FOMC to consider but not commit to summer hike, BoJ to cut again

The market appears prepared for the Fed to revert to a ‘nearly balanced’ risk assessment. We are not looking for a big reaction to this outcome. It might give the USD a modest boost by implying that a hike in the summer is being considered, but a hike by July (after the Brexit vote) is 40% priced-in and thus already seen by the market as a significant possibility pending still considerable global and domestic uncertainty. We expect a comprehensive set of policy easing measures by the BoJ on Thursday. This will need to include a further rate cut to sustain recent gains in the USD/JPY. Notwithstanding the backlash against the rate cut and NIRP in January, the BoJ and Kuroda appear to have warmed the market up to this outcome, linking it to their desire for a weaker JPY. We think Kuroda and the BoJ plan to deliver a significant rate cut in conjunction with a large increase to its asset purchases aimed in part to at least stabilize the JPY over the medium term. We predict a further near term rise in USD/JPY towards the high end of a 110/115 range. As discussed in our report on 19 April, we see the RBNZ on hold but retaining an easing bias.

40% odds of a Fed hike in June or July

It’s widely agreed that the FOMC will not change rates on Wednesday, appearing to as much as ruled this out at its dovish March policy meeting. But the market is still hanging on every subtle word change in the statement for hints that the Fed may move at its June 15 policy meeting.

Fed fund futures suggest that the market is pricing in only around 16% chance of a 25bp hike in rates in June, and a 40% chance that rates are hiked 25bp in either June or July. This assigns a significant chance that the Fed chooses to hike in July over June, even though July is between the quarterly revisions of FOMC projections and Chair press conferences where policy changes are generally preferred, especially in a gradual policy agenda.

The reason for the unusual increase in odds between June and July probably reflects the proximity of the UK Brexit referendum on 23 June, not long after the FOMC June meeting. The market thinks that even if the Fed might be inclined to hike in June, it would consider holding off six weeks to wait for the outcome of the UK referendum.

Fed Fund futures suggest that the market is pricing in about a 64% chance that the Fed has raised rates by 25bp by the September 21 FOMC meeting.

The market pricing currently expects Fed fund futures to be around 61bp by the end of the year, placing it 24bp above the current rate (suggesting it sees about one rate hike for the rest of this year).

This might seem low compared to the two Fed hikes projected by the FOMC. However, the market has long been below the FOMC projections and the uncertainty is clearly skewed to less rather than more given the risk of some financial or other crisis throwing the Fed of course, as has occurred over the last year.

A 40% chance of a 25bp hike in June or July suggests that the market believes that the Fed will signal at its meeting this week that it is keeping its options open for a hike in the summer. We tend to agree and see limited scope for a significant rally in the USD on this outcome.

Nearly balanced

Most commentators are waiting to see what the Fed says about the ‘balance of risks’. The FOMC dropped from its statement in January an assessment of the ‘balance of risks’. It said instead that, “The Committee is closely monitoring global economic and financial developments and is assessing their implications for the labor market and inflation, and for the balance of risks to the outlook.” This suggested that uncertainty over the outlook meant that the Fed was more likely to stay pat for longer.

In March, the Fed again decided not to make an assessment of the balance of risks. But it said, “Global economic and financial developments continue to pose risk”. The implication was that the Fed was still on hold at least through the April meeting.

The Fed raised rates for the first time in the post crisis era in December last year and the statement said, “The Committee sees the risks to the outlook for both economic activity and the labor market as balanced”

In most meetings in 2015, ahead of this December rate hike (that appeared to be delayed several times from around the middle of the year due to a rising USD, increasing global uncertainty and a weakening energy sector) the FOMC statement said, “The Committee continues to see the risks to the outlook for economic activity and the labor market as nearly balanced but is monitoring global economic and financial developments.”

The market for the most part appears to expect the Fed to revert to this “nearly balanced” assessment.

If it fails to re-instate these words, the statement might be seen as dovish. On the other hand, if it says the risks are fully “balanced” this will be seen as much more hawkish that expected and will see the odds of a hike in the summer rise to be almost fully priced-in.

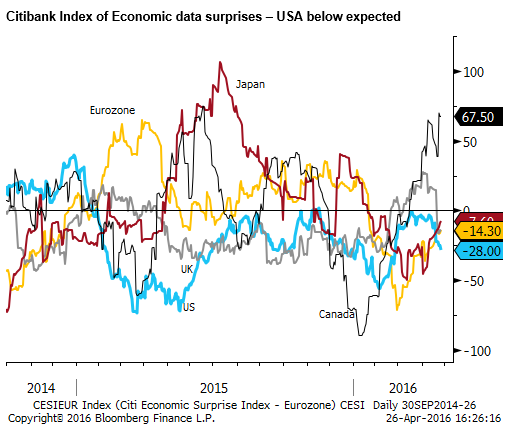

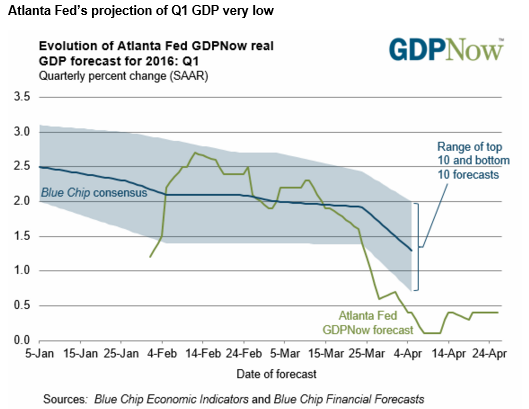

The economic data since March has been weaker than expected, with the one exception – the labor market appears to have tightened further judging by new lows in unemployment claims and a modest uptick in wage growth trends.

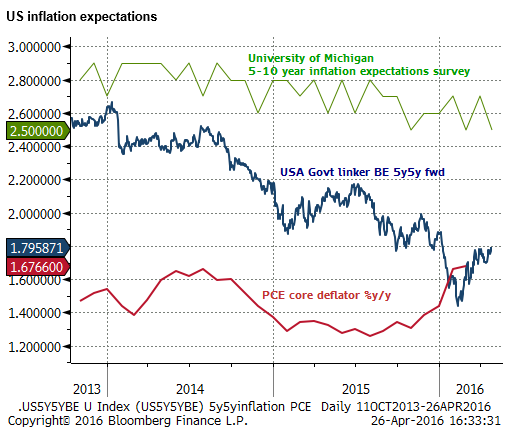

Surveys of inflation expectations have remained low, although market-based measures have improved from low levels.

Measures of financial market stress have eased substantially and overall monetary conditions, including a weaker USD, stronger equities and lower long term yields and credit spreads, have eased significantly. These factors might encourage the Fed to see the downside risks to their outlook substantially reduced.

However, in the context of the relatively recent recovery from a weak first two months for global asset prices, still overall high levels of volatility, the pending Brexit vote, ongoing high uncertainty over policy and economic direction in China, relatively weak global growth forecasts, and excess supply for major commodities, it does not feel like the time to signal the all clear of global conditions.

As such, we doubt the Fed want to do more than open the door to a second rate hike provided domestic and global economic conditions improve further.

Japan to ease policy across all dimensions

In contrast, the bar is set reasonably high for the BoJ to deliver sufficient easing to further weaken the JPY. It may be the case that it will have to cut rates further and expand bond purchases to drive JPY any weaker.

There has been a considerable turn around for the JPY and expectations for the BoJ. Only a week or so ago, many doubted that the BoJ would ease policy this week in the wake of the severe backlash over its surprise introduction of negative interest rates policy (cutting rates by 20bp from +10bp to -10bp) on 29 January.

Weaker bank stocks, a stronger JPY and weaker consumer and business confidence, seemingly in response to the NIRP, made many doubt that the BoJ will cut rates further, although some thought that the BoJ might revert to its previous approach of expanding its asset purchases to ease policy this week.

However, reports late last week from un-named officials that the BoJ was considering offering loans to banks at negative interest rate to support bank lending, aimed at alleviating some of the unwanted side effects of negative rates, appears to open the door for the BoJ to cut the policy rate further.

Even though the JPY strengthened after the NIRP policy in January, a further rate cut this week as part of a comprehensive set of policy easing measures would be aimed at weakening the JPY, giving rates across the curve scope to fall further below zero.

BoJ Governor Kuroda and other un-named officials expressed their concern over a strengthening JPY last week, further suggesting they may include a rate cut in a wider set of measures.

The BoJ’s use of shock tactics with respect to the NIRP in January failed to trigger the desired response of a sustained weakening in the JPY. With respect to this policy tool, last week the BoJ instead appears to have fed expectations aiming this time to build a link between a weaker JPY and NIRP, such that delivering a rate cut might propel the JPY lower, or at least limit its advance.

The stage appears set for the BoJ to deliver comprehensive policy easing across all policy tools, expanding the size and scope of asset purchases and a further cut in the policy rate.

In terms of the most direct influence, cutting rates and increasing government bond purchases together should tend to weaken the exchange rate. However, increased purchases of exchange traded stock funds, REITS and corporate bonds might have the reverse effect, tending to boost domestic asset prices potentially generating a positive response on the JPY exchange rate.

As such, if the BoJ fail to cut rates, and place greater emphasis on increasing purchases of ETS and REITS, then JPY might rally.

Placing more emphasis on higher government bond purchases might place some downward pressure on the JPY, but to ensure the JPY weakens the BoJ probably needs to also cut rates further.

In light of the Kuroda’s concern over a stronger JPY we presume that the policy decision on Thursday will include a further rate cut and a significant slug of increased bond purchases along with increases in ETF and REIT purchases.

Overall, even if Kuroda delivers a rate cut, the market is likely to remain cautious in buying the USD/JPY. After its sustained fall since mid-2015, accelerating this year, sentiment has more permanently shifted towards the JPY.

The Asia Nikkei news reports that the GPIF is now actively looking to hedge its foreign asset exposure. And exporters are now looking to hedge export earnings. The BoJ’s Kuroda now faces a more up-hill battle it driving the JPY weaker.

GPIF to embrace currency hedging: president – Asia.Nikkei.com

Yen underpinned by exporters buying forward contracts – Asia.Nikkei.com

While Kuroda may not have the capacity or desire to shock the market this time around, he may still adopt the tactic of over-delivering to attempt to spark a more sustained and positive response to the BoJ’s policy decision. As such, we expect a comprehensive set of measures all significant in size and some further recovery in USD/JPY moving it to the high side of a 110/115 range.