BoJ may be charging up the defibrillator

BoJ’s Kuroda has changed policy only twice since becoming governor in March 2013, both were designed to deliver shock and awe, the second with entirely no warning, exactly this time one year ago. The ECB argued last week that further policy easing is likely to be required to get its forecasts for inflation over the medium term back towards target; the same appears true in Japan. As such, Kuroda may feel compelled to action to stay true to his firmly held objective of raising inflation expectations.

Compelled by the forecasts

After the surprise policy announcements last week by the ECB and China, the focus this week is on how the Fed and BoJ respond at their policy announcements on Wednesday and Friday respectively. The Fed only release a short statement with no press conference, but the BoJ conducts its major semi-annual forecasting round with projections for its inflation target for the next two fiscal years. As such, the risk is high that this forecasting process compels the BoJ to step up its easing measures, along the lines that the ECB suggested was likely at its next meeting in December.

Shock value

BoJ members have given no hints that a policy easing is imminent. But the BoJ is certainly not averse to surprising the market. Kuroda wrote the play-book on shocking the market, delivering two shock and awe policy moves in April 2013 and one year ago on 30 October 2014. In particular the 2014 policy decision was almost totally unexpected. As such, we should not expect any warnings in the media or press with regards to the meeting on Friday.

The ECB’s Draghi appears to have adopted a similar style of shocking the market from time-to-time. Arguably this is designed to get more bang out of policy easing measures akin to giving the patient a hit with a defibrillator.

Don’t be fooled by upbeat comments

Part of the messaging adopted by Kuroda is designed to lift inflation expectations. In the past he has said he faces a different task than his US and European counterparts. He notes that they have inflation expectations anchored at higher levels close to their 2% targets. However, he has the task of deliberately raising inflation expectations in the community. This has always been the point of his inflation targeting mantra “to achieve a price stability target of 2 percent at the earliest possible time, with a time horizon of about two years.”

At various times the market has speculated that he may soften this line, and accept a slower path back to inflation. However, Kuroda will be reluctant to appear to give-up for fear of pandering to the defeatist undertone in the community that low inflation, even deflation, is the natural state in Japan.

To this end he often sounds quite up-beat on the prospects for higher inflation, making some think this means he is unlikely to change policy. However, the communication is less about policy signalling and more about convincing society that inflation is coming and here to stay. The aim is to raise inflation expectations and in turn influence Japanese behaviour to invest and spend more while rates are currently historically low.

Progress on inflation

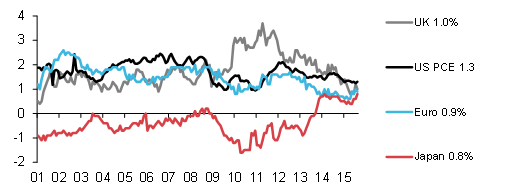

Kuroda can point to progress in lifting underlying inflation; excluding food and energy it rose 0.8%y/y in August, a high since 1995 excluding the impacts of consumption tax hikes like that in April 2014. The market expects this to tick up to 0.9%y/y in Sep when reported on Friday just ahead of the BoJ policy announcements. The chart below illustrates how much Japan has closed the inflation gap with the other major economies (US Core PCE 1.3%, UK core 1.0%, Euro core 0.9%)

Core inflation %y/y (excluding food and energy

source Bloomberg

Headline inflation in Japan was last at 0.2%y/y and is expected to fall to flat in data for September on Friday, but this is hardly any different than the other major economies where both the UK and the Eurozone headline numbers are -0.1% for Sep and the US is plus 0.3% for August. The BoJ has historically used the CPI less fresh food (including energy) as its underlying inflation measure and this is forecast to fall -0.2%y/y in Sep.

Oil prices deflationary or transitory?

A key question is whether the BoJ decides to treat the weaker oil price as a transitory influence on inflation rather than something it should react to and further ease policy to counter its disinflationary effects. In some of his recent commentary, Kuroda has alluded to rising inflation excluding energy as a sign that his policies are working. Some might conclude, therefore, that he is unlikely to ease policy.

However, as discussed, these comments are more about shoring up inflation expectations. The ECB’s Draghi at his press conference last week explicitly linked the current low oil price with medium term inflation expectations and highlighted the risk that this posed to undershooting his inflation target.

Kuroda himself made this same link to explain his surprise policy easing in October 2014. He might again argue that to bolster expectations in the face of lower oil prices, and reduce the risk that future inflation outcomes fail to reach their targets, he may decide to again ease policy further this week, just as Draghi has signalled and Kuroda, himself, did a year ago.

Draghi spoke positively about the momentum in the domestic Eurozone economy, and stable inflation expectations since the previous meeting. He nonetheless signalled that the staff forecasts to be prepared for the December meeting are unlikely to project inflation high enough soon enough, with risks to the outlook emanating from weaker emerging market growth and a higher EUR exchange rate. All the same arguments easily apply to Japan, and thus Kuroda, if he wants to appear as aggressive in pursuing his inflation target, then he may feel pressured to take further policy easing measures.

Lower rates would help generate shock value

If Kuroda wanted to shock the market, he might also consider cutting the target cash rate below 0.10%. He has said in the past that this is not under consideration. However, Draghi until last week said the current negative 0.2% deposit rate was essentially the floor. He jettisoned this view last week, saying that the bank was now open to the idea of cutting rates further after viewing the experience of other central banks. The Eurozone has achieved lower rates than Japan with its policy and thus currently has an easier policy setting. Kuroda could decide to make a change at any time on the rates policy, including this Friday.

BoJ may prefer some additional currency weakness

Draghi noted that the EUR exchange rate had appreciated in effective terms by around 6% from earlier in the year, and thus was contributing to a lower inflation outlook. The BoJ’s nominal effective exchange rate is up only around half as much since the first half of the year, and may not be as big a concern for the BoJ. Nevertheless the BoJ might like to see it a bit weaker and cutting the interest rates would certainly help.

Labour market tight, but wages growth sluggish

The one argument that may be used to prevent a policy easing is the further tightening in the labour market. The jobs-to-applicants ratio is at a high since 1992, rising steadily over the last year. The unemployment rate has been relatively stable since March, currently at 3.4%, a low since 1997, suggesting that the labour market is one of the tightest in the world.

On the other hand this is not yet translating into convincing increases in wages. Scheduled cash earnings (underlying wages) rose 0.2%y/y in August. They have been rising from year earlier levels since January, and thus Kuroda can claim progress on raising inflation. But it he could afford to push harder for wage growth.

Market views are mixed

The latest survey by Bloomberg had 15 of 36 economist forecasting additional stimulus at the meeting this week. After last week’s ECB and China policy announcements, the odds are probably leaning further in favour of policy action by the BoJ. If they decide to move, it may well be a decisive step. Kuroda has made two policy changes since becoming governor in March 2013, both large incremental moves. This alone raises the odds that he decides to cut rates. Few appear to be expecting a rate cut, and it would have additional shock-value. Most expect an expansion in the monthly purchases of government bonds currently designed to grow the money base by 80tn per month.

The JPY is thus poised to move either way this week on the policy decision. USD/JPY is up on the higher probability of action, currently sitting around the high side of its range since August.

In the news

- PBOC cut interest rates and the reserve-requirement ratio. The one-year benchmark lending rate was cut 25bp to 4.35% and one-year deposit rate was cut by the same amount to 1.5%. The RRR was cut 50bp. However, it also removed the ceiling on banks’ deposit rates, allowing banks to pay higher rates to attract funding. Presumably the central bank aims to keep banks well funded through its RRR cut and other term repo operations to keep a lid on deposit rates.

- Chinese yuan expected to be included in SDR at an announcement expected in November: International Monetary Fund staff are set to give the all-clear for China’s yuan to be included in the lender’s benchmark currency basket, laying the groundwork for a favorable decision by policymakers, people familiar with the discussions said on Sunday. (IMF set for green light on China’s yuan joining currency basket-sources – Reuters.com)

- China has formally requested to join the European Bank for Reconstruction and Development (ERBD). This may open channels for investment and is seen as part of its New Silk Road” or “One Belt, One Road” project (China applies to join EBRD to build ties with Europe – FT.com).

- Shanghai listed Yantai Xinchao Industry co. said it was acquiring oil properties in West Texas from two US companies for $1.3bn. Bankers and “industry insiders” say a host of Chinese firms have expressed interest to buy up energy assets in North America (According to a Wall Street Journal article – Chinese Property Developer Snaps Up Texas Oil Fields – WSJ.com)

What They Said

- The MD of Australian listed company Oil Search Peter Botten said in an interview over the weekend that Australian government revenue from its large gas projects, “will be a very good revenue, but a lot less than originally thought”… “Even 18 months ago.” He noted that “Gas pricing has gone from $US15 MBTU (one million British thermal units) down to $7, so 50 per cent less I would suggest.” He noted that around a quarter of the jobs in the Australian oil and gas sector have been lost over the last six months

- Former Fed Chair Bernanke said, “The tough decision that she [Yellen] and her colleagues have to make is, is there enough domestic momentum to keep us moving forward despite these drags from abroad.” He said the US economy has shown evidence that it is “pretty strong”, citing housing, auto sales and consumer spending. (Bernanke Says Yellen’s Tough Decision Turns on Global Headwinds – Bloomberg.com).

- SNB Vice President Fritz Zurbruegg said, “At the current level the franc remains markedly over-valued.” He said the of the SNB’s December policy meeting, “Of course that’ll include an assessment of the ECB’s monetary policy measures and their possible effects on Switzerland.”

- Chinese President Li said his government will not “defend to the death” its goal of 7% growth. ” We have never said that we should defend to the death any goal, but that the economy should operate within a reasonable range.”

- Yi Gang, Vice-governor of the PBOC said China would be able to keep growth at 6-7% for the next three to five years, a rate he called “very normal.” The comments come ahead of the Chinese Communist Party conference that will discuss the next 5-year plan (Chinese premier Li Keqiang plays down 7% economic growth target – FT.com)

Economic news

- Eurozone PMI flash for manufacturing was unchanged at 52.0 in October, above 51.7 expected, down slightly from the high for the year in June of 52.5, largely stable since March.

- Eurozone PMI flash for services rose from 53.7 to 54.2 in October, above 53.5 expected; remaining relatively stable around 54.0 since March.

- Canada CPI headline inflation fell from 1.3%y/y to 1.0%y/y in Sep, below 1.1% expected. Core inflation was unchanged at 2.1%y/y, below 2.2% expected.

- US Markit PMI flash manufacturing reading rose from 53.1 to 54.0 in October, stronger than 52.7 expected, up from the low of 53.0 two months ago since Oct-2013 to a high since May this year, suggesting the sector may be stabilizing after sliding over much of the last year, dragged down by the weak energy sector and strong USD.

- Japan PMI manufacturing rose from 51.0 to 52.5 in October flash reading, above 50.4 expected. The highest since March-2014.

Markets on the Move

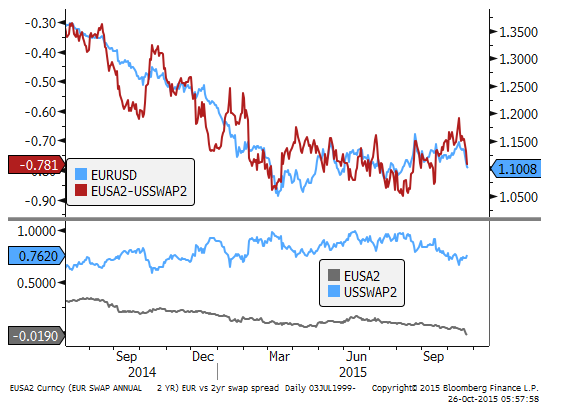

- US 2 year swap rates rose 3.5bp on Friday to 0.762%, to a high since 9-Oct (2 week high). 10 year government yields rose 6bp.

- Eurozone 2 year swap rate slipped a further 1.1bp to a new record low of a negative -0.019%. 10 year German government yields rose 1.6bp to 0.512%.

EUR/USD vs. 2yr swap rate spread

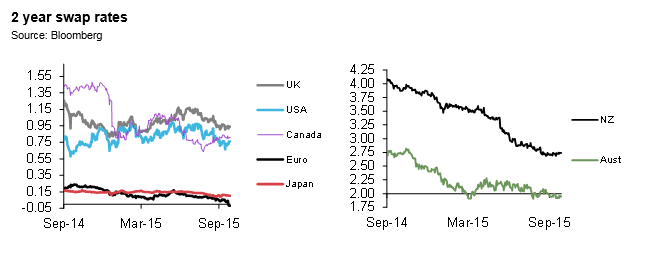

- Canadian 2yr swap rates rose 0.8bp, UK 2yr swap rates rose 2.3bp. Japanese 2yr swap rates fell 0.4bp to 0.104%. Australian 2yr swap rates are up around 1.5bp

- USD/JPY rose above its previous highs in Sep, to its high since 31-August. EUR/USD fell below its previous lows in Sep, to a low since 11-Aug. Key support is around 1.0820/40 (lows in May, July and Aug).

- EUR/GBP fell below the low in Sep to a low since 21-Aug. GBP/USD fell to a low since 14 October.

- AUD rose to almost 0.7300 in Asia and retreated to the low 0.7200s in early American trading on Friday to be little changed for the last few trading days. CAD fell (USD/CAD rose) reversing modest gains in Asia and early Europe to a high since 2-October. Falls coincided with weaker oil and copper prices. And slightly lower than expected Canadian CPI data.

- US stocks rose 1.1%, back in the range that prevailed from Feb to Aug before the sharp fall from 20 to 24 August. Info Tech stocks rose 3.0% on Friday to a new high for the year, more than fully reversing the August drop. The energy sector fell 0.2% to be little changed over the last two weeks.

- Oil fell to a new low since 2-Oct, precariously trading on a slightly rising trend support line since early-Sep.

- Natural Gas futures trading on NYME fell 4.2% on Friday and are lower this morning in Asia to a low since 2012. Warmer than usual weather has delayed the start of winter demand.

On the Radar

- UK BBA loans for house purchases, CBI industrial trends survey

- ECB’s Mersch speech “The Challenges of Innovation.”

- Germany IFO

- USA New Home Sales

- China 26/29 Oct – 5th Plenary Session of the 18th Central Committee of the Communist Party of China. The 13th Five year plan (2016-20) will be top of the economic agenda (some focus on if the growth target is revised down).

- Thailand Trade balance

- Indonesia PM Joko Widodo visits the US

Later this week

- Australia 28 Oct – CPI

- Australia 29 Oct – New home sales

- Australia 30 Oct – Credit growth

- Japan 27 Oct – PPI services

- Japan 28 Oct – Retail sales

- Japan 29 Oct – IP

- Japan 30 Oct – Employment, Household spending, CPI

- Japan 30 Oct – BoJ policy and semiannual outlook/Kuroda press conference

- China 27 Oct – Industrial profits

- China 28 Oct – Consumer confidence

- China 28/31 Oct – Leading Index

- China 1 Nov – Government sponsored PMI mfg and non-mfg

- (businessinsider.sg)

- USA 27 Oct – Durable goods orders, CB Consumer confidence, S&P/CS house price index, Markit PMI services, Richmond Fed Mfg index.

- USA 28 Oct – trade balance advanced

- USA 28 Oct – FOMC

- USA 29 Oct – GDP Q3

- USA 30 Oct – Employment Cost Index

- USA 30 Oct – Personal income/expenditure, PCE inflation data

- USA 30 Oct – ISM Milwaukee, Chicago PMI, UoM Consumer sentiment final

- New Zealand 27 Oct – Trade balance

- New Zealand 29 Oct – RBNZ Official Cash rate (OCR) review

- New Zealand 30 Oct – Building Permits, ANZ business survey, Credit growth

- Canada 27 Oct – BoC Deputy Governor Timothy Lane speech

- Canada 29/30 Oct – CFIB Business barometer

- Canada 30 Oct – monthly GDP

- Eurozone 27 Oct – Money supply and credit growth

- Germany 27 Oct – Retail sales

- Eurozone 28 Oct – ECB’s Coeure, Praet and Constancio speak

- Eurozone 29 Oct – EC surveys on business, services and consumers

- Germany 29 Oct – CPI and unemployment

- Eurozone 30 Oct – CPI first estimate for October

- Eurozone 30 Oct – Unemployment

- UK 27 Oct – GDP Q3, index of services

- UK 29 Oct – Nationwide house price index, money supply & credit growth, CPI retail sales monitor

- UK 30 Oct – Consumer confidence, Lloyds’ business barometer

- Singapore 26 Oct – IP

- Singapore 30 Oct – Money supply

- Thailand 30 Oct – Current Account

- Thailand 27/30 Oct – Manufacturing production and capacity utilization

- South Korea 27 Oct – consumer confidence

- South Korea 28 Oct – retail sales

- South Korea 30 Oct – business surveys and leading index

- South Korea 1 Nov – Trade balance

- Philippines 27 Oct – Trade balance

- Philippines 30 Oct – Money supply

- Taiwan 27 Oct – Monitor Indicator

- Taiwan 30 Oct – GDP Q3

- Taiwan 1 Nov – PMI Mfg

- India 30 Oct – Fiscal deficit

- Malaysia 30 Oct – Money Supply

Further out

- Australia 3 Nov – RBA rates policy

- Australia 5 Nov – RBA Governor Stevens speaks

- Australia 6 Nov – RBA Statement on Monetary Policy

- Australia 2 Dec – GDP Q3

- Japan 6 Nov – Labor cash earnings

- Japan 16 Nov – GDP Q3

- Japan 19 Nov – BoJ

- Japan 27 Nov – CPI

- Japan 14 Dec – Tankan

- Japan 18 Dec – BoJ

- China 2 Nov – Caixin Mfg PMI

- China 4 Nov – Caixin Services PMI

- China 8 Nov – Trade balance

- China 10/11 Nov – CPI, Credit, Retail sales, IP, Fixed Asset Investment

- USA 2 Nov – Market PMI mfg final, ISM manufacturing, construction spending

- USA 4 Oct – ADP employment, ISM non-mfg

- USA 5 Nov – Fed Vice Chair Fischer speaks at the National Economists Club

- USA 6 Nov – Payrolls

- USA 3/19 Nov – Congressional Debt ceiling approach. (WSJ article)

- USA 25 Nov – PCE deflator inflation indicator

- USA 3 Dec – Fed’s Yellen speaks to the Economic Club of Washington

- USA 4 Dec – payrolls

- USA 16 Dec – FOMC

- New Zealand 2 Nov – Treasury monthly economic indicators report

- New Zealand 4 Nov – Labour report Q3

- New Zealand 17 Dec – GDP Q3

- Canada 4 Nov – Trade balance

- Canada 6 Nov – Labor data

- Germany 5 Nov – Factory orders

- Eurozone 13 Nov – GDP Q3

- Eurozone 2 Dec – CPI first estimate and unemployment

- Eurozone 3 Dec – ECB meeting

- UK 3 Nov – PMI mfg, PMI construction

- UK 4 Nov – PMI services

- UK 5 Nov – BoE inflation Report and policy decision

- UK 11 Nov – employment data

- UK 7 Nov – CPI

- UK 10 Dec – BoE policy decision

- South Korea 2 Nov – Current Account, PMI Mfg

- Taiwan 2 Nov – PMI

- Indonesia 2 Nov – PMI and CPI