Fed still has a keen sense that hikes are required this year

The rates and FX market is little changed after the Fed Chair Yellen speech that tended to confirm market expectations that the weak April/May payrolls data has dealt the summer rate hike a knock-out blow. A July hike is possible but only in the unlikely event that payrolls rebounds strongly in the 8-July report. The Fed has essentially stepped back into data-watching mode and needs to be convinced that the slowdown in the labor market is a temporary reaction to weaker activity and uncertainty early in the year. Nevertheless it still has a keener sense that hikes are required before year-end. Chair Yellen suggested she was not planning much change to her projections in the 15 June FOMC meeting, and we may find a hawkish tinge in the FOMC ‘Summary of Economic Projections’. Chair Yellen emphasized that policy is not on a pre-set course and the outlook remains highly uncertain. The USD has been wounded but the outlook at this juncture remains more unclear than usual. The Fed is more finely tuning into domestic economic outcomes readying for a hike should conditions keep on a moderate growth path. Notwithstanding recent weaker momentum, the labour market is seen as close to the Fed’s full-employment objective.

Payrolls sink the summer hike

The weak job US payrolls report on Friday was a significant shock to the market and it appears also to the Fed judging by comments made by Fed members in recent days, including Chair Yellen.

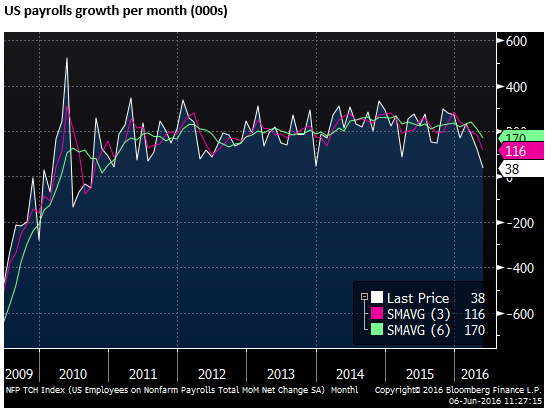

After a long run of relatively stable payrolls growth, the low May result (38K) and downward revisions to March (167K) and April (130K) suggest that the pace of growth may have significantly stepped down.

There have been a few one-off drops in recent years, and much depends on the next payrolls report. There is a chance that the low April and May results were outliers in the trend or a relatively short temporary pause.

However, the three-month average payrolls growth was 116K in May, a low since mid-2012, a period of significant global market uncertainty generated by the Eurozone crisis and a period of waning growth that preceded the third round of QE policy expansion by the Fed in late 2012.

There was the Verizon strike that appears to have dragged down payrolls by around 35K in May, and thus the result might be expected to bounce back by this amount above the underlying trend in June. As such the result is somewhat less alarming than the May result suggests. But at this stage the market needs to weigh the odds that the pace of job growth has fallen to a rate that no longer leads to further tightening in the labor market.

The July payrolls report due on the 8th (after the ISM reports, mfg on 1-July and non-mfg on 6 July, and after the 14/15 June FOMC minutes on 6-July), takes on increased significance for the near term outlook for monetary policy.

Mixed labor market indicators

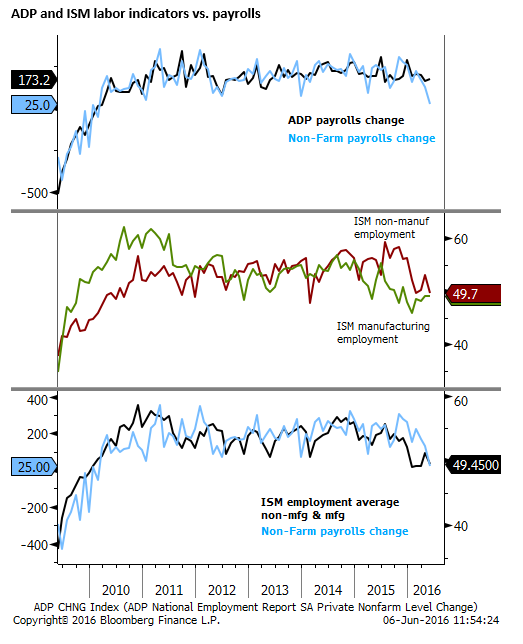

One predictor of the government payrolls report, the ADP employment report, released a day or two ahead of the payrolls, did not predict the fall in non-farm payrolls. It rose a bit in May to 173K, and it suggests that payrolls may rebound next month.

However, the fall in payrolls is consistent with the drop in the ISM purchasing managers reports. The chart below shows the employment components of the manufacturing and non-manufacturing ISM reports.

The May non-manufacturing ISM report was released after the payrolls report on Friday and was also significantly lower than expected, including a fall-back in its employment component to 49.7 in May, revisiting its low in February. The three-month average of the employment component is around its lows since 2010.

The chart below shows the average of the two ISM employment components comparted to the change in non-farm payrolls. Payrolls growth in recent months has slipped back in line with the ISM employment components, which remain around their lows since 2010. They suggest that the drop in the payrolls growth in recent months may be slow to rebound in coming months, diminishing the scope for Fed rate rises.

The Fed’s own broad indicators are telling different stories

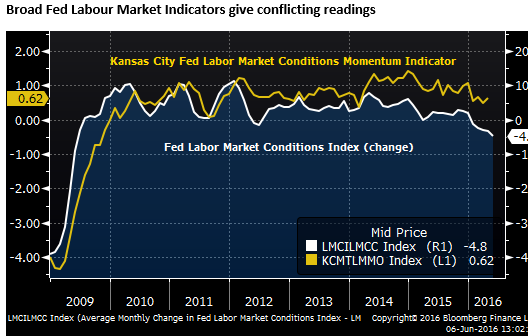

The Federal Reserve’s Labor Market Condition Index (LMCI), reported on Monday, a weighted average of 19 indicators and therefore a comprehensive overall read on the state of the labour market, fell 4.8 points, its largest fall since May-2009, the fifth fall in a row, suggesting the momentum in the labor market has been slowing all year at an increasingly deteriorating rate.

However, this indicator of labor market conditions is significantly weaker than an alternative broad-based model developed by the Kansas City Federal Reserve, a weighted average of 24 indicators called their Labor Market Condition Momentum Indicator (the most recent data point in for April).

It is interesting that two different groups of Fed researchers have developed models with considerable overlap in their dependent variables that give quite different readings on the current state of the labor market. The LMCI suggests labor market conditions may be outright deteriorating, but the KCFLMI suggests it may still be improving albeit at a slower pace than last year, still around its average rate since 2010. (Chart below)

Close but not quite there

Before the May labor market report, the state of the labor market appeared to be approaching and getting quite close to full-employment. The Fed’s June Beige Book released on Wednesday last week said, “Employment grew modestly since the last report, but tight labor markets were widely noted in most Districts.” The media reports of Fed comments suggested that most were prepared to hike in coming months (June or July).

However, the May employment data suggests improvement may have stalled close to full employment, but perhaps not quite there.

Some parts were still strong or stable. The unemployment rate fell to the low side of the 4.7 to 5.0% range considered to be the long run tendency, essentially ‘full employment’, in the March FOMC Summary of Economic Projections.

However, this was entirely driven by a fall in the participation rate that has fallen in the last two months after rising encouragingly from a record low in Sep-2015 over the preceding six months.

The U6 under-employment rate that tends to move concurrently with the unemployment rate and captures those marginally attached to the labor force or employed part-time for economic reasons was steady at 9.7% albeit at a low since 2008. (It is still some-what above the average from 1995 to 2007 and might be considered still above normal)

Some weaker leading employment indicators

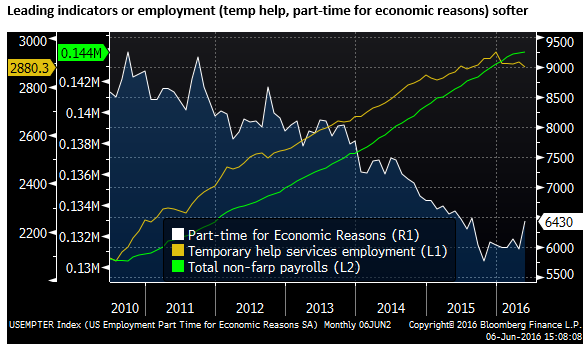

Some leading indicators of total employment have weakened in recent months. ‘Temporary help services’ jobs fell 21K in May after rising 5K in May, and have been down four out of the last five months. ‘Employed part-time for economic reasons’ also rose 468K in May. Both indicators suggest the underlying demand for labor has weakened.

Fed Chair Yellen back to data-watching

In her comments today, Fed Chair Yellen, said, “I believe we are now close to eliminating the slack that has weighed on the labor market since the recession”…but that, “Recent signs of a slow-down in job creation bear close watching”.

She spoke extensively on the state of the labor market, noting evidence that it is close to full employment, and measures that suggest it retains underlying moment. She said:

“Job openings rate was at a record high in March, and the quits rate–the share of employees voluntarily leaving their jobs–has moved up and in March stood close to its pre-recession levels. The increase in the quits rate is a sign that workers are feeling more confident about the job market and are likely receiving more job offers.” (JOLTS job openings report for April is due on Wednesday)

“Average hourly earnings for all employees in the nonfarm private sector increased 2-1/2 percent over the past 12 months–a bit faster than in recent years and a welcome indication that wage growth may finally be picking up.” (On Friday, earnings rose 2.5%y/y, as expected, unchanged from April).

“Other timely indicators from the labor market have been more positive. For example, the number of people filing new claims for unemployment insurance–which can be a good early indicator of changes in labor market conditions–remains quite low, and the public’s perceptions of the health of the labor market, as reported in various consumer surveys, remain positive. That said, the monthly labor market report is an important economic indicator, and so we will need to watch labor market developments carefully.”

Summer hike requires sizeable rebound in June payrolls

However, while remaining cautiously optimistic, it does appear Yellen prefers to gather more information on the state of the labor market and economy in light of the weak April/May employment reports. This suggests that the timing of the next rate hike will depend crucially on upcoming payrolls reports. At a minimum a 15 June hike appears now off-the-table and a 27 July hike may only be possible if the June labor report rebounds back to the trend in 2015 and early this year.

The probability of this is diminished in light of the recent mixed labor indicators discussed above, consistent with the current pricing in the Fed Fund futures market that has dropped the probability of a hike by the end of July to 22% from over 50% just ahead of the May payrolls report.

The Fed still has a keener sense that hikes may be required before year-end

Fed Chair Yellen can see that there may have been a temporary slow-down in employment growth related to weaker activity in Q1 and financial market uncertainty. But economic conditions may now be returning to a more robust outlook. As such, she remains cautiously optimistic that labour data will improve in coming months. But she also acknowledges a risk that it may take longer to rebound. As such, the timing of the next rate hike has become more data-dependent and the Fed is back in ‘watch and wait mode’, albeit with a keener sense that a hike may be required relatively soon (if not as soon as June or July).

Yellen said:

- “If the May labor report was an aberration or reflects a temporary slowdown resulting from the weakness in economic activity at the start of the year, then job growth should pick up and support further gains in income.”

- “Business investment has been weak in the past six months or so, even beyond the energy sector, and investment in capital equipment is reported to have declined in the last quarter of 2015 and first quarter of this year. I suspect there is a transitory element to this weak investment performance, and I expect investment to rebound. But the latest labor market data raise the less favorable possibility that firms may instead have decided to expand their operations more slowly, and I intend to continue to pay close attention to developments in this area.”

- “So an important question is whether the U.S. economy could continue to make progress amid fairly considerable global bumpiness. I continue to think that the answer to that question is yes, but the weak investment performance in recent months is concerning, and Friday’s employment report provides another reminder that the question is still relevant.”

- “One development that could shift investor sentiment is the upcoming referendum in the United Kingdom. A U.K. vote to exit the European Union could have significant economic repercussions.”

No pre-set course and uncertainty high

A message that Chair Yellen tried to impart in this speech, was to emphasize that the Fed does not have a pre-set course and much depends on the data and is subject to considerable uncertainty over the path of the US and global economy. There was no reference to a hike appearing appropriate in coming months, a theme that had been implanted in several Fed comments over previous weeks.

She said:

- “Monetary policy is not on a preset course and significant shifts in the outlook for the economy would necessitate corresponding shifts in the appropriate path of policy.”

- “An important theme of my remarks today will be the inevitable uncertainty surrounding the outlook for the economy.”

15 June FOMC projections may have a hawkish tinge

While a hike appears off-the-table, an important consideration for the 15 June policy meeting will be what the ‘FOMC Summary of Economic Projections’ project for interest rates. Will it still have the same number of members projecting two hikes this year? Will it retain the same longer run outlook for neutral rates?

In the March FOMC meeting, rates forecasts were lowered significantly, contributing to the dovish market reaction to that meeting, and the trend for some time has been downward revisions to the FOMC’s long run outlook for rates.

Nevertheless, In March, nine of 17 members still projected two hikes in 2015 and only one projected one hike, with 7 projecting more than two. The market has consistently and correctly been biased towards expected fewer hikes than the Fed, and it still has only 20bp of hikes priced-in by year end, less than one-full hike. Again it finds itself far below the last set of Fed projections.

While the May payrolls report, combined with mixed activity indicators this year, suggests that the Fed is no longer so sure about hiking in coming months, it may not have stepped back from seeing risks leaning towards two hikes this year.

Yellen said, “Next week, concurrent with our policy meeting, the FOMC participants will release a new set of economic projections. Those could, of course, differ from the previous set of such projections in March. But speaking for myself, although the economy recently has been affected by a mix of countervailing forces, I see good reasons to expect that the positive forces supporting employment growth and higher inflation will continue to outweigh the negative ones. As a result, I expect the economic expansion to continue, with the labor market improving further and GDP growing moderately. And as I just noted, I expect to see inflation moving up to 2 percent over the next couple of years.”

This suggests that most Fed members will not be changing the forecasts since March, in which case the FOMC projections may have a more hawkish tinge than expected by the market.