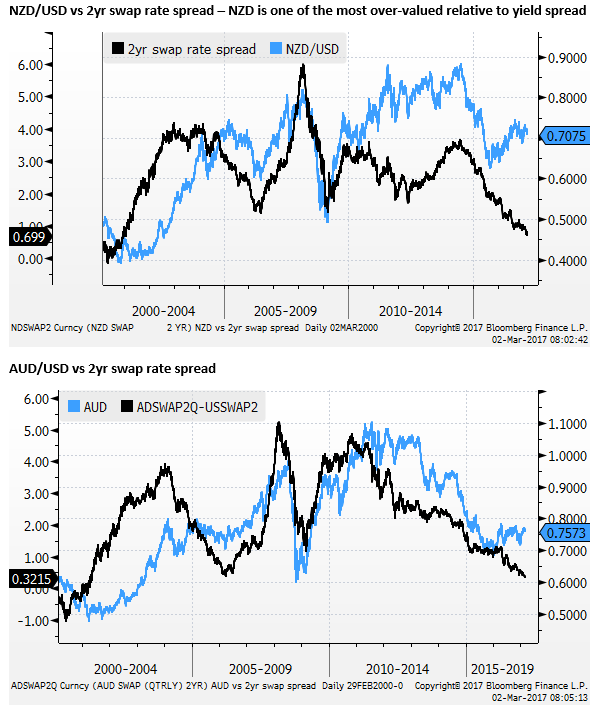

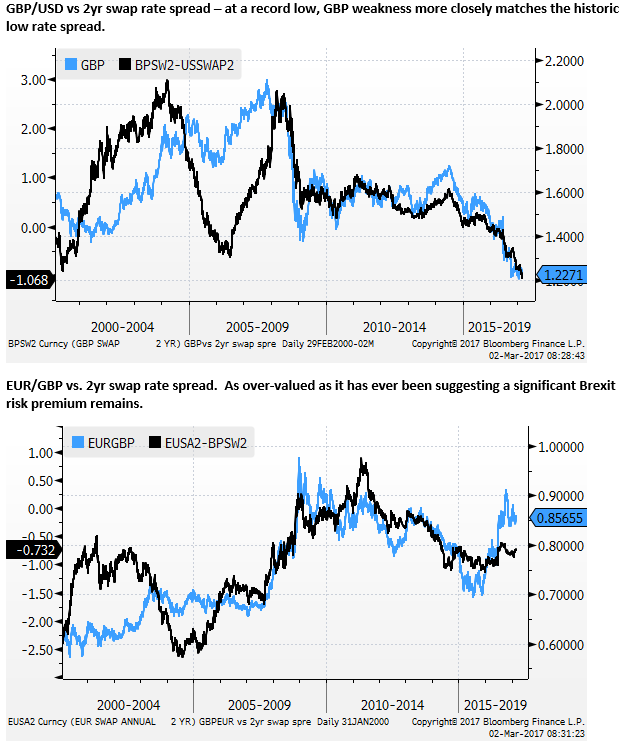

Fed already behind the curve, USD looks cheap compared to yield gaps, NZD expensive

Alternative measures of core inflation in the US, including the Dallas Fed’s PCE trimmed mean measures, show inflation is now very close to the Fed’s mandate and in a rising trend. Core CPI measures, including the Cleveland Fed’s trimmed mean and median, are well above the mandate. Inflation trends globally appear to have turned higher, including in China, the USA’s biggest source of imported goods. The NY Fed’s survey of inflation expectations was at an 18-month high in January. Jobless claims were at a record low last week, and a range of activity indicators show rising and above trend growth; including the ISM manufacturing new orders index rising in February to equal the peak in 2013. While there has been much focus on Trump’s economic policy proposals, current indicators suggest that the Fed may have fallen behind the curve. Apart from hiking on 15 March, now widely expected, the Fed may also upgrade its forecast for rates and its risk assessment. The USD has significantly underperformed the improvement in its yield advantage over the last 18 months. Even though the USD is at historically high levels, compared to relative interest rates, it now appears cheap against most currency pairs. The NZD appears to be one of the most over-valued currencies compared to yield spreads and would be vulnerable to any pullback in global risk appetite or a further rise in global bond yields.

USD has underperformed its yield advantage for around 18-months

The USD has bounced back this week on heightened expectations of a Fed rate hike in two week’s time. However, the USD has still significantly underperformed the improvement in its yield advantage over the last 18 months. While the USD looks historically expensive, its gains since 2014 appear to be more than fully explained by relatively high US yields.

NZD on borrowed time

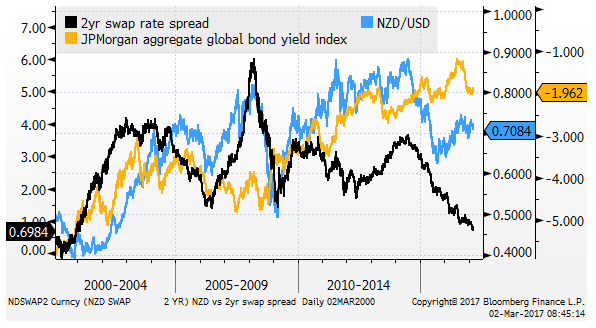

One of the factors that we have used in the past year to account for the under-performance of the USD relative to interest rates is the fall in global yields and the ‘search for yield’. Investors have been willing to accept a thinner margin of additional return for the same amount of risk.

In particular, this may have helped explain the stronger performance of higher yielding currencies like the NZD, which has more clearly out-performed its narrowing yield advantage than most other currencies.

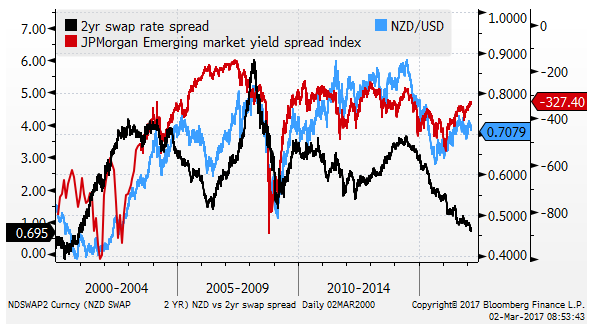

The chart below adds the JPMorgan aggregate global bond yield index to the chart shown above (inverted). As yields fell to record lows around the middle of last year, it may have helped explain the divergence in the NZD/USD from its narrowing yield advantage.

Global bond yields have risen significantly since around September last year. However, so far, they remain relatively low, below levels that prevailed in 2015. Perhaps they have not advanced enough yet to significantly break the back of extreme ‘search-for-yield’ investor behavior and force the NZD/USD lower to re-connect with its lowest yield advantage since 2001.

The chart below shows the same chart above, but this time adds the JPMorgan emerging market bond spread (over US Treasuries) index (inverted). This index has fallen to new lows since 2014, suggesting that the search for yield remains strong even as global bond yields have risen. This index is also closely aligned with degrees of risk appetite and global equity markets that have increased strongly in recent months.

This index appears to explain a good deal of the movement in NZD/USD since 2008, more so than the interest rate spread. But we wonder, now that with the absolute NZD/USD 2yr yield advantage is low (70bp), with global bond yields rising, whether the ‘pick-up’ in yield is enough to compensate investors for the exchange rate risk.

The NZD would be more vulnerable if the current upswing in global equities and narrowing credit spreads were to have a setback. Global growth indicators appear to be more supportive for global asset markets. But risks are also growing with the Fed expected to move ahead with policy tightening, building evidence of global inflation pressure, intense uncertainty over the political agenda in the US, political uncertainty in Europe and ongoing fears that Chinese debt levels and growth are too high and too fast.

USA inflation close to the Fed’s mandate

Looking more immediately at the case for rate rises in the USA, we agree with the assessment of recent Fed speakers that the Fed is now close to its dual mandate, recent evidence suggests that economic growth remains above trend, and further progress is being made towards the Fed’s goal of full employment and 2% inflation.

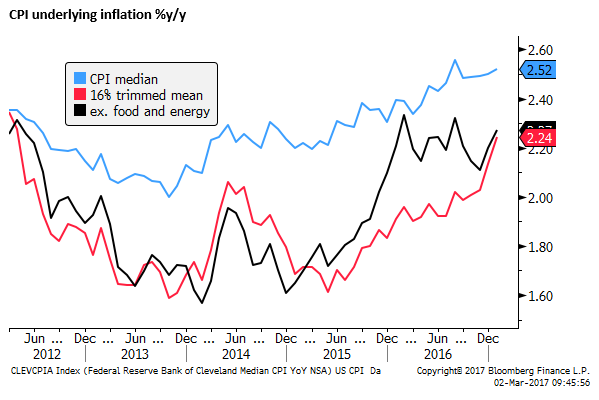

The PCE inflation report was close to expected on Wednesday. Headline inflation at 1.9% and PCE core (excluding food and energy) at 1.7%y/y. However, the Dallas Fed’s alternative core or underlying measure (trimmed mean) rose on a 12-month rate by 1.9% in Jan, a high since 2012, just short of the 2% Fed target. The six-month annualized rate was also 1.9%, up from 1.7% in Dec.

The Fed has noted some residual seasonality in the seasonally adjusted US inflation data, and this appears to be born out on the six-month annualized trimmed mean that has tended to peak around the middle of the year, and trough at the end of the year. Again, it has jumped sharply in January. Seasonality aside, the trend appears more clearly rising, and the underlying measure close to target.

Behind the Numbers: PCE Inflation Update, January 2017 – DallasFed.org

The same trend is also apparent in the CPI data. The Cleveland Fed’s trimmed mean underlying measure of CPI inflation rose sharply from 2.03% in November to 2.24% in January, now clearly above the 2% Fed target and in-line with the CPI excluding food and energy. The Cleveland Fed’s other alternative underlying measure (CPI median) was already well above the Fed target, averaging above 2.50% since August last year, firming to 2.52%y/y in January.

These underlying measures suggest that the Fed is facing a rising trend in inflation that is already very close to its target, and well above target on all underlying CPI measures.

Cleveland Fed CPI measures – ClevelandFed.org

In its January policy statement, the Fed said, “Inflation increased in recent quarters but is still below the Committee’s 2 percent longer-run objective.” The headline PCE deflator was 1.9%y/y in January, and the PCE excluding food and energy, most frequently referred to as the Fed’s preferred core inflation reading, was 1.7%. As such, technically, it could maintain the same statement. But it might acknowledge in its next statement that it is close to reaching its inflation target.

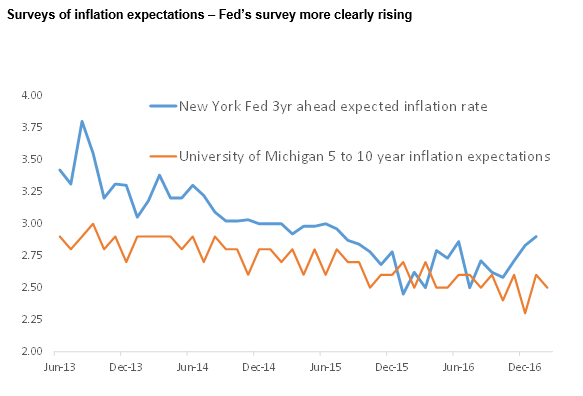

New York Fed’s survey of inflation expectations higher

On inflation expectations the Fed said in January that, “Market-based measures of inflation compensation remain low; most survey-based measures of longer-term inflation expectations are little changed, on balance.”

The New York Fed’s survey of inflation expectations three-year ahead median rose for a third month in a row in January to 2.90%, a high since July 2015, up from a low of 2.50% in June last year.

On the other hand, the University of Michigan Consumer Sentiment survey has not shown any noticeable change in its 5yr to 10 yr ahead inflation expectation, which remains around its low levels seen in the last year or so, last at 2.5%.

Nevertheless, the Fed’s Dudley has said he prefers the quality of the New York Fed’s survey, and there is fledgling evidence of rising inflation expectations in this survey.

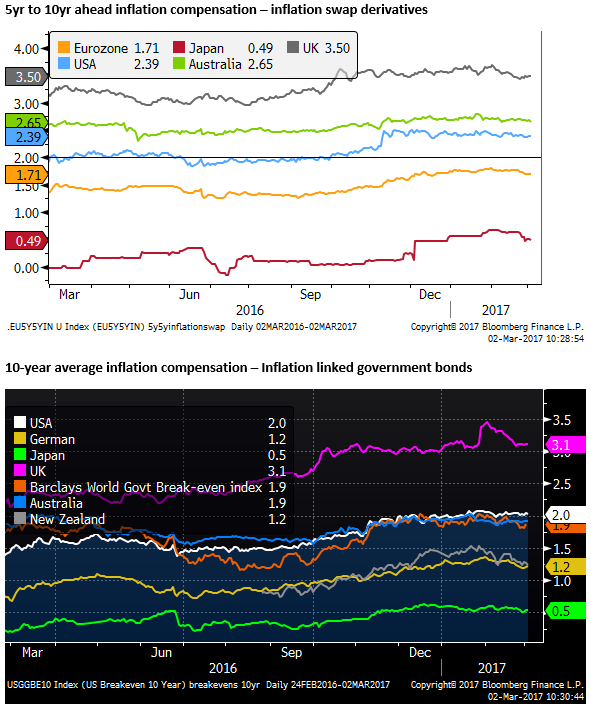

Market-based measures of long-term inflation compensation have dipped a bit recently, after rising significantly in the lead up to and soon after the US election in November. As such the Fed might continue with its January assessment “they remain low”.

Higher global impulse for inflation

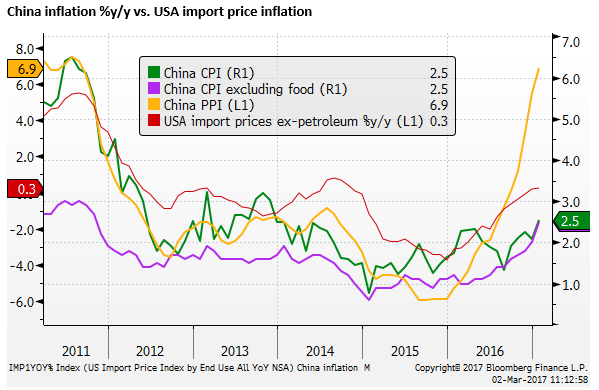

The global impulse for higher inflation also appears to have increased. Headline inflation rates have picked up around the world, in large part related to the recovery in commodity prices. This may tend to help build global inflation expectations.

There is mixed evidence of a pick-up in underlying inflation readings, but these have picked up in a number of nations from low levels and are at least stable in most. The inflation readings in China have gained a lot of attention, seen in the past as a source of global deflation. Their trend has shifted decisively in the last year. As the USA’s largest trading partner this should tend to raise inflation expectations in the USA.

Activity indicators point to above trend growth momentum

The Atlanta Fed down-graded its Q1 GDP growth forecast from 2.5% to 1.9% following the weaker than expected January personal spending data (showing a decline real spending of -0.3%m/m). This would continue a pattern of relatively modest growth (1.9%y/y in Q4-2017). However, the Fed’s mandate is employment and inflation, and indicators continue to suggest that the Fed is now basically at its mandate.

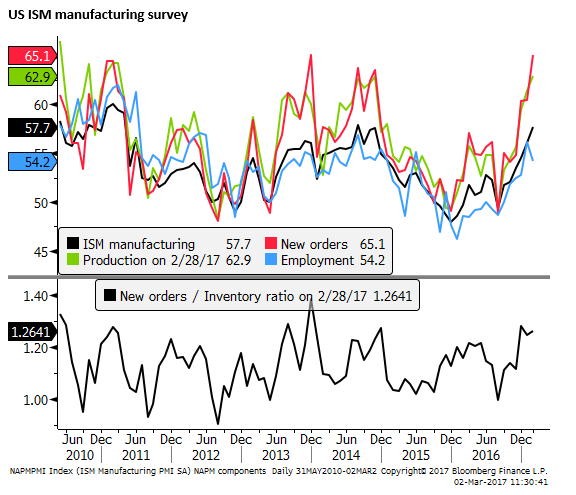

Furthermore, a range of other indicators suggest that activity remains buoyant. The ISM manufacturing index rose more than expected to a strong 57.7 in February, including a surge in new orders to 65.1, equaling the previous peak in 2013.

The Conference Board USA leading index was solid in Jan (+0.6%m/m), up 0.4% on average over the last three months, a high since Jun-2015. The Chicago Fed National Activity Index dipped a bit in Jan, but on average over the last three months it was very close to zero, suggesting growth running near trend, around the high since Sep-2015

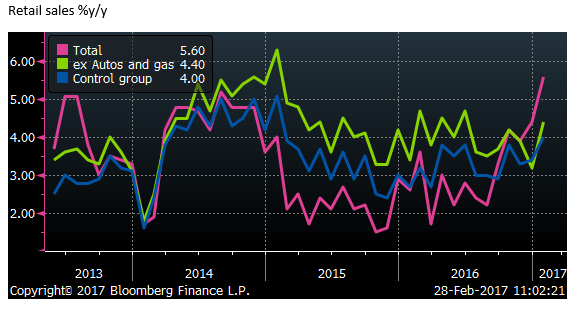

NY Fed President Dudley highlighted the significant rise in business and consumer optimism in surveys earlier in the week. The strong consumer confidence is consistent with the stronger the expected retail sale data in January.

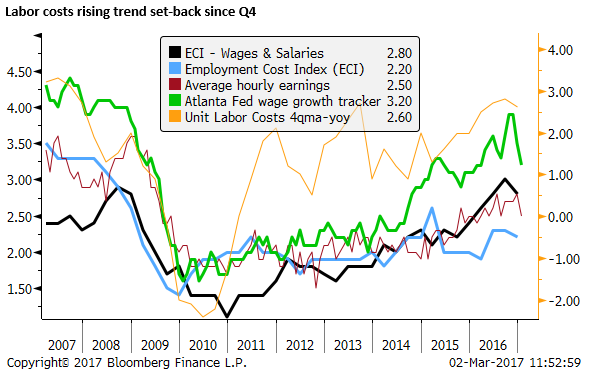

Labor market tightens

The employment report is due next week; it should continue to show a labor market close to full employment. Unemployment claims have fallen to a new record low on a four-week moving average. The Conference Board Consumer survey measure of ‘Jobs hard-to-get less plentiful’ remained around its low since 2007 (in net negative territory).

The most recent wages data for January were lower than expected, and showed some set-back in the rising trend. However, this data tends to be volatile, so we must be wary of it bouncing back in the February report due next week.