EUR and CAD need to square up to growing threats

The market has spent much of this year unwinding a structural short EUR position. Bank analysts have shifted to a bullish long-term EUR view, ECB QE taper is largely priced-in, the political risk gap between Europe and the USA has narrowed, and the EUR is now stretched from its widening yield disadvantage. Traders appear to hold an extreme long EUR position, and a head-and-shoulders top appears to be developing; a break of recent lows might target a fall to 1.13. The US is making progress towards tax reform, and the market is too sanguine on US inflation risks. Traders also appear to be holding extreme long positions in CAD, the Bank of Canada has shifted its tone on its policy outlook, Canada housing market is slowing, and negotiations on NAFTA are not going well (although have been extended).

The USD may be pulling out of down-trend this year

The USD may be starting to show signs of pulling out of the falling trend since the beginning of the year. A key resistance for the USD will be the recent high established around a week ago. A break above that level will tend to support the notion that its recovery over the last month is real and can build into year-end.

EUR direction may be key for USD

Arguably, one of the driving forces behind the weaker USD trend this year has been a relentless rebound in the EUR. To some extent, this mirrors the strength in the JPY last year that contributed to a weaker USD trend through the first three quarters of 2016. In both cases, the market ignored the protests of the central bank guardians of these currencies and their ongoing commitment to accommodative monetary policy.

To be fair, in the case of the EUR, the ECB is moving towards a taper, whereas the BoJ is still deep in its most accommodative stance. Nevertheless, the ECB has been at pains to emphasize “patience and persistence.”

Unwind in structural short EUR largely complete

The bottom line is that both the JPY rebound last year, and the EUR rebound this year appear to have been driven by a significant unwind of structural shorts in these currencies.

Very few analysts have made mention of interest rate or yield differentials as a factor in their EUR forecasts this year. Quite simply these have tended to play little part in EUR direction. Instead, they have discussed the EUR as responding to a more solid and sustained growth path and capital inflow to its equity markets.

We can only guess as to when the broader market has unwound a structural position (in this case a short EUR). Time is a factor; it has been a 10-month period of strength in the EUR, not dissimilar to the period of JPY strength last year before it reversed course.

Another factor might be judging market sentiment. FX analysts have come around to now forecasting a stable long-term recovery in EUR. Bloomberg shows the median forecast is for 1.20 in mid-2018, 1.22 at end-2018, onto 1.25 over the two and three-year horizon. This is probably indicative of the broad sentiment in the market, and we might conclude that, on balance, investors are no longer significantly under-weight EUR.

QE taper priced-in

Another way to assess structural positions is the reaction to recent news. The market no longer appears to be reacting much to news that the ECB is set to taper its QE purchases for a second time in January, with an end to purchases insight around Q3 next year.

Bloomberg reported on 12 October that un-named ECB officials said that a cut in monthly purchases in half from EUR60bn to 30bn from January, to run through to at least September next year, was a feasible option. There was little reaction to this widely reported story. In fact, the EUR slipped from its recent highs after this report, and failed to hold gains after a weaker than expected US CPI report released on the following day.

ECB to Consider Cutting QE Purchases in Half Next Year – Bloomberg.com

We might conclude that the ECB has filtered its plan for tapering into the market ahead of its meeting next week and the market is largely prepared for the announcement. The weaker EUR since this, probably controlled, leak suggests that the EUR is losing momentum and is at greater risk of a deeper fall in coming weeks.

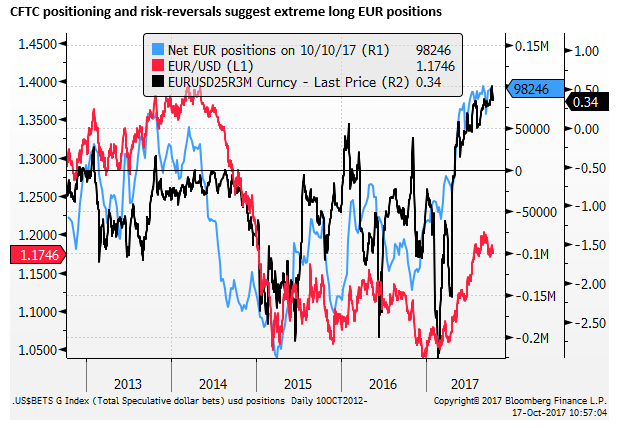

Traders long EUR

Other evidence suggests that short-term traders have amassed a long position in the EUR. The CFTC data on EUR futures positions of non-commercial traders on the CME, since July, have been around their previous extremes.

These positions have crept higher in recent weeks, notwithstanding some weakness in the EUR. As such, traders have tended to buy the recent dip in the EUR, and may be well loaded up on the currency. The risk is that buying power for the EUR is used up, and a position unwind may trigger a deep fall if bullish EUR sentiment starts to turn.

The skew in EUR option risk reversals also suggests that the market is quite bullish for EUR, and therefore holding long positions.

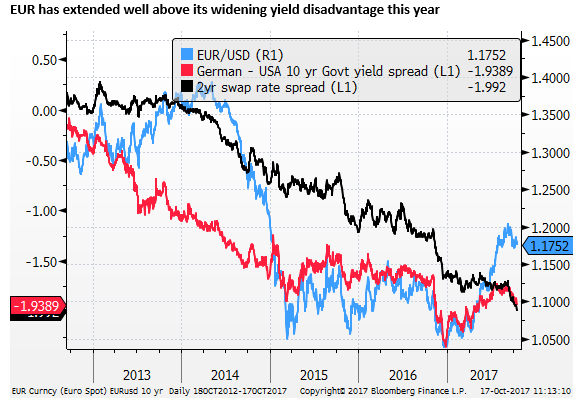

EUR extended from yield spreads

Having identified that the market may have unwound a structural short EUR position, and traders may be long, we need to be on the lookout for what could turn sentiment towards EUR. One factor could be a shift in focus back towards the yield spread between EUR and USD. While this has not been a focus for most of this year, the EUR has stretched quite a distance from this spread this year, and the market might begin to fear that it snaps back.

Now that the market has largely built-in a taper in QE, it might move its attention back to the ECB’s commitment to keep interest rates at their current negative rate “for an extended period of time, and well past the horizon of our net asset purchases.”

Political risk gap narrows

Another consideration is the relative political outlook in the USA and Europe. Since the election of Macron as President of France in May this year, the Eurozone has appeared to be displaying much greater unity and political stability, whereas the Trump administration has appeared chaotic and Congress has failed to pass key legislation; in particular in healthcare.

However, in the last month. Merkel’s CDU party underperformed in elections, and she is trying to cobble together a coalition with left and right parties. The far right AfD party has entered the Bundestag for the first time with over 13% of seats. Merkel’s CDU party also under-performed expectations in the state elections in Lower Saxony on the weekend.

After Austrian elections over the weekend, a coalition involving a far-right party may take power. Spain is grappling with a successionist movement in Catalonia. An election is slated for Italy before 20 May next year, and the far-left Five-star movement is vying for leadership.

In the USA, the market may be getting used to the Trump-style of politics. And he appears to be doing a better job in recent months showing a capacity to make deals across the aisle; including on hurricane funding and moving the debt ceiling forward.

This week he has appeared in a joint press conference with Senate Majority leader McConnell and has expressed his support for a bipartisan bill in the works for funding for Obamacare subsidies in exchange for giving states more flexibility. The bar may have been lowered for Trump and Congress, but they are now more easily rising above it.

The administration and Congress have shifted more attention to tax reform. There appears to be as much potential for upside surprises in Congress as disappointment.

A key Budget vote slated for Thursday this week would increase the odds of a tax reform bill later this year or early next year. Passage would be a positive for the USD.

EUR Head and Shoulders

As we mentioned earlier, a key resistance level for the USD is its recent highs set just over a week ago. In relation to the EUR, this resistance appears more powerful. A break of the recent lows in EUR will generate the appearance of a head and shoulders reversal in EUR that might target a fall to around 1.13.

A fall to 1.13 is far from the mind of the market at the moment, but consider the risk that inflation and wages data in the USA are higher than expected and/or Congress makes progress on tax reform. Such events may be catalysts for a major reversal of sentiment.

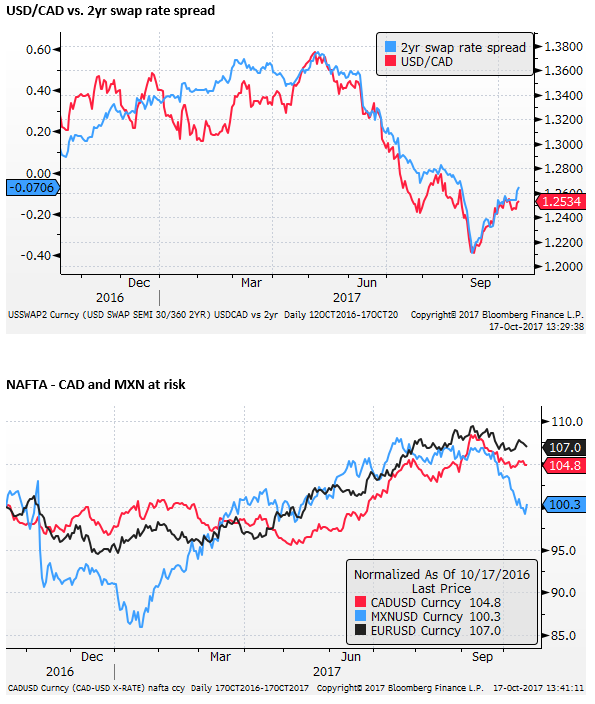

CAD at risk of a deeper correction

Another currency where we see the risk of a deeper correction is for the CAD. Apart from the shift in tone on the rates outlook by the BoC, some moderation in economic reports, including weaker house prices in recent months, it appears that NAFTA risks are starting to creep into the CAD.

Like the EUR, traders appear to be holding significant net long positions in CAD, making it more vulnerable to a shift in sentiment.

The CAD gyrated today, along with the MXN. It fell first on reports that both Canada and Mexico negotiators rejected a range of US proposals. Later it rebounded on reports that the parties had agreed to extend the talks through Q1 next year; raising hopes that all sides are willing to keep working on a deal for longer.

Trilateral Statement on the Conclusion of the Fourth Round of NAFTA Negotiations – Canada.ca