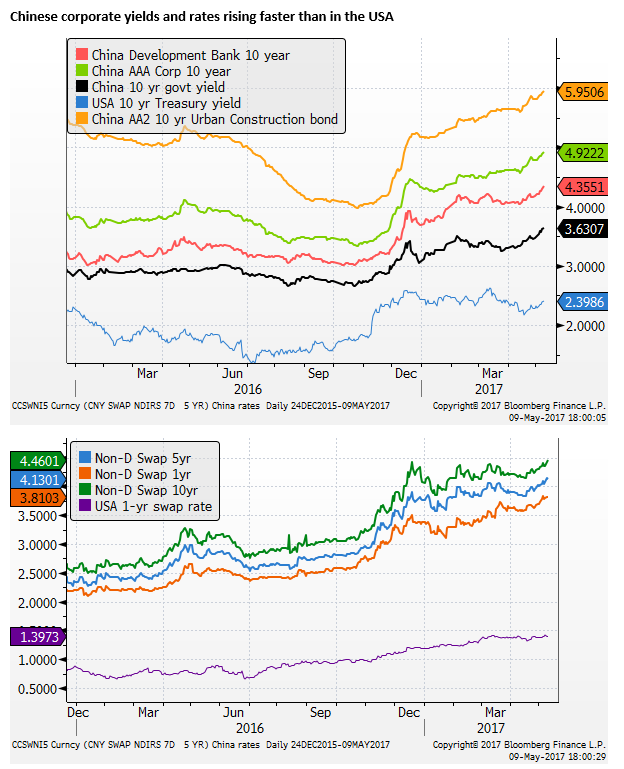

Dove-tailing with the slide in iron ore prices has been a step-back in Chinese PMI data and weak Chinese financial markets (including currency, bonds, and equities), consistent with recent news reports of qualitative efforts to reign in excesses in Chinese credit markets.

The AUD has often traded as a proxy for financial risk in China, and iron ore futures may also reflect some of this risk in China.

AUD responding to household debt fears

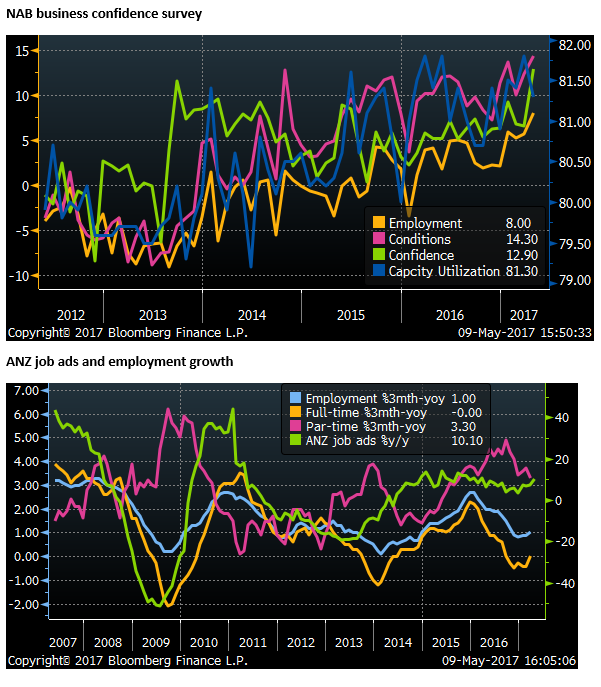

The AUD also fell sharply after weaker than expected building approvals and retail sales data, despite a strong NAB business survey and ANZ job ads.

The focus on building approvals and retail sales suggest the more prevalent fear is a drag that may be arising from the heavy debt load carried by households and a peaking in the housing market.

Since becoming RBA Governor in September last year, Lowe has raised awareness of household debt risks. The RBA has suggested it is willing to live with a longer path back to its 2 to 3% inflation target to avoid further fueling household debt creation. In other words, the RBA fears more harm than good from additional rate cuts from current record lows.

This reluctance to cut rates may have initially supported the AUD, but it also contributed to more regulatory pressure to contain credit growth in recent months.

In a speech last week, Governor Lowe highlighted research that suggests households may already be at a tipping point; they are reluctant to borrow more, even if rates were cut further, suggesting they are near limits on debt, and rate cuts may do little to boost demand. On the other hand, households may be much more sensitive to rate rises. They are already in a mind to consolidate debt, and rate hikes might accelerate this process, dampening consumer spending more significantly than past episodes of rising rates.

Household Debt, Housing Prices and Resilience – RBA.gov.au

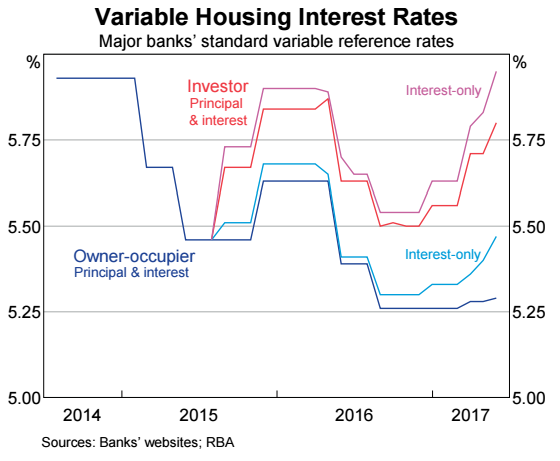

There has already been some increase in mortgage rates faced by households due to measures by regulators designed to force banks to tighten lending standards; mainly for investor loans, particularly interest only loans.

It is possible that at the current high levels of existing household debt, some modest out-of-cycle increases in Australian bank mortgage rates, and evidence that the housing market is around a peak may be contributing to weaker consumer spending.

As the chart above suggests, the retail sales data points to a weak Q1 GDP contribution from household consumption.

The May RBA SoMP noted that households’ perceptions of their personal finances have declined since late 2016. Surveys indicate that households believe that paying off debt is currently a wiser place for saving than investing in real estate.

There is a risk that a peaking in the housing market may shift consumer attention more towards paying down debt than consumption. Already it appears that the wealth effect of higher house prices in the last year has had little positive impact on consumption. Australian’s now fear more than welcome higher house prices; worrying about how their children will afford to buy a house, and sensing high house prices are unsustainable.

The RBA has assumed in its forecasts that household consumption will grow in-line with income over its forecast horizon. There would appear to be a downside risk to this forecast, especially if interest rates start to rise in Australia. A desire to reduce debt faster in response to higher mortgage rates and a weaker housing market may significantly weaken consumer demand.

Since household consumption accounts for 57% of GDP, a weaker trend in consumption may have significant consequences for the overall economy. The RBA may be much more constrained from raising rates over the period ahead. The implications are clearly negative for the AUD compared to most other currencies in a rising global yield environment.

Little to recommend in the AUD

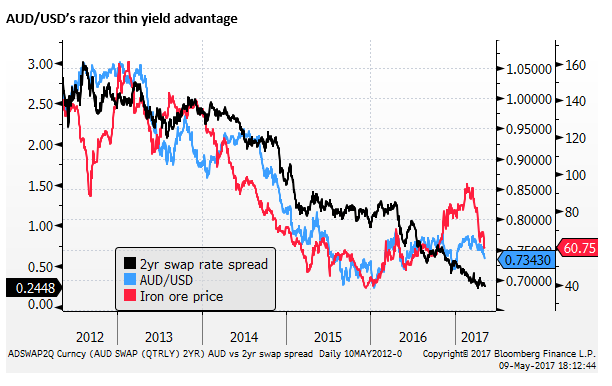

The AUD has been losing yield advantage over the last five years, and this accelerated in the last year as the RBA cut rates in 2016 and the Fed resumed hikes in December last year. The two-year swap rate is a thin 24bp in favour of the AUD.

The FX market has not paid consistent attention to yield spreads in recent years, with flows to equities and higher yield corporate bonds frequently dominating investor attention. The low volatility environment tends to favour higher yielding currencies. Nevertheless, the rate spread in favour of the AUD is so low now it may not be attracting much demand.

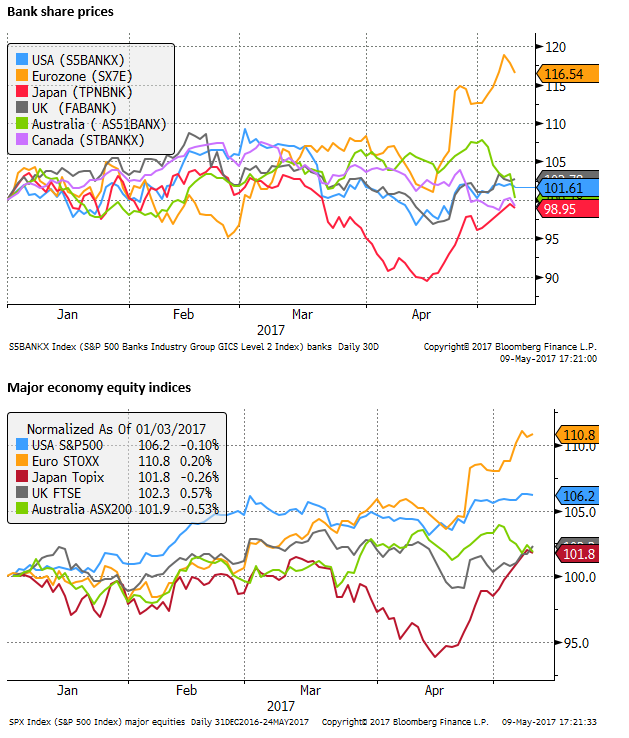

The Australian equity market also has little to recommend it compared to global peers, highly concentrated in the large banks that are under regulatory pressure to slow lending to households, and exhibiting higher risk related to the housing market.

Australian bank share fell on Tuesday anticipating an announcement by the government to place a special levy on these highly profitable institutions in the May budget. From 1 July 2017, banks with $A100bn in liabilities will pay an annualized rate of 0.06% on their liabilities. It is expected to raise $A6.2bn over four years.

The USD has generally regained some strength in recent trading. Yields in the US are creeping up as the market readies for a probably second rate hike by the Fed on 14 June.

We may find that the AUD slips to new lows to reflect its diminished yield advantage, increased risk related to its housing market, related sluggishness in consumer spending, the recent retreat in iron ore prices, higher Chinese financial risk, firming US yields and relatively unattractive Australian bank equities.