BoJ and ECB open door for lower EUR/JPY

In the last two weeks the ECB has taken steps towards more monetary easing and the BoJ has taken a step back. This has resulted in a further fall in the rates spread to a record low for the EUR/JPY. The cross does not look cheap on a longer term perspective and we see a higher risk of a significant fall over the next few months. A short strategy in this pair has the advantage of being less-affected by developments in the US economy that may cause sharp moves in the USD, such as over the payrolls report this week.

Contrasting central bank steps

On Friday, the BoJ held policy unchanged at its major semi-annual forecasting round, suggesting policy is likely to remain stable for the foreseeable future and less responsive to events over the next six months. A week earlier, the ECB said it was likely to expand its monetary easing at its next quarterly forecasting round on 3 December to bolster its forecast for achieving 2% inflation over the medium term. This contrast suggests scope for EUR/JPY to fall further. As a strategy it has the advantage of being little affected by developments in the US that might influence the USD or global risk appetite.

While the BoJ is still conducting an aggressive policy easing which given enough time may generate the inflation it intends, the BoJ actions last week contrast from the actions it took a year ago and the actions that appear to be intended by the ECB next month.

The ECB plans to respond to lower oil prices and weaker emerging market growth. The BoJ has instead lowered its near term inflation and growth forecasts and decided to treat lower oil prices as a transitory effect that it can look through. Kuroda has moved forward the expected date for reaching his inflation target by effectively six months to March 2017. This embodies greater risk that a more sustained period of sub-target inflation reduces inflation expectations, dampens spending and wage growth, raises real interest rates and sends the BoJ off course in pursuit of rising inflation.

The BoJ’s Kuroda may feel he has achieved a rising inflation trend and he does not need to respond with further policy easing at this time, promising to still act further if required. Nevertheless, the events over the last two weeks shifts the path of policy outlooks towards more easing at the ECB and less at the BoJ. This may result in further significant downside in EUR/JPY in the next few months.

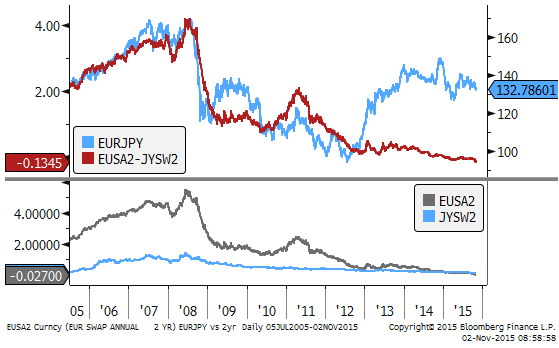

The rates spreads between the two currencies reflect this development. The ECB is expected to further reduce its deposit rate (effective floor rate for money market rates) deeper into negative territory from -0.2%, along with expansion and extention of its asset purchase plan. The BoJ has long targeted cash rates at +0.1%. The 2-year swap rate spread between the two countries fell to a new record low, driven by a significant fall in Eurozone 2yr swap rates now below zero. The chart below shows the 2yr swap rates, the spread and currency pair.

The connection between the rate spread and the currency pair has not been particularly strong since the BoJ established its QE policy in 2013, but with the ECB now ensconced in a similar policy with the added aspect of negative rates, the EUR/JPY does not appear particularly cheap on a longer term scale.

EUR/JPY and 2yr swap rate spread

The decision by Kuroda not to further ease policy at this time leans on his assessment that he can see progress in the domestic economy whereby rising company profits and a tightening labour market have lifted wage growth in the last year and generated higher inflation expectations and price-setting behaviour.

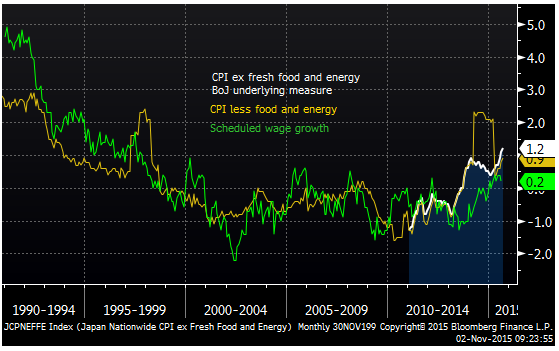

The Bank’s preferred underlying inflation indicator, CPI less fresh food and energy has risen significantly over the last six months from around 0.5%y/y to 1.2%.y/y, a high in over two decades excluding the effect of consumption tax hikes.

This outlook and strategy suggests that the BoJ is unlikely to respond to global developments including a moderately stronger JPY until it sees the outcome from the next annual wage negotiations around Q2 next year. Instead Kuroda plans to rely more on persuading executives to raise wages.

In the BoJ semi-annual Outlook for Economic Activity and Prices, it said this progress on tightening labour markets and higher capital utilization had contributed to higher wages growth last year. But in what appears to be part of its effort to pressure companies to act further it said, “Nevertheless, it should be noted that, given that firms have been seeing record profits and the unemployment rate has declined to the range of 3.0-3.5 percent, the pace of improvement in wages has been somewhat slow.”

Scheduled wage growth, an underlying measure excluding bonuses, rose only 0.2%y/y in August. As the chart below illustrates this measure of wage growth has historically been around the same level as inflation, or above inflation before 1995, suggesting indeed wages growth has been well below what is required to achieve sustainably higher inflation.

Japan underlying inflation and wage growth

Economic news

- Australia manufacturing PMI fell from 52.1 to 50.2 in October. However, the three month average (51.3) and the six month average (50.1) are around their highs since 2010. The employment component fell from 50.7 to 49.2. The new orders component fell from 53.4 to 49.9.

- Australia: CoreLogic RP Data House Price index rose 0.2%m/m in October. From a year ago, prices rose 10.2%y/y, down from 11.1%y/y in Sep. This is still around the high growth rate seen recent years and too early to say there has been any significant cooling in price growth

- Australia Building Approvals rose 2.2%m/m in Sep, more than 1.0% expected, but were revised down to -9.5%m/m in Aug, from -6.9%m/m. Private house approvals fell 1.9%m/m in Sep, after rising 4.1%m/m in August. The trend for this core segment is relatively flat over the last year; they are up 0.8% 3mth/yoy in Sep. Apartment approvals rose 6.1%m/m in Sep after falling 15.7% in Aug. They rose 31.5% 3mth-yoy in Sep, but were up only 0.8% 3m/3m-annualsied. The ABS trend data suggests this volatile component may have peaked around May this year.

- Australia TD Securities Inflation index was flat in October, up 1.8%y/y, down from +1.9%y/y in Sep. The trimmed mean was also flat m/m and up 1.7%y/y, from +1.6%y/y in Sep.

- Japan manufacturing PMI was revised slightly lower from 52.5 to 52.4 in October, still up significantly from 51.0 in Sep, at a high in 12-months.

- China: government sponsored manufacturing PMI was steady at 49.8 in Oct, below 50.0 expected. Remaining around its lows since 2012, just below the growth line of 50 for the last three months.

- China: Markit/Caixin manufacturing PMI rose to 48.3 in Oct, above 47.6 expected, from 47.2 in Sep, the first rise in four months to a high since June.

- China: government sponsored non-manufacturing (services and construction) PMI fell to 53.1 in Oct from 53.4 in Sep, a new low in this series, continuing a falling trend for the last 5 years.

- India: Manufacturing PMI fell to 50.7 in Oct, down from 51.2 in Sep, to a low since 2013.

- South Korea manufacturing PMI was down a little to 49.1 in Oct from 49.2 in Sep. The last two months are up from a recent low of 46.1 in Jun, back to around its March level.

- South Korea export growth slowed to -15.8%y/y, a low since 2009, below -14.5% expected, down from -8.4%y/y in Sep. Import growth was -16.6%y/y, below -13.5%y/y expected, up from -21.8%y/y in Sep. The trade balance was $6.69bn, below $7.13bn, around its record high levels over the last six months.

- South Korea current account balance was $10.6bn in Sep. around a record high.

- Taiwan: manufacturing PMI rose to 47.8 in Oct, a high since May, from 46.9 in Sep. This is the second rise in a row from a low of 46.1 in Aug (a low in data available since 2012).

- Malaysia: manufacturing PMI fell to 48.1 in Oct, from 48.3 in Sep, still up from the low in Aug of 47.2, around the high since May.

- Indonesia manufacturing PMI rose to 47.8 in Oct, from 47.4 in Sep. relatively stable since June, up from a low for the year of 46.4 in Mar.

- Indonesia CPI inflation was down to +6.3%y/y in Oct, below +6.4% expected, from +6.8%y/y in Sep. Core CPI inflation was down a bit to -0.1%, below flat expected, from -0.05% in Sep.

- Thailand CPI inflation rose to -0.8%y/y in Oct, above -1.0% expected, up from -1.1%y/y in Sep. Core CPI inflation was little changed at +0.95% in Oct, as expected.

- USA Employment Cost Index was +0.6%q/q in Q3, as expected, up from +0.2%q/q in Q2. From a year earlier it was steady at 2.0%y/y in Q3, down from 2.6%y/y in Q1, a high since 2008. Current levels are back to the stable average it has been in since 2010.

- USA PCE deflator was 0.2%y/y in Sep, as expected, down from 0.3%y/y in Aug. Core PCE inflation was steady at 1.3%y/y in Sep, below 1.4% expected, around the same levels all year, down from around 1.6%y/y in mid-2014.

- USA personal income rose 0.1%m/m in Sep, below +0.2% expected, but it was revised up to +0.4%m/m from 0.3% in Aug. Personal spending was also up 0.1%m/m in Sep, below +0.2%m/m expected.

- USA University of Michigan Consumer Sentiment was revised down to 90.0 in Oct, below 92.5 expected, from a preliminary 92.1, up from 87.2 in Sep.

- USA University of Michigan inflation expectations in the next 5 to 10 years fell to 2.5%, revised down from a preliminary 2.6%, to touch the previous record low in 2002, down from 2.7% in Sep. It is at the lowest three and six month average levels for this gauge on record. Still above the Fed’s inflation target of 2%, and not much below a long run average of 2.9%, the Fed can probably still claim surveyed measures of inflation expectations are stable, but they are trending down gradually in recent years.

- USA Chicago manufacturing PMI rose to 56.2 in Oct, above 49.5 expected, up from 48.7 in Sep, at a high since January.

- USA manufacturing PMI for Milwaukee rose to 46.7 in Oct, above 44.0 expected, up from 39.4 in Sep, but still below or at other levels since 2013.

- Canada monthly GDP was +0.9%y/y in Aug, below 1.0% expected, up from +0.7%y/y in Jul, but revised down from +0.8%.

- Eurozone CPI first estimate for October was flat in Oct from a year earlier, as expected, up from -0.1%y/y in Sep. The core measure was up to +1.0%y/y in Oct, above 0.9% expected, and +0.9%y/y in Sep.

- Eurozone Unemployment was stronger at 10.8% in Sep, below 11.0 expected, down from 10.9% in Aug, revised down from 11.0%, at a low since 2012.

- Germany Retail sales were +3.4%y/y in Sep, below 4.1% expected, up from 2.1%y/y in Aug, revised down from +2.5% expected.

- UK Consumer confidence fell to 2 in Oct, below 4 expected, from 3 in Sep, still around long run cyclical highs.

- UK Lloyds business barometer rose to 50 in Oct from 42 in Sep, close to its average over the last two years.

On the Radar

- USA Market PMI mfg final, ISM manufacturing, construction spending

- Eurozone PMI mfg final

Later this Week

- Australia 3 Nov – RBA rates policy

- Australia 4 Nov – PMI Services, Trade Balance and Retail Sales

- Australia 5 Nov – RBA Governor Stevens speech, RBA Lowe panel discussion

- Australia 6 Nov – RBA Statement on Monetary Policy, and PMI Construction, RBA Edey speech

- Japan 4 Nov – PMI services, and consumer confidence

- Japan 5 Nov – BoJ 6-7 Oct policy minutes

- China 4 Nov – Caixin Services PMI

- China 7 Nov – FX Reserves

- China 8 Nov – Trade balance

- USA 3 Nov – ISM New York, Factory Orders, and vehicle sales

- USA 3 Nov – Fed’s Williams

- USA 4 Nov – ADP employment, ISM non-mfg, trade balance

- USA 4 Nov – Fed’s Brainard & Harker, Yellen testifies on banking regulation, Fed’s Dudley speaks on the economy

- USA 5 Nov – Fed Vice Chair Fischer speaks at the National Economists Club, Productivity/unit labour costs

- USA 6 Nov – Payrolls

- USA 6 Nov – Consumer credit

- USA 6 Nov – Fed’s Tarullo, Lockhart, Brainard

- USA 7 Nov – Fed’s Williams speaks on economic outlook

- New Zealand 4 Nov – Labour report and wages Q3

- New Zealand 6 Nov – government 3mth financial statements

- Eurozone 3 Nov – ECB’s Draghi speaks in Frankfurt

- Eurozone 4 Nov – PMI services final, PPI

- Eurozone ECB 5 Nov – PMI retailing, Retail sales, EC forecasts

- Canada 4 Nov – Trade balance

- Canada 6 Nov – Labor data

- Germany 5 Nov – Factory orders

- UK 3 Nov – PMI mfg, PMI construction

- UK 4 Nov – PMI services

- UK 5 Nov – BoE inflation Report and policy decision

- South Korea 2 Nov – Current Account, PMI Mfg

- Taiwan 2 Nov – PMI

- Indonesia 2 Nov – PMI and CPI

Further out

- Australia 9 Nov – ANZ job ads

- Australia 10 Nov – NAB Business Confidence, and Housing Finance

- Australia 11 Nov – Westpac Consumer Confidence

- Australia 12 Nov – Employment Report

- Australia 17 Nov – RBA policy minutes

- Australia 18 Nov – Wage Cost Index

- Australia 2 Dec – GDP Q3

- Japan 9 Nov – Labor cash earnings

- Japan 10 Nov – Current Account, and bank lending

- Japan 11 Nov – Machine Tool Orders

- Japan 12 Nov – Machine Orders, and PPI

- Japan 16 Nov – GDP Q3

- Japan 19 Nov – BoJ

- Japan 27 Nov – CPI

- Japan 14 Dec – Tankan

- Japan 18 Dec – BoJ

- China 10 Nov – CPI

- China 11 Nov – Retail sales, IP, Fixed Asset Investment

- China 11/15 Nov – Credit and money supply

- China 18 Nov – Property prices

- USA 9 Nov – Labor Market Conditions Index

- USA 10 Nov – NFIB small business confidence, and import price index

- USA 12 Nov – JOLTS job openings

- USA 13 Nov – Retail Sales, PPI, UoM consumer sentiment and monthly budget statement

- USA 16 Nov – Empire state manufacturing index

- USA 17 Nov – CPI

- USA 18 Nov – Housing starts/Building permits

- USA 18 Nov – FOMC 28 Oct policy minutes

- USA 25 Nov – PCE deflator inflation indicator

- USA 3 Dec – Fed’s Yellen speaks to the Economic Club of Washington

- USA 4 Dec – payrolls

- USA 16 Dec – FOMC

- New Zealand 10 Nov – Retail sales (card spending)

- New Zealand 10/14 Nov – REINZ housing market data

- New Zealand 11 Nov – Financial Stability Report

- New Zealand 12 Nov – PMI mfg and ANZ consumer confidence

- New Zealand 16 Nov – PMI services, and retail sales Q3

- New Zealand 17 Nov – 2yr inflation expectations

- New Zealand 10 Dec – RBNZ MPS and policy announcement

- New Zealand 17 Dec – GDP Q3

- Eurozone 11 Nov – ECB President Draghi speaks at BoE event in London

- Eurozone 12 Nov – Industrial production

- Eurozone 13 Nov – GDP Q3, and trade balance

- Eurozone 16 Nov – CPI final

- Eurozone 19 Nov – ECB account of the monetary policy meeting

- Eurozone 2 Dec – CPI first estimate and unemployment

- Eurozone 3 Dec – ECB meeting

- UK 11 Nov – employment data

- UK 7 Nov – CPI

- UK 10 Dec – BoE policy decision