EUR feeling pinch, Trump tax policies would boost USD

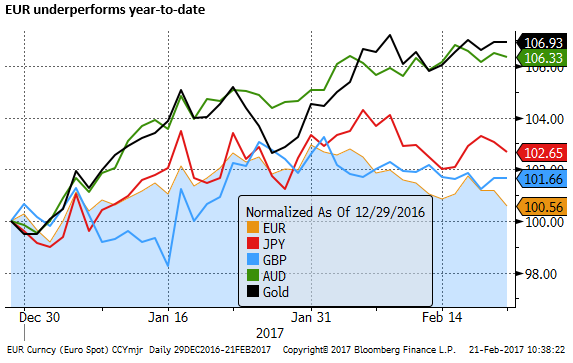

The EUR has underperformed most currencies this year, despite signs of strengthening economic recovery in the Eurozone. Political risk and the Greek debt merry-go-round may be weighing on the currency. Widening in Eurozone periphery bond spreads continues as a trend, and the alternative right contender in French elections in April/May Marine Le Pen is seen in betting markets as having as much chance of victory as the two leading moderate contenders Macron and Fillon. Two weeks ago, Trump raised expectations of an announcement of major tax reform very soon and sounded constructive towards China and Japanese trade relations, contributing to a bounce in the USD. However, this was soon overshadowed by controversy over his former National Security Advisor and allegations of collusion with Russia, and a pivot back to immigration policy and attacking the mainstream media. US equities still seem to have their eyes on the tax policy prize, but the USD less so. Indeed some obstacles and distractions may delay the tax plan, but a border adjustment tax appears central to the plan, and this should place clear upside pressure on the USD exchange rate. Something to keep in mind as we await progress or otherwise.

EUR feeling the pinch

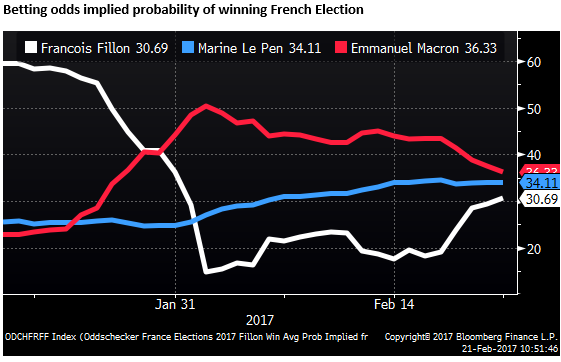

EUR may be starting to feel the pinch from the coming French election and the merry-go-round on the Greek bailout package. (First round of French election on 23 April, final two runoff on 7 May)

The betting odds of winning the final French Presidential election for the top three candidates shows that it appears to be an even race, with the favorite Macron’s probability of winning falling back close to Marine Le Pen and Fillon. It appears likely that Le Pen will make it through the first round of voting to the final run-off.

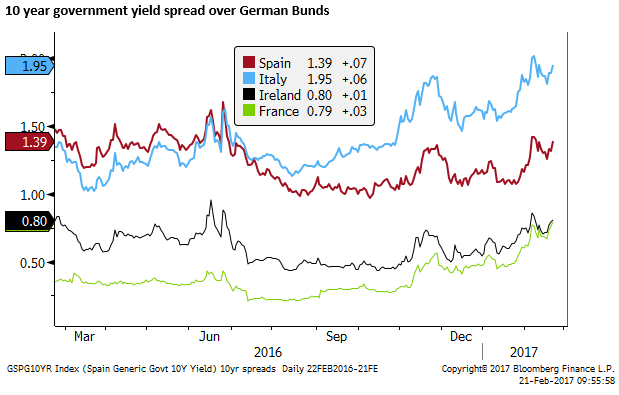

There has again been some widening in Periphery Eurozone Government bond spreads in recent days. The French spread has risen to a cyclical high.

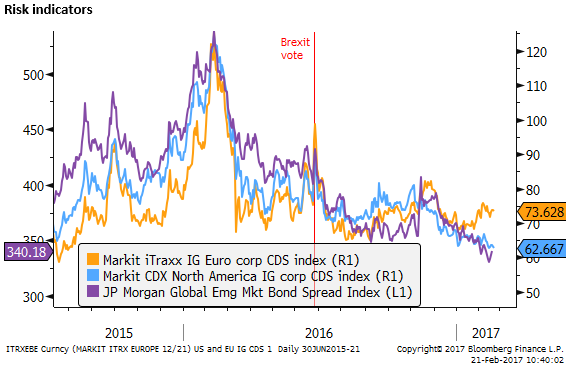

Credit Default Swap indices show under-performance in European investment grade corporate risk (higher CDS) relative to US corporates and emerging markets.

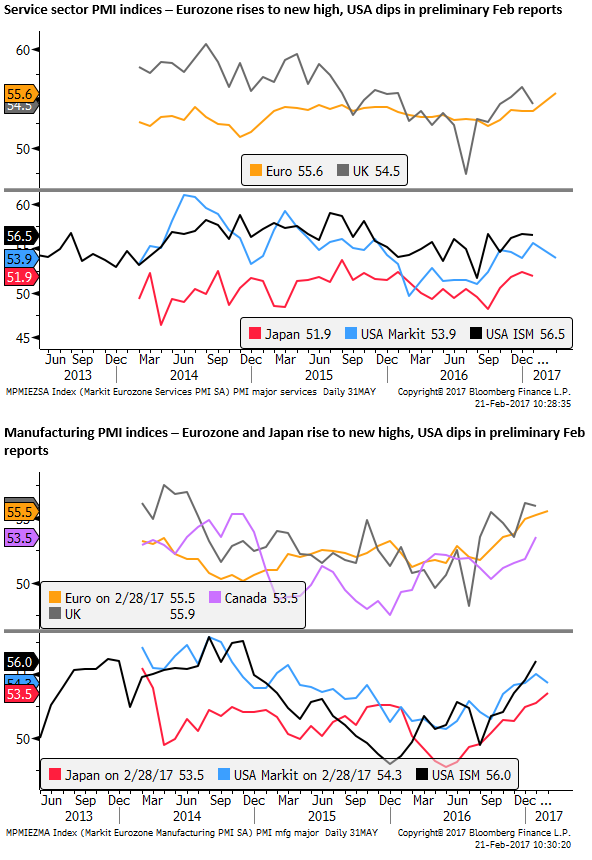

EUR failed to draw much support from its preliminary PMI data, rising to new cyclical highs for both services and manufacturing. Whereas the preliminary Markit USA PMI data were softer.

Still waiting for Trump’s tax policy

There appears to be a lot riding on the tax plan promised by Trump. US equities seem to have risen significantly in anticipation of a sizeable corporate tax overhaul that is expected to cut the corporate tax rate from 35% to 20%, or even to 15%, and apply border adjustment to remove tax payable on export revenue but also remove the tax deductibility of import expenses.

Trump said during his press conference with Japan PM Abe not quite two weeks ago that “what is happening with the tax structure is going along very well” and there will be “some very big news on tax structure over the next short period of time.”

He also said that, “I think the US is going to be an even bigger player than it is right now, by a lot, when it comes to trade, a lot of that will have to do with our tax policy which you will be seeing in the not too distant future. We will have an incentive based policy much more than we have right now. Right now nobody even knows what policy we have, but we are going to have a very much incentive based policy, working with Congress, working with Paul Ryan, working with Mitch McConnell. And I think people are going to be very very impressed.”

This seems to suggest the House Republican plan for a corporate tax cut with a border adjustment tax will be the basis for Trump’s tax policy.

Border Adjustment Tax a key feature

The Tax Foundation describes the border tax adjustment (BAT) as shifting from a “production-based” to a “destination-based” tax. Essentially you are taxed where goods are sold rather than produced.

Understanding the House GOP’s Border Adjustment – taxfoundation.org

The Tax Foundation argues that the BAT acts somewhat like a Value-Added-Tax (VAT) or Goods and Services Tax (GST), which are applied in many countries with exemptions for exports, but not the USA (although the USA does have state-based sales taxes). In this sense, it helps justify the BAT on the grounds that it levels the playing field with countries that have VATs that are not applied to exports.

However, the equivalence of BAT and VAT is debatable and the former may run into complaints from foreign countries that it does not comply with World Trade Organization (WTO) rules. The BAT looks very much like a tariff on imports and rebate on exports that would give the USA a trade advantage.

Trump Is Right: ‘Border Adjustment’ Tax Is Complicated – Bloomberg.com

The tax overhaul promised by Trump appears to be based on a proposal from House of Representative Republicans in Congress first released in June 2016 (A Better Way – abetterway.speaker.gov) that proposes converting the current corporate tax into a “destination-based cash flow tax”. The cash flow part means that US companies could expense capital investment in the first year rather than depreciate them over a number of years.

Expected to bring back jobs

The proponents of the tax overhaul hope that it will boost the tax base, employment and investment in the USA. It would do so by reducing the incentive for USA companies to shift production overseas to take advantage of lower foreign tax rates. It might reduce the apparent practice of large US corporations holding foreign sourced income in foreign countries, waiting to see if the US government will provide a tax holiday. And it might reduce so-called tax inversions, where a small foreign company buys a large USA company. In fact, some may argue that the aim of the tax overhaul is to make the USA appear something of a tax haven and encourage foreign companies to move to the USA.

Raising extra revenue from importers

The other advantage of the BAT is that, all other things equal, it should raise significant additional revenue because the USA has a large trade deficit. By effectively imposing a tax on imports and a rebate on exports, in theory equal to the proposed corporate tax rate (20%), the US government would earn 20% of the trade deficit. The annual trade deficit is currently around $500bn, suggesting that the government would earn $100bn per year. The idea is that this helps pay for the overall corporate tax cut.

However, the BAT will increase costs on USA importers, and of course, considering the USA has a trade deficit, these are a very significant part of the economy. Large retail companies in the USA, importing foreign goods for sale to US consumers, will attempt to pass on higher costs of imports to consumers, tending to raise inflation in the USA. While these companies may benefit from an overall corporate tax cut, they will have to pay a bigger share of corporate tax than less import-intensive and more export-orientated businesses. The prospect of higher prices for US consumers is an obvious draw-back of the tax policy that is expected to generate pushback in Congress.

BAT should cause USD to appreciate

The Tax Foundation argues that the BAT is trade neutral, suggesting that it should have no net impact on the trade balance. However, it comes to this conclusion with the help of adjustment in the exchange rate and national prices. The bottom line is that the BAT will cause the USD to appreciate and/or prices in the USA, especially for imports, to rise.

All other things equal, a BAT makes importing less profitable, imported goods more expensive, and exporting more profitable. If there were no exchange rate or price adjustment we would expect the trade balance to narrow and stronger demand for domestically produced goods over imports. This would tend to cause more generalized inflation. It might also tend to boost capital inflow as companies sought to bring production onshore. The combination of narrowing in the trade deficit and more capital inflow would place upward pressure on the exchange rate.

In a flexible exchange rate regime, currency appreciation would be expected to make the bulk of the adjustment to rebalance supply and demand. A higher exchange rate would make exports less competitive and imports cheaper, and reduce the advantage of moving production onshore, tending to offset the effects of the BAT on the trade deficit and balance of payments.

From our perspective, as a currency analyst, it would seem that the USA tax overall is, if nothing else, bullish for the USD. It is perhaps somewhat surprising that the USD has not risen more in response to Trump and Republican tax overhaul plans.

This is especially the case since the US equity market has appeared to be more clearly and consistently lifted by the prospect of tax overhaul. Although to be fair, global equities are higher perhaps in response to stronger global growth indicators; including the PMI data charts shown above.

Delays and Distractions

The stock market may have its eyes more clearly focused on the tax plan prize, while the currency market may weighing up the difficulties of passing complex legislation amidst a variety of other Trump Administration priorities and distractions.

Trump has spent much political capital in pursuing his policies on immigration and may get bogged down with repealing and replacing Obamacare. Healthcare policy has been a political mine field for past administrations, and it threatens to derail progress in tax policy.

The following WSJ article suggests that it may be necessary to resolve healthcare policy first in order to pave the way for tax policy.

The article says: “GOP leaders consider handling Obamacare first vital for procedural reasons. It’s necessary to resolve the costs and tax implications of the health plan to write a new budget. And under congressional rules a new budget plan is necessary to provide an umbrella under which a tax overhaul can be passed with a simple majority, thereby avoiding a potentially deadly Democratic filibuster in the Senate. So, unless Republicans are willing to try to get the eight Senate Democratic votes needed to pass a tax bill, tax change will be hostage to Obamacare.”

Amid Trump Controversies, Tax Overhaul’s Uncertain Path – WSJ.com

The other difficulty is paying for the tax overhaul. The plan appears set to cut corporate tax sharply, and Trump said he also wants to cut personal income tax rates. Even if the BAT is expected to raise $100bn per year directly, this is not going to cover more than a fraction of the budget hole that broad tax cuts will create.

The Trump administration would have us believe that the tax cuts will unleash a more productive and stronger US economy, allowing it to ride the Laffer curve to prosperity and pay for tax cuts, in a way that President Ronald Regan is often credited in the 1980s. However, the Congressional Budget Office (CBO) and the Federal Reserve are far from convinced. As such, the Trump Administration may struggle to create an impression of sustainable budget policy. Something that may be required to garner sufficient support for its tax proposals from fiscal conservatives in its own party.

It is approaching two weeks since Trump last had much to say about tax reform. He has been dealing with choosing a new National Security Advisor and deflecting allegations of colluding with Russian government officials during and after the election campaign. He has reverted to making much noise on immigration issues and attacking the mainstream media.

Perhaps announcements on tax policy reform are coming soon. Surely the market and the media will begin to ask more questions on this issue soon. On the other hand, the continued focus on other issues may be tending to undermine the USD.

Trump wants a weaker USD

A factor that may have caused some weakness in the USD this year is that Trump and his administration officials have at various times continued to imply that major USA trading partners, including China and Germany, have used policies designed to weaken their currencies to take a trade advantage.

The implication is that Trump would prefer a weaker USD and certainly might come out and comment against broad further strength in the USD should it occur.

It is far from clear that these types of comments would have any lasting impact on the exchange rate. If Trump and the Republican-led Congress succeed in delivering a corporate tax reform with a BAT, the USD is more likely to rise.

However, Trump’s comments on currencies and trade are part of a broader theme of protectionism that tends to threaten confidence in global growth. At times this might seem to support alternative safe havens like gold and JPY.

Risk aversion has been more atmospheric than apparent in broader market developments. It appears to be seen in some reduction in USD long positions taken initially on hopes of growth-orientated Trump policies. However, emerging market, commodity prices, and currencies have been buoyant, tending to ignore risk factors and respond to evidence of improving global economic growth.

At the time of the Abe visit, Trump appeared to soften his attitude towards both Japan and China, suggesting that he may approach trade relations with this two major trading partners in a more measured manner. This, combined with his comments on tax reform, allowed some rebound in the USD. However, this was soon overshadowed by the controversy surrounding his former National Security Advisor.