EUR looks like the safe play

The EUR has broken above the psychological 1.10 level after a lengthy and frustrating period of consolidation below this level since the first round of the French election. Eurozone economic momentum has maintained a steady improving trend and more clearly appears on a sustainable path to achieving the ECB’s inflation goals over the medium term, in contrast to Japan which is nowhere in sight of ending its unconventional extreme policy easing measures. Political risk in Europe has faded whereas it has increased in the USA as Trump stumbles from one controversy to the next. Geopolitical risk remains elevated with the US still threatening trade disputes, China’s credit issues ever present, North Korea threatening and the US President shifting to focus on fighting ISIS. Europe is looking more like a haven rather than a source of risk. Trump’s domestic economic policy appears stalled, and the risk is that US economic confidence fades. Many commentators see US equities as relatively expensive, and equity flow appears to be moving towards the Eurozone with more consistency. The ECB may continue to talk down the prospect of a change in ECB policy, but this may only serve to slow the recovery in EUR. A move towards the high side of its range over recent years near 1.15 seems quite possible.

EUR sentiment shift

After a frustrating period of consolidation following the first round of the French election, and whipsaw on the second election round, the EUR has decisively broken its recent range.

A factor that may have delayed the EUR rise is positioning. Despite the ECB’s negative rate and QE policy, speculative traders using the CME futures market have been reducing their short EUR positions this year, moving last week to the first net long position since 2014.

The shift to a net long EUR speculative position may be a headwind for the EUR, but it is consistent with shifting sentiment towards to EUR, supported by consistent Eurozone economy strength this year, signs that core inflation is improving and strength in the Eurozone equity market.

Eurozone economy consistency

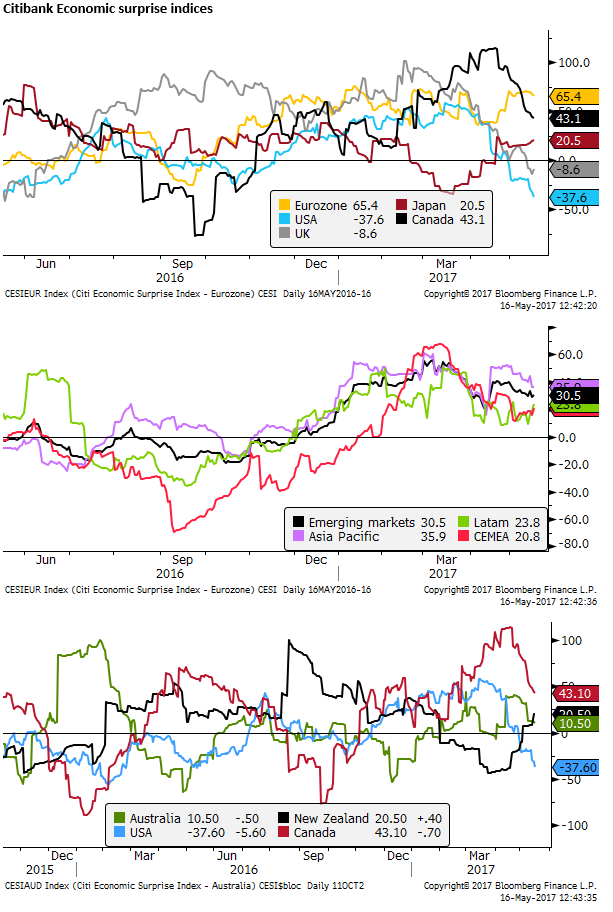

In terms of beating market expectations, EUR is now leading the pack. The Citibank economic surprise indices show persistent out-performance in the Eurozone since Q3 last year. Whereas, USA economic data has been underwhelming in recent months; its economic surprise index is below all others, including EM and commodity exporters.

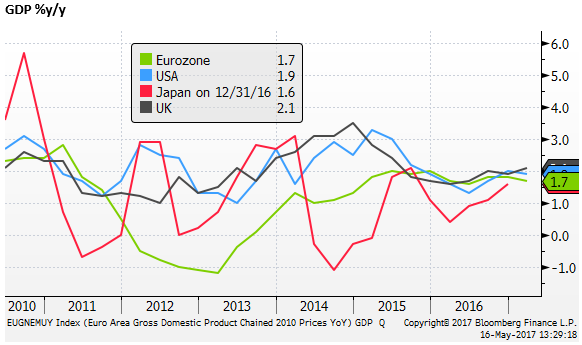

Q1 GDP released in the Eurozone on Tuesday, rose as expected by a 0.5%q/q and 1.7%y/y, after rising 0.5% q/q in Q4 last year, maintaining a steady solid path in recent years, above the long-run potential, which may be around 1%.

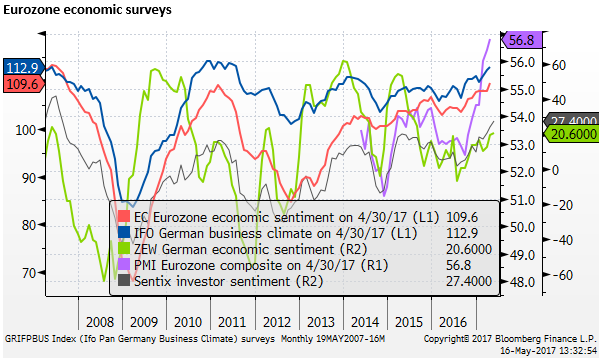

The German ZEW index continued the recent pattern of improving economic surveys; firming in May, albeit rising less than expected.

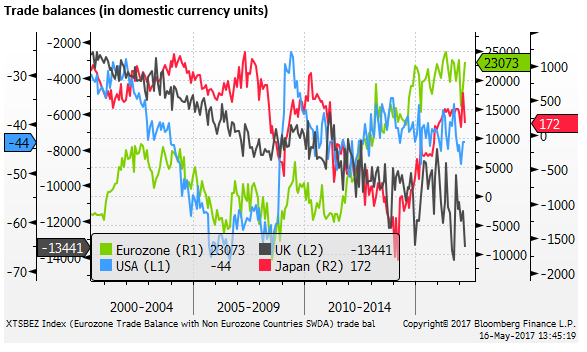

Trade balance trends support EUR

The Eurozone trade balance released on Tuesday rebounded more than expected to EUR23.1bn, well ahead of the expected 18.7bn, returning to near record highs, contrasting with weaker trends in the deficit majors – USA and UK. We can only imagine what Trump and his Commerce Secretary Ross might say about this trend and the appropriate level of the EUR.

Eurozone asset markets show strength

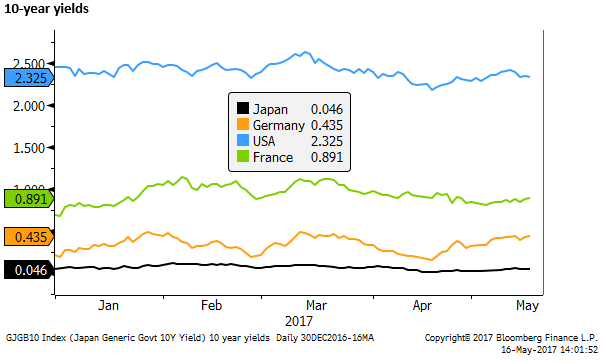

The market continues to look towards the Fed raising rates, with a hike on 14 June 80 to 90% priced-in. However, US yields have stalled in recent weeks, whereas they have firmed in Germany. Some of this may reflect the ebbing in political risk in Europe, but even French yields have firmed in recent weeks. This suggests that confidence in the recovery may be rising in the Eurozone, whereas the market is in two minds about the outlook in the USA.

Eurozone equities surged after the first round of the French election, and have continued to rise in May, significantly out-performing the US equity market, notwithstanding the gains in the EUR exchange rate.

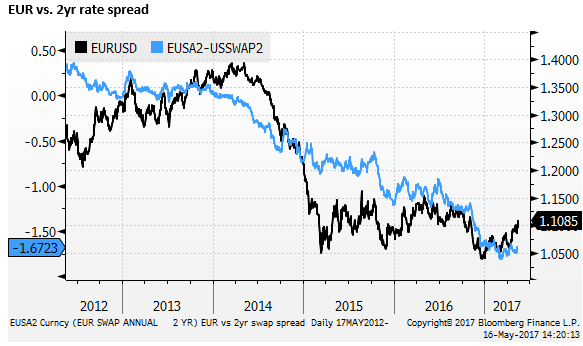

EUR is not particularly responsive to yield spreads

It is evident that rate spreads are not a significant driver of the EUR in recent years. The yield spread has moved somewhat in favour of the EUR in recent weeks as US rates have ebbed, but, overall, the 2yr yield spread has remained relatively stable this year, whereas the EUR has recovered to its high since November. The EUR has now essentially unwound the Trump rally in the USD that follows his election on 8 November.

Relatively low and negative EUR yields may help slow the rally in the EUR, but the market is responding to economic growth and equity flows. The market can see the end of the ECB’s extraordinary monetary policy in view. QE tapering is widely expected beyond the current QE policy set to expire in December.

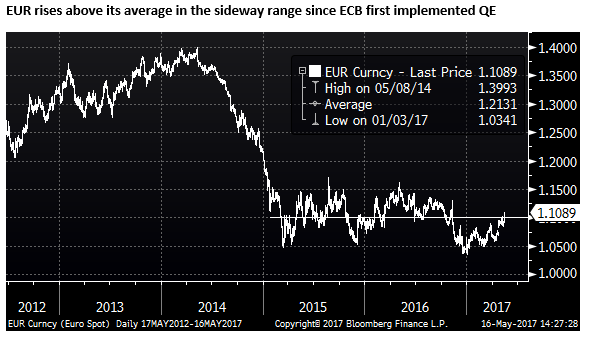

EUR rises above its average in its sideway range since ECB QE first implemented

In December last year, EUR briefly broke to a new low. However, it has since established itself above the key 1.05 level. It is now above its average since the ECB first implemented QE policy in January 2015 at around 1.10. it might seem now on its way to test the high side of this range at 1.15.

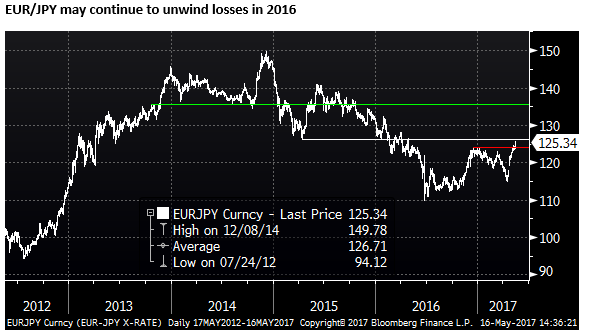

Against the JPY, EUR has broken above its highs around the turn of the year. However, it is still well below its levels from 2013 to 2015. While the Eurozone is making significant progress towards reaching its inflation target goals, and the end of its QE policy is coming into view, the same cannot be said for Japan. It is conceivable that EUR/JPY will continue to rise, notwithstanding its recent sharp rally since the French election, to levels around which it traded when ECB QE policy was first implemented in 2015 (around 135).