BoJ Reboot may reinforce rise in bond yields and USD

A longer term yield rebound has driven the USD higher in recent weeks, with less focus on short-term rates. The rise in yields reflects a reversal from irrationally low levels and perverse strength in currencies with NIRP. The BoJ has been forced to reassess its policy approach that was no longer working. It does not make sense to keep buying medium and long-term bonds at negative yields and it appears to have created a perverse strengthening in the JPY by encouraging more savings (increasing the Japanese current account surplus) and weakening inflation expectations (raising real yields in Japan). We may find out this week that the BoJ rejects the idea of buying bonds at negative yields, spilling over to a potential policy re-think at the ECB, and triggers a further rise in global yields. The BoJ may further aim to increase the cost of hedging back to JPY by lowering its NIRP. We think a steeper yield curve and more negative cash rates may shift the JPY back to a weaker trend. Some fallout to global asset markets is expected, but we don’t see global economic confidence as being sapped by weaker asset prices, and in fact may make way for a more healthy recovery in global equity markets before long. Difficult Brexit negotiation outlook weighs on GBP.

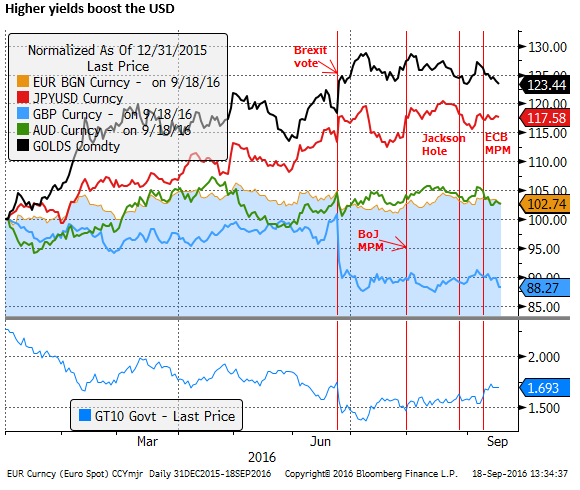

Longer-term yields driving currencies

Longer-term yields rather than short-term rates have been the more important driver of currencies recently, in part through their influence on broader asset markets, triggering some reversal of the search for yield that boosted equities, corporate bonds and emerging markets.

Higher yields appear to have caused the USD to strengthen broadly, although less obviously against the JPY that has been more mixed. Bond yields started to rise noticeably after the ECB policy meeting on 8 September.

Higher yields boost the USD

The ECB disappointed expectations that it might announce a lengthening in its QE program and show more urgency to deal with some renewed weakening in its inflation outlook. The meeting was segued by the BoJ meeting on 29 July where the BoJ failed to meet expectations of more bond purchases and instead singled a major review of its monetary policy. Together the two meetings suggested there was a reluctance to expand QE and concern over the negative consequences of low and negative bond yields and possible dysfunction in markets where the central bank had become the dominant influence.

A correction in irrational bond markets

The extreme lows in Japanese and German bond markets had spilled over to most global government bond markets and in turn to higher yield markets further up the food-chain. As such lower expectations about these central banks’ future demand for their government bond markets spilled over to higher bond yields globally.

Several global bond market luminaries, including Bill Gross and Jeffery Gundlach, had warned that yields were unsustainable low. Gross described negatively yielding bonds as liabilities, not assets, and said that central banks had effectively flipped assets from the left to the right-side of the global balance sheet. I am not sure exactly what that means but it draws from a sense of irrationality in negative yielding bonds. It is hard to understand why any investor would buy a long-term asset they will lose money on if they hold to maturity.

Bill Gross Investment Outlook – Janus.com

Gundlach Says Starvation for Yield Creating ‘Mass Psychosis’ – Bloomberg.com

Global bond yields to rise as investors see fiscal expansion on horizon – Gundlach – Reuters.com

It seems that yields fell to irrationally low levels because major segments of the financial industry, pension managers and insurance companies, were set-up to buy long-term assets at any price. But these industries do not seem viable if a negative yield environment were to persist.

BoJ Governor Kuroda, in his speech on 5 September, said, “As long-term and super-long-term rates have declined significantly since the introduction of the negative interest rate policy, the rates of return on investments of insurance and pension products are expected to decline. Under these circumstances, the sales of some saving-type, products are suspended. Some business firms have revised down their profit forecasts due in part to the increase in the net present value of retirement benefit obligations. Although direct impacts of these developments on the entire economy may not be substantial, we should take account of the possibility that such developments can affect people’s confidence by causing concerns over the sustainability of the financial function in a broad sense, thereby negatively affecting economic activity.”

Gold weaker as bond yields rise

We had argued that the price of gold should rise as negative yielding bonds forced investors into alternative assets that were still safe but at least not negative yielding. We were surprised that gold did not rise much further this year. But it is less surprising that as yields have risen recently, gold has been one of the weaker forms of currency, slipping against a recovering USD more than other major currencies.

Irrational currency response to NIRP

Part of the negative yield perversion sprung from gains in the JPY and relative strength in the EUR despite negative yields. There is a degree of irrationality in a rising currency when yields are negative. NIRP has cost Japanese investors to hedge overseas investment, and that cost has risen as Japanese demand for hedging foreign currencies has increased, tending to widen the JPY/USD cross-currency basis and increase rates to borrow USD and other currencies in their domestic money markets.

As bond yields fell abroad and the cost of hedging increased, the opportunity for Japanese investors to make any profit on foreign investment diminished.

The only reason to keep paying these hedging costs from a Japanese perspective was because they thought the risk of a rising JPY exchange was too high to ignore. The risk of a rising JPY may have increased because of several factors:

A view that JPY had become cheap and thus might revert to more normal levels,

A view that the BoJ had run out of scope to further ease policy, and may have given up to a degree is willingness to achieve higher inflation,

A view that the government would not intervene to stabilize the currency, and

A recovery in the Japanese current account surplus to previous highs.

Lower energy import prices boosted the current account balance. Lower inflation expectations and sharply lower Japanese bond yields increased the desire to save for future spending, especially in Japan’s situation of more aged demographics, lowering current consumer demand and further widening the current account surplus.

As such, while low yields may appear to have made JPY assets less attractive, potentially weakening the JPY, they had the opposite effect of encouraging, even more, savings, undermining inflation expectations, tending to boost the current account surplus and real rates of return in Japan, supporting the JPY.

A breaking point in the strong JPY dynamics

Perhaps the effects of the strong JPY dynamic on international markets reached a limit. Global bond yields may have fallen and the cost of hedging foreign currencies back to JPY risen to such a degree that Japanese institutions no longer found a way to profitably invest offshore. As such, the dampening effects on their earnings from negative or extremely low yields in Japan mattered more. And the pressure intensified on the BoJ and the government to change course.

The BoJ has been made to see that low and negative yields in Japan, while lowering the cost of borrowing and encouraging some investment, was, more importantly, undermining Japanese financial sector profitability, undermining economic confidence and clearly not having the desired effect of weakening the JPY. In fact, in a way, it was boosting the JPY and being counter-productive.

It is not clear that the BoJ has the answers to its conundrum, but it at least recognized that its policy was not working and it needed to do a review; as it announced on 29 July.

BoJ policy options

The media and market commentary suggest that the BoJ is not in one mind as to what it should now do to restore the effectiveness of its policy. In our view, they need to address the strength in the JPY. If the government would intervene with a mind to cap the gains in JPY or the BoJ would introduce a policy of buying foreign bonds, this would be a valuable addition to policy. But these policies appear totally off limits.

The next best thing may be to further increase the cost of hedging foreign investment by lowering negative interest rates. And pull-back on longer-term bond purchases, since yields have already fallen to irrationally low levels and may be having counter-productive effects via increasing savings, lowering inflation expectations and dampening economic confidence. It is hard to see the point in continuing to buy longer-term bonds, perhaps beyond 5-year maturities, at yields below zero.

If the BoJ implements these policy options it may be effective in reversing some of the negative unwanted consequences of its current policy settings and restore some faith in its capacity, in time, to reach 2% inflation. A more normal upward sloping yield curve with negative yields from one to three years and positive yields further out the curve might be conducive to stronger economic confidence in Japan.

JPY should weaken on BoJ operation reverse twist

Almost by definition, to achieve this goal, the JPY needs to be seen as relatively weak, and unlikely to appreciate much, encouraging more unhedged investment abroad. There is no guarantee that by simply buying less long-term bonds, the BoJ will achieve a weaker JPY, although a lower NIRP would more clearly help weaken the JPY, increasing the cost of hedging foreign investment.

However, if the BoJ buys less long term bonds and yields rise and encourage more demand from the private sector in Japan, it will mostly draw funds away from hedged Japanese investment in foreign bond markets (not unhedged) and thus it will not generate additional demand for JPY.

This should increase yields in foreign bond markets. Combined with the higher cost of hedging in Japan (via a lower NIRP), higher yields abroad will increase the return on unhedged foreign investment in Japan, and thus may encourage more Japanese sales of JPY. In addition, it might encourage more carry trades, selling JPY by global investors. This may improve the effectiveness of NIRP, which arguably is designed to weaken the JPY.

When NIRP is achieving its goal of a weaker exchange rate, boosting inflation expectations, it should tend to be associated with a positively sloped yield curve. Almost by definition, if NIRP results in a flat yield curve with negative yields across a wide spectrum of maturities, it is not working. At this point, central bank buying longer-term bonds may be counter-productive. And this appears to be the case in Japan.

As such, the simple act of buying less long-term bonds, helping restore a more normal shaped yield curve may improve the optics of BoJ policy, tend to help lift confidence, inflation expectations and contribute to reversing an irrational and unsustainable pattern of strength in the JPY.

Global market fallout should be contained

From an international perspective, a reversal in the pattern of falling global bond yields has caused some broader correction in higher risk/beta asset prices. Higher longer term bond yields and a more positive sloped yield curve might be expected to draw funds away from higher risk and higher yielding asset markets back into bonds. As such, some correction in asset prices should be expected.

The broad weakening in global asset prices might be associated with a degree of increased risk aversion that undermines global growth confidence. However, to the extent that equity markets rose because of a reach for yield rather than improved earnings, the impact on confidence from a reverse in this trend in unlikely to be severe.

The rise in asset prices in the first place, in the search for yield, was not associated with improved confidence, and in fact represented forced investment that led to increased concern over unsustainable financial market dynamics. As commentary by Gross and Gundlach attested to, fears over unsustainability and irrational pricing in asset markets have been of considerable concern. The Merrill Lynch of global investors has for months reported that cash holdings are much higher than the long-run average.

As such, a correction towards more normal shaped global yield curves and weaker equity prices may, in fact, be associated with some relief with minimal fallout to global confidence via a weaker wealth effect.

Furthermore, the degree to which yields rise beyond a correction from irrationally low levels can be contained by the maintenance of easy central bank policies. Higher bond yields in the US will lessen the case for Fed rate hikes for longer. It will increase the capacity of QE policies to be prolonged for longer. Ultimately yields can only rise sustainably as global inflation expectations recovery.

It is possible to see this arise as the global economy recovers gradually, emerging markets restore more normal growth, fiscal policy becomes more supportive and structural reforms gain momentum. There are no doubt very powerful headwinds from high levels of debt in many countries and political risks that stand in the way of normalizing the global economy. But it is possible that we have seen the beginning of the end of a downtrend in global bond yields.

Brexit risks undermine GBP

At the end of last week, the weak state of European bank balance sheets and Brexit uncertainty came to the foreground to undermine the EUR and GBP. Fears over European banks have flared a couple of times this year and have quickly faded. It may do so again. The latest catalyst was the opening gambit in a proposed USA Department of Justice fine on Deutsche Bank for its involvement in the pre-2007 mortgage-backed bond fiasco in the USD that was a key factor in triggering the 2008 Global Financial Crisis. It seems unlikely that this issue will be the one that tips the scales towards a new sense of crisis in European banks.

UK Brexit fears were stoked by an admission (reported by those close to the UK government discussions) that Chancellor of the Exchequer Phillip Hammond was ready to accept that the UK would have to leave the EU single market. This should not be an enormous shock judging by the many comments since the Brexit vote from EU politicians that the UK will not be allowed to have its cake (limit immigration) and eat it too (access to the single market).

A key fallback position of the UK government is to negotiate a deal with the EU that allows its financial services sector to remain highly integrated with Europe and can continue its role as a center of financial services for Europe and in turn globally; a crucial plank in the UK economy. At issue is the so-called “passporting rights” of financial services companies in the UK to operate freely across the European Economic Area (EEA). But even this objective is fraught with uncertainty, and other UK sectors would surely suffer for longer and perhaps indefinitely if left out of the single market.

The Brexit uncertainty for the UK may be set to remain a weight on the GBP this week after EU leaders appeared to harden their views on dealing with the UK Brexit, emphasizing a need to force the UK to suffer the consequences of its exit to encourage other member states to pull together and deal with their problems rather than emulate Britain and try its luck outside the EU.

At a summit of EU leaders (the first excluding the UK) in Bratislava, Slovakia last weekend, the Slovak Prime Minister Robert Fico, holder of the rotating EU presidency, is reported by the FT to have said, “Europe will make Brexit “very painful” and ensure Britain is worse off outside the EU, Slovakia’s premier has said, as he dismissed the UK’s confidence about divorce talks as “bluff”. And further, “It will be very difficult for the UK, very difficult,” he said in an interview with the Financial Times, “The EU will take this opportunity to show the public: ‘listen guys, now you will see why it is important to stay in the EU’. This will be the position.”

Slovakia says Europe will make Brexit ‘very painful’ for UK – FT.com