For the Fed July is the new June, RBNZ on hold in June

We think the market should get prepared for a July Fed rate hike that we rate as a better than 50% chance. By July the market will be clear of the Brexit vote that is likely to result in a stay-in outcome and avert global market instability. The stronger US retail sales and consumer confidence, and firm housing and CPI data suggest that the US economy is on track. The Fed may view July as an opportune time to deliver another small step towards normalizing policy without upsetting confidence and allowing scope to follow up in December, satisfying the majority of FOMC members’ March projections for two hikes this year. The prospect of higher US rates should tend to support the USD. Despite firming US rates, gold continues to exhibit a positive trend and may reflect more persistent bigger picture investment flows. In which case gold may be resilient to higher US rates in coming months, but we prefer gold against JPY, EUR and AUD. We do not see the path clear for the RBNZ to cut rates in three weeks in a meeting priced to be a close call, but we expect the RBNZ MPR to project lower rates and prevent a sustained bounce in NZD.

July in the new June for the Fed

The market pricing of a hike on 15 June was negligible last week, but has risen to a not insignificant 14% today in the Fed Fund futures market. We think that leaving rates on hold ahead of the UK Brexit referendum on 23 June makes sense and still see no hike in June.

The odds of Brexit are still modest in the betting market and have diminished a bit over recent months to less than 30%, but the opinion polls are still running at 50%. The event might be particularly unsettling to global financial markets and hard to predict. As such, waiting one more month on a policy decision is the prudent decision. There is also a contentious national election in Spain on 26 June and a meeting of oil ministers on 2 June, both potentially unsettling events.

The probability of a hike at the 27-July meeting (or before) is priced at 30% (up from only 20% earlier in the week). While in-between press conferences and FOMC projection dates, this FOMC meeting is well after the 23 June Brexit referendum. It will allow two more reads on the payrolls data.

A hike in July would be 7 months after the December hike and appear consistent with a gradual and cautious path and leave the Fed in a position to assess its impacts over a several months and still hike in December, fulfilling the projection of the majority of FOMC members made in March for two rate hikes this year. Quite a few FOMC members may see this as an attractive option.

There is a view that the Fed much prefers to change policy at the quarterly meetings that include press conferences and projections. As such, if it holds fire in June, then some people see the next real live date is September.

However, Fed members have often argued that every meeting should be considered live, and moving rates in July, subject to reasonable market stability, would be the perfect time to demonstrate that point. As such, July is a highly important meeting date and should be considered live. Like 40 is the new 30, July is the new June.

June meeting will still be highly anticipated

The 15 June policy meeting will still be highly anticipated with its latest FOMC projections and Chair Yellen press conference. She may choose to lay the ground-work for a hike in July depending on global financial markets stability. How the Fed presents in June will be crucial for market expectations for rate hikes and may be highly important for global markets.

Sending a signal of a probable hike in July will greatly lift the odds of a hike in December and lift the US yield curve.

Ambivalence without much guidance, continuing with a wait and see message, especially if the number of FOMC members looking for two hikes this year falls by several members, may weaken the dollar significantly, place upward pressure on gold and may support a variety of asset prices. In March there were 9 of 17 members projecting two hikes this year, only 1 projecting one hike, and the remaining 7 predicting three or four hikes.

In April, the FOMC was not under much pressure to test its outlook. At that time, it could remain ambivalent, without the scrutiny of updating projections, after a soft economic data in Q1 and significant global market uncertainty. Its members could maintain rhetoric saying two hikes were possible even probable this year if the economy strengthened as they anticipated.

However, the FOMC will be forced to be more precise and guide more clearly if it still sees two hikes this year.

A hike by Fed in coming months might help reduce uncertainty

Hiking in July might be regarded as a ballsy move with economic growth on a more moderate path, inflation still significantly below target on the Fed’s preferred measure and still significant global economic and financial market uncertainty. However, it may also be viewed as offering a sense of confidence in the outlook and providing reassurance to the market that the Fed has in mind a more certain path for rates, consistent with its gradual guidance.

A second hike in the current tightening cycle at this point is unlikely to appear particularly hawkish or significantly undermine asset prices and confidence. The US dollar has weakened this year and while it may rise again, if it goes too far, the Fed could use this as excuse to delay the third hike in its cycle.

The Fed will be able to decide on a hike in the light of economic conditions, and the early evidence is that activity may be improving from Q1, consistent with further progress to full employment and target inflation.

The CPI inflation data suggest inflation in underlying terms may still be trending higher. The Cleveland Fed weighted median CPI rose to a new high of 2.5% and the trimmed mean was stable at 2.0%. These core measures are already at or over the Fed’s 2% inflation target. The Fed’s preferred measure, the PCE deflator remains a significant margin below the CPI core measures, allowing the Fed to keep rates low for longer, but the overall picture suggests progress is being made towards raising inflation. The PCE data is due on 31 May.

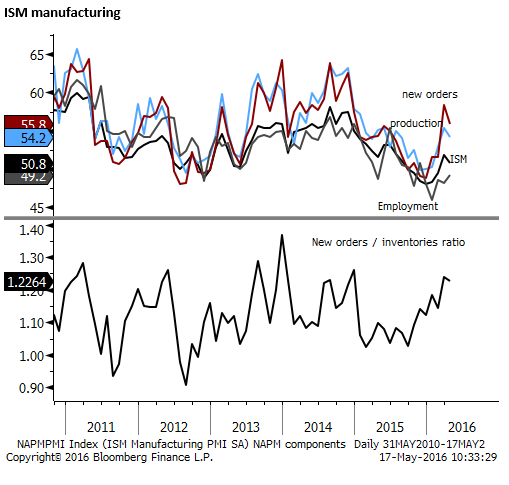

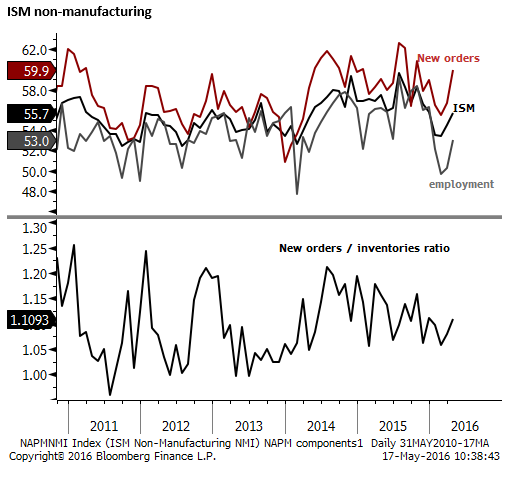

The US ISM indices for manufacturing and non-manufacturing have improved from the lows around the turn into 2016.

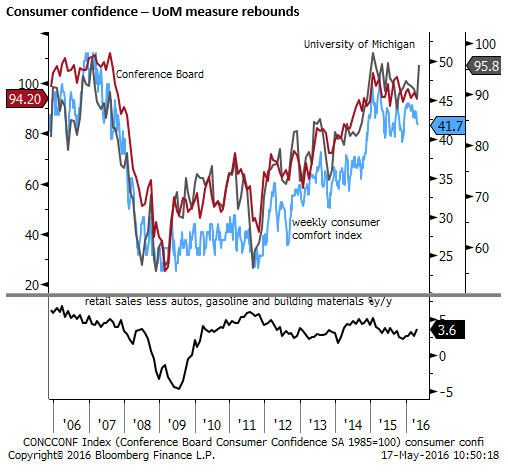

The Michigan University consumer confidence preliminary reading for May rose significantly more than expected. It sits above other readings of consumer confidence, and if repeated in other measures would suggest consumer spending, supported by solid income growth, will help drive sustained growth.

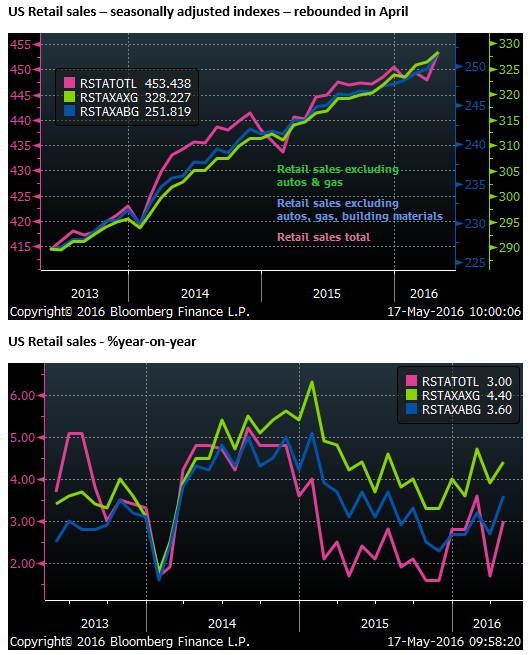

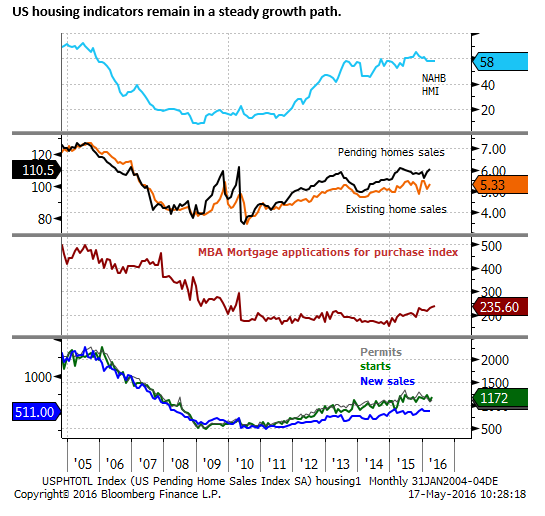

The domestic economic picture suggests that the economy is resilient, has coped with weaker global growth momentum and retained a moderate growth path. It should provide comfort to the Fed that it can make one more small step towards normalizing policy.

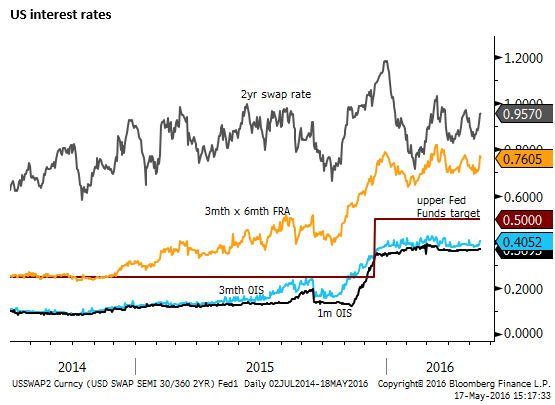

US rates have firmed in the last week since the payrolls report was lower than expected, in line with the rebound in retail sales. The retail sales and consumer confidence data this week may presage a trend towards firmer data in the months ahead, seeing a further rise in rate hike expectations and US front end rates.

It is interesting that despite a rise in US 2yr yields of 3.5bp on Tuesday and 6bp this week to a high since 26-April, the USD is largely unchanged against the EUR and JPY, gold is firmer and most emerging and commodity currencies are firmer. We can’t’ over-interpret moves from day-to-day, but the market is not sure that the USD should resume its rally on thoughts that the Fed is closer to raising rates.

This may in part still reflect the intense uncertainty over Fed policy direction. Even though the odds of a hike have lifted this week, a full hike is still not fully discounted by year-end.

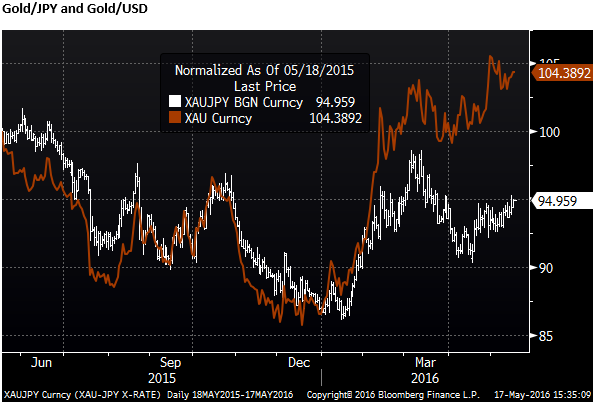

Gold may remain resilient to firmer USD

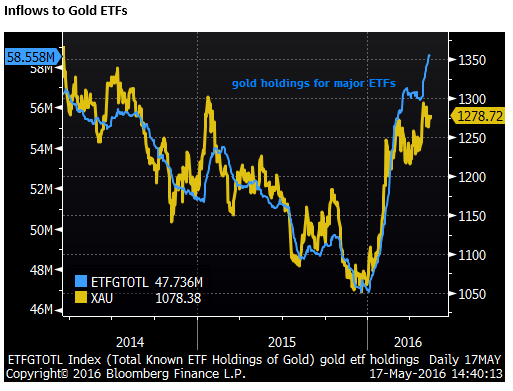

Gold has gained a lot of attention this year, with several high profile investors saying they have increased holdings of gold. George Soros is the latest to advertise his shift into gold, another is the one time manager of the Soros Quantum Fund, Druckenmiller. These big time investors are seeing gold as a safe haven against global monetary policy that is being pushed to its limits and asset prices that may be priced for perfection. Fears over debt vulnerabilities in China feature highly in this assessment.

Gold has reported to have benefited from significant inflows into gold related exchange trade funds. The chart below illustrates these flows. If anything, it is surprising that gold has not already pushed to new higher highs, judging by the interest that appears has been aroused.

Another factor that may boost gold is demand from China. There are mixed reports regarding demand from China, but capital outflow from China has persisted for almost a year, and the CNY exchange rate, while improving in Q1 against a weaker USD, may have resumed its downtrend that began spectacularly in August last year with a surprise devaluation. Chinese investors may also be seeking a more stable store of value and increasing demand for gold.

Gold has been grinding through a wide but still rising trend since rising sharply and breaking previous highs in February. As such, it is exhibiting a solid pattern and may prove resilient even if the USD were to strengthen on higher US rates expectations.

We continue to see upside potential for gold, but prefer to hold it against non-dollar currencies, including JPY, EUR and AUD as the prospect of higher US rates in coming months may keep gold/USD capped.

RBNZ may again may keep rates on hold pending new Debt-to-Income limits

One of the more contentious rate decisions pending is that in New Zealand on 9 June. The market is very close to seeing a 50% probability of a cut. We are leaning towards no change since the RBNZ may want to get its macro-prudential policy to contain excessive strength in its housing market sorted out first.

The odds of a cut had shortened to almost an 80% probability just ahead of the RBNZ semi-annual Financial Stability Report (FSR) released on 11 May, in which there was speculation that the RBNZ would set out plans to further tighten macroprudential measures aimed at curbing credit for housing.

The RBNZ certainly used the FSR to herald new measures, but had no details. In its press conference, The RBNZ governor and key officials suggested that they were working towards a new measure that would limit bank mortgages to a maximum ratio of household income (Debt-to-Income (DTI) ratio limits)

Such a measure could be quite effective in curtailing the growth in house prices in New Zealand. To date the RBNZ has used limits on Loan-to-Value ratios to contain house price growth. This has been effective, but may now have run out of puff in slowing demand. DTI limits may have a stronger and more lasting impact.

If so it may allow scope for the RBNZ to cut rates further, but it is unlikely that the RBNZ will be able to put enough flesh on this new macro-prudential policy tool in coming weeks to open the door to a rate cut at its next meeting. The most likely time for a further rate cut is September, by which time the DTI proposal could be largely formed. But even then the RBNZ must be close to implementing this policy otherwise it threatens to spur on mortgage credit growth ahead of the implementation.

Inflation at least stable and activity stronger

The recent economic and inflation data do not clear the path to a further rate cut in three weeks on 9 June. Low consumer price inflation remains an issue for the RBNZ that has been below target now for around 5 years, and it has been under increased political pressure to boost inflation. However, it at least appears that underlying inflation may have stabilized around 1.5% or a bit higher, and may have increased modestly by some measures over the last year.

The 2-year-ahead inflation expectations survey data fell sharply in Q1 to a new low of 1.63% and appeared to be a key factor in the RBNZ decision to cut rates again in March this year. The most recent data was little changed at 1.64%, and while still low, will be viewed as largely reflecting the most recent low levels of headline inflation that rose from a record low 0.1%y/y in Q4-15 to 0.4%y/y in Q1.

A variety of domestic activity indicators suggests that demand growth is running above potential, supported by rapid immigration and strong housing market.

The RBNZ see substantial risks in the global economy and economic and financial stability risks associated with low milk prices that are placing pressure on farm incomes. However, this does not appear to have had a significant enough drag on overall economic activity to trigger further policy easing.

RBNZ may use the June MPR to project lower rates and cap NZD

In the May 11 FSR the RBNZ said, “Imbalances in the housing market are increasing with house price inflation lifting again in Auckland, after cooling in late 2015 and early 2016 following new restrictions in investor loan-to-value ratios and government measures introduced in October.

“House prices have also begun increasing strongly in a number of regions across New Zealand, although house prices outside Auckland are generally much lower relative to incomes.”

“Dairy prices remain low with global dairy supply continuing to increase. Many farmers now face a third season of negative cash flow with heavy demand for working capital.”

In its April policy press release, the RBNZ disappointed some expectations that it would cut rate back-to back. But it retained its easing bias saying, “Further policy easing may be required to ensure that future average inflation settles near the middle of the target range.”

The market sees significant odds of a cut at the June meeting because it will be accompanied by a quarter Monetary Policy Statement and press conference. RBNZ likes to adjust policy on MPR dates, and it has eased policy each quarter since September last year.

However, activity indicators are more buoyant since mid-2015, global growth concerns and dairy prices are at least no worse than in Q1, inflation indicators are more stable and the housing market has resumed excessive growth.

One factor that might encourage the RBNZ to ease in June may be to avoid further strength in the NZD, especially against the AUD since the RBA cut rates in May. The recent strength in the NZD against the AUD is keeping the NZD TWI at an uncomfortably high level.

The RBNZ may be anxious to get inflation higher and be prepared to cut rates in June, while using moral pressure on banks to prepare for DTI lending restrictions before they are actually implemented. In doing so it may feel comfortable that a rate cut at this juncture might not further exacerbate house price gains.

Alternatively it could attempt to use its June monetary policy statement to further advance the notion of DTI limits and incorporate these into its forecasts; in which case it could use its policy statement to project lower rates. This may prevent any sustained rally in the NZD exchange rate and even dampen the exchange rate by enhancing speculation that the RBNZ will be in a clearer position to cut rates later in the year.

We think the second strategy makes more sense and anticipate no cut in June, but a clearer message in the MPR that a cut is forecast in September and perhaps further into next year.