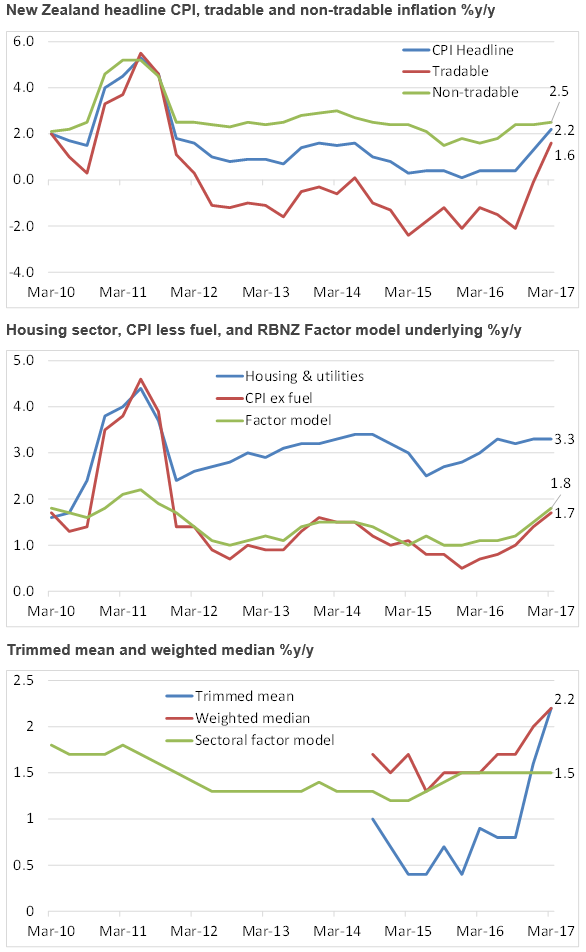

Inflation impulse picks up in New Zealand; The RBNZ will need to revise up its dovish policy guidance

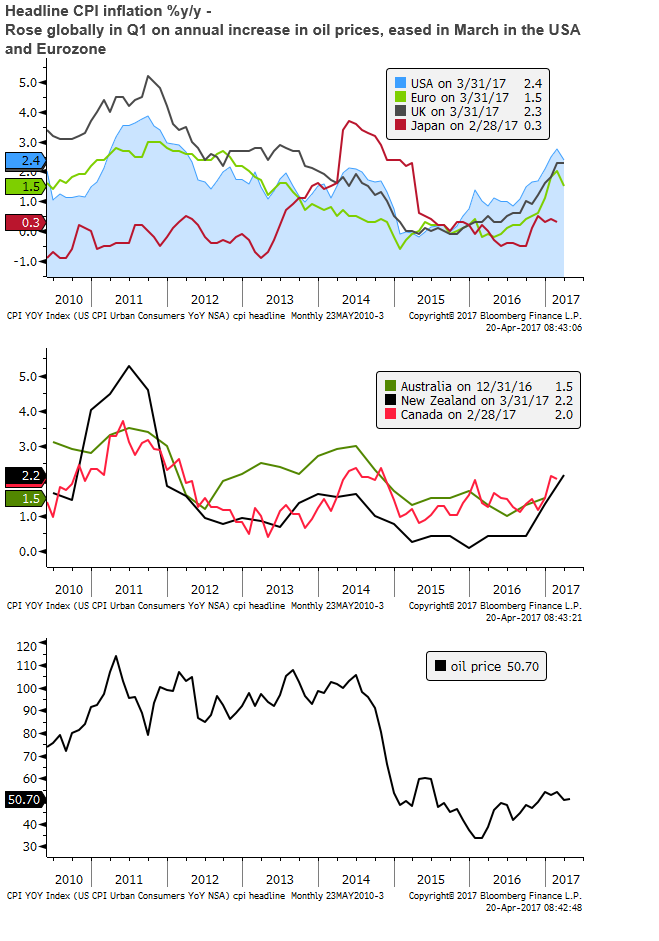

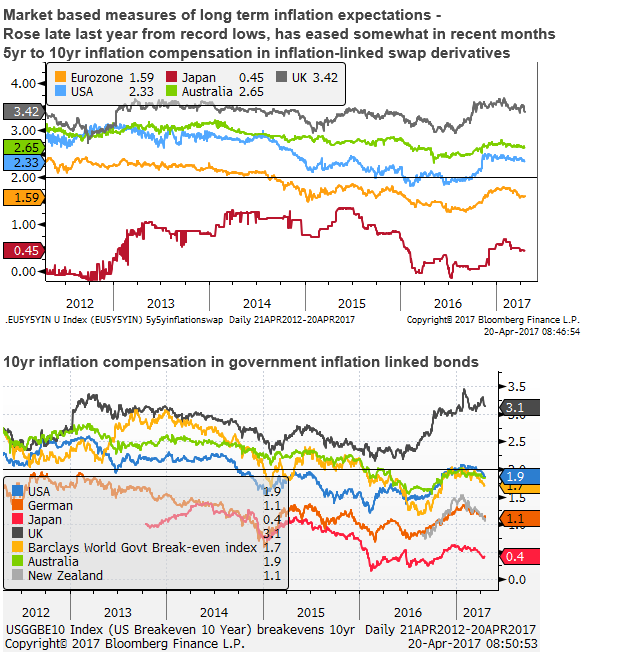

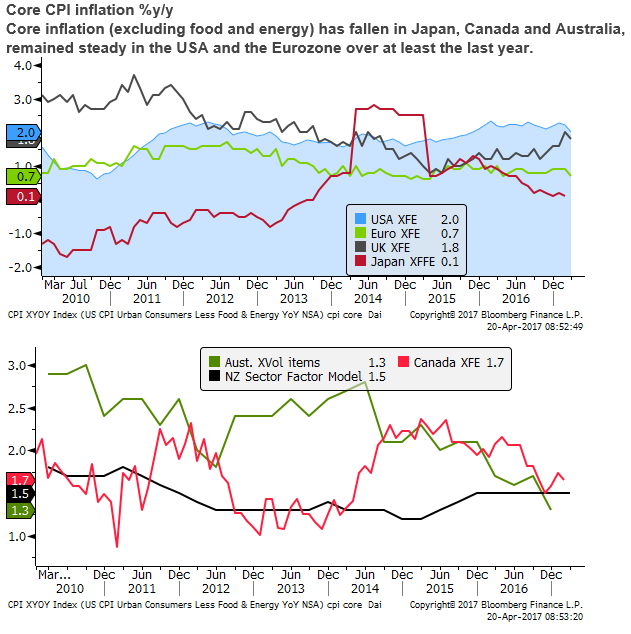

New Zealand experienced a rebound in headline inflation in Q1, consistent with the global trend and higher oil prices from a year earlier. More recent inflation data from the USA and Europe has eased, along with some flattening in oil prices and still subdued core inflation trends. Market-based measures of longer-term inflation expectations have also eased in recent months. However, underlying inflation measures were broadly stronger in New Zealand and have been improving, albeit from low levels, for over a year. A rising underlying inflation trend is consistent with several years of above-trend demand growth and a tight housing market. The inflation and growth momentum in New Zealand, improved global growth outlook, and firmer dairy prices suggest that the RBNZ’s low and stable rates guidance needs to be revisited at its 11 May policy meeting. It may continue to hold rates steady in coming meetings given it is only just getting inflation on target after a prolonged period below target. It will also remain comforted that wage inflation remains low, although attention will fall on the Q1 labour market data on 2 May. The RBNZ will continue to call the NZD too high, but it is hard to argue for a fall in the near term unless driven by global developments. The market is also looking for a sizeable rebound in Australia’s CPI inflation next week. Some recovery is likely after surprisingly low outcomes last year. However, the inflation impulse was still hitting its lows in 2016 and lagging New Zealand by at least a year. The moderate growth outlook in Australia suggests underlying inflation may take longer to clearly start to recover from record lows. AUD has struggled recently with lower iron ore prices and increasing public anxiety of the housing market. AUD may appear somewhat more vulnerable than the NZD given its lower inflation impulse. However improving global growth indicators, led by China, also provide support for the AUD.

New Zealand headline inflation rebound in Q1 follows the global trend

Inflation has returned in New Zealand. The headline inflation rate of 2.2%y/y in Q1, above 2.0%y/y expected, was the first reading above the RBNZ inflation target of 2% since 2011, and since 2009 excluding the hike in GST in 2011.

Many countries experienced a rebound in inflation in Q1 driven by higher oil prices from year-ago levels. However, a number of countries, including the USA and Europe, experienced a dip in inflation in their March data. Oil prices have stabilized since December and are somewhat lower recently. And market-based measures of inflation expectations have fallen somewhat in the last month.

As such we must be careful over interpreting the rebound in NZ inflation In Q1. There were also a few other factors that boosted the result – tobacco tax increase and higher fresh food prices. Excluding food and fuel, the CPI rose 1.6%y/y, unchanged from Q4, but up from 1.0%y/y in the first half of 2016.

However, several core inflation measures have accelerated and suggest inflation is returning to its targeted zone faster than expected. And the tobacco excise tax is set to be raised 10% annually three more times over the next few years, and it follows a similar hike in Q1 last year, so it is hard to see it as a one-off.

New Zealand core inflation picks up

Non-tradable inflation, less affected by the vagaries of the exchange rate and oil prices and more indicative of underlying domestic inflation pressures edged higher to 2.5%, a high since Q3-2014; up from a low of 1.5% in Q3-2015, above the 2% inflation target.

The housing sector continues to drive up inflation. This sector that includes rents, newly build houses excluding land value, maintenance, housing services and utilities, rose 3.3%y/y in Q1, stable at this high rate for the last year.

Fuel accounts for a large share of the rebound in tradables inflation (+1.6%y/y, a high since 2011). But the CPI excluding fuel still rose 1.7%y/y, also a high since 2011.

The 10% trimmed mean underlying measure jumped from 1.6%y/y in Q4 to 2.2%y/y in Q1-2017, above the RBNZ 2% inflation target. The weighted median also jumped to 2.2%y/y

The RBNZ produces several statistical models of underlying inflation. The “Sectoral factor model” was steady at 1.5%y/y, steady at this rate since Q4-2015, up from its lows of 1.2% in Q4-2014/Q1-2015. However its “Factor model” underlying measure rose to 1.8%y/y a high since 2011.

The Sectoral factor model that was steady at 1.5%y/y is also broken down into core nontradables and core tradables. The nontradables core component rose to 2.6%y/y, revisiting highs in Q1 and Q2 last year. Further indication that this most stable underlying measure is also exhibiting uplift in domestically driven prices.

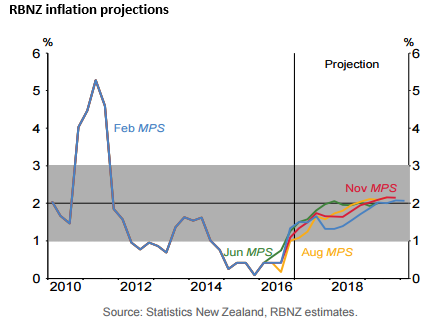

RBNZ inflation and rates outlook will need significant revision in May

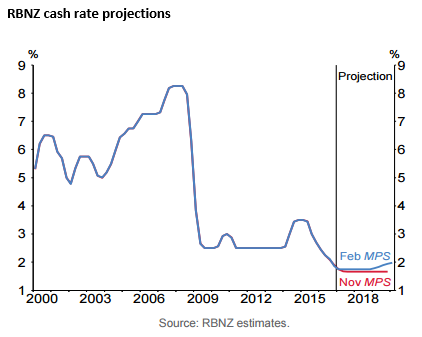

The RBNZ effectively moved to a neutral policy stance after cutting rates in November last year to a new record low of 1.75%.

Two rate cuts in late 2016 were enabled by tighter and broader restrictions on housing loan to valuation ratio (LVR) limits, designed to cool the property market, enacted in October 2016.

The rate cuts were aimed primarily at lifting inflation that had remained below target for several years, despite solid economic growth.

The RBNZ feared that the prolonged low level of inflation would more permanently lower inflation expectations, and they were under increased political pressure to achieve their inflation mandate.

The stubbornly high NZD exchange rate, despite rate cuts in recent years, contributed to low tradables inflation; dragging down overall inflation and arguably inflation expectations. The RBNZ NZD trade-weighted index rose to a recent peak in early-Feb this year. It eased modestly in early-March (by around 4%)

In its 23 March policy statement, the RBNZ said, “The trade-weighted exchange rate has fallen 4 percent since February, partly in response to weaker dairy prices and reduced interest rate differentials. This is an encouraging move, but further depreciation is needed to achieve more balanced growth.”

On inflation, the RBNZ said, “Headline inflation has returned to the target band [1 to 3%] as past declines in oil prices dropped out of the annual calculation. Headline CPI will be variable over the next 12 months due to one-off effects from recent food and import price movements, but is expected to return to the midpoint of the target band over the medium term. Longer-term inflation expectations remain well-anchored at around 2 percent.”

In its 9 February MPS, the RBNZ forecast headline CPI inflation to rise from 1.3%y/y in Q4-2016 to only 1.5%y/y in Q1-2017 (well below the actual outcome of 2.2%y/y).

It did not forecast inflation to rise to above 2.0% until the last two-quarters of its three-year horizon (2.1%y/y in Q4-2019/Q1-2020). As such, the starting point for inflation is now much higher than it anticipated in February, and, importantly, it is the first time it has been at or above the 2% target in over 5-years.

As a consequence of this expected protracted period ongoing sub-target inflation, the RBNZ projected no change in its official cash rate projections for over two years, and only one full rate hike by the end of its three-year forecast horizon.

The market is projecting no change in the New Zealand cash rate at least through the next two policy meetings (11 May and 22 June). A full hike is not fully discounted in the market for around 12 months.

In the wake of these inflation data, the RBNZ will almost certainly bring forward the timing of its rate hike projections. We expect to also see a further moderate increase in market rates, increasing the odds of a rate hike sooner.

RBNZ is likely to raise its global growth outlook

In its 9 February quarterly monetary policy statement the RBNZ said, “There is significant uncertainty about the outlook for trading-partner growth and inflation, and risks remain skewed to the downside.” Their posture on global conditions remained subdued in their 23 March policy statement.

In recent months global economic indicators have continued to broadly improve. The IMF upgraded its global growth forecast somewhat, released earlier this week, and generally sounded more confident in this projection. It said, “Global economic activity is picking up with a long-awaited cyclical recovery in investment, manufacturing, and trade”. Growth was forecast to rise from 3.1% in 2016 to 3.5% in 2017 (up from an earlier forecast of 3.4%) and further to 3.6% in 2018. However, it continued to say there are “structural impediments to a stronger recovery” and the balance of risks are” tilted to the downside”.

The RBNZ too may feel more confident in the global economic outlook by the time it updates its forecasts. It next meets to decide on rates on 11 May, when they will also release a quarterly monetary policy statement.

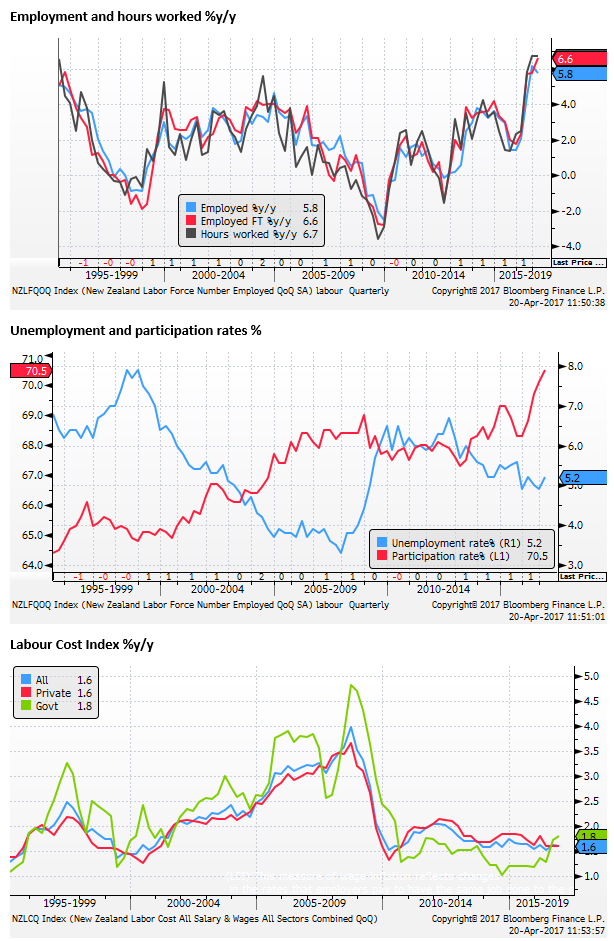

NZ Labour market very strong but wages still subdued

The rest of the world may appear to be catching up to the New Zealand growth outlook, but recent indicators suggest that New Zealand is maintaining its stable, strong, above-trend rate of growth.

One factor that may keep the RBNZ from pushing up rates too soon is that wages growth remains subdued. The most recent data is for Q4 last year, but there has been no apparent acceleration in wages growth for the last seven years.

The Labour Cost Index (LCI) that adjusts for compositional changes in employment has been rising at around an annual rate of 1.6%y/y for the last three years.

The labour market has exhibited strong employment growth over recent years, surging to a high of 5.8%y/y and 6.7%y/y in hours worked. However, rapid immigration and rising participation have prevented the labour market from tightening all that much. The unemployment rate was 5.2% in Q4-2017. It may be approaching full employment levels, but as yet there is no evidence of wage pressure.

The Q1 labour market data are due on 3 May, ahead of the RBNZ policy meeting on 11 May.

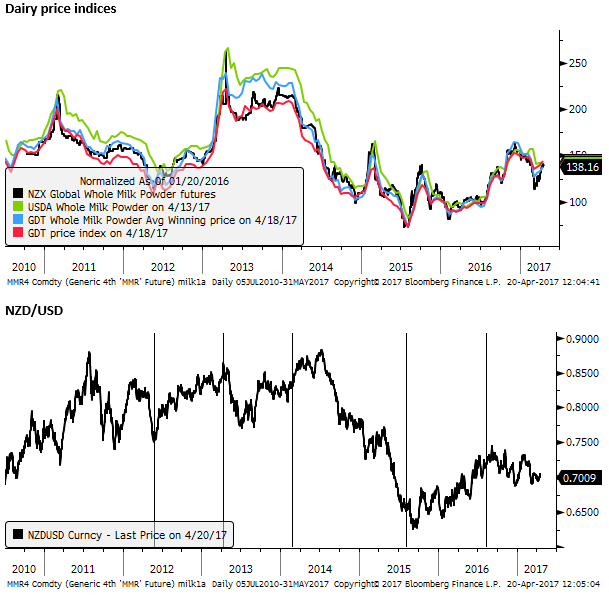

NZD remains too high for RBNZ, but milk prices have firmed recently

The other reason why the RBNZ may be reluctant to sound less dovish is for fear of placing upward pressure on the NZD exchange rate. On the other hand, it can feel a bit more comfortable that dairy prices have firmed recently

Having only recently seen inflation move back to target after a prolonged period below target, and some special factors that might contribute to a moderation in the coming quarters, such as a lower annual increase in fuel and fresh food prices, the RBNZ might not feel compelled to tighten in coming meetings. However, it is no longer clear cut that it can afford to maintain record low-interest rates for a prolonged period.

Does it point to faster inflation in Australia?

The Australian CPI data for Q1 is released on 26 April next week. Indeed, the market is anticipating a rise in the headline CPI from 1.5%y/y in Q4 to 2.3%y/y in Q1.

Note that the RBA target mid-point for inflation is higher than New Zealand and most advanced countries (at 2.5%) between a 2 to 3% target range. As such, an as expected rebound in inflation would still be below the target mid-point.

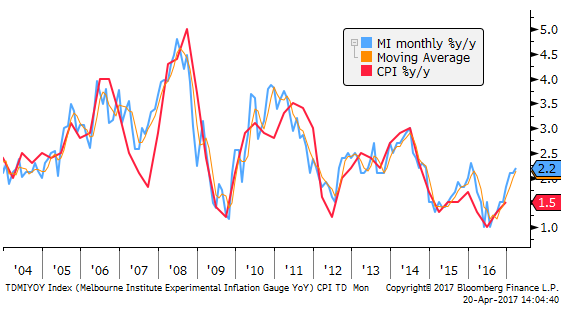

The Melbourne Institute monthly inflation measure of Australian inflation rose to 2.1 to 2.2%y/y in the first three months of this year, suggesting the government quarterly inflation measure might rise by the same amount (not quite as much as the median market expectation).

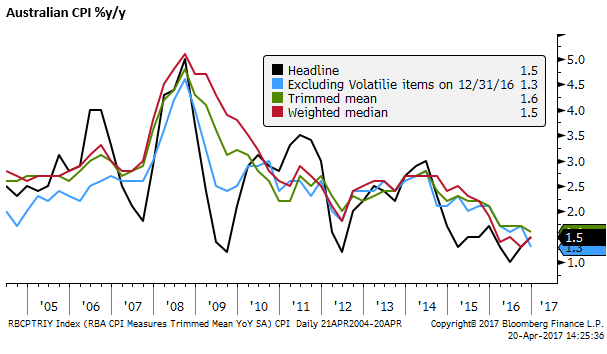

Inflation was surprisingly low last year and did contribute to two further rate cuts from the RBA. Underlying measures fell abruptly in Q1 last year on a much lower than expected outcome, and remained low with modest outcomes in the second half of last year.

The market is looking for some recovery in the underlying measures in Q1 this year, since they will be dropping out one of the lowest quarterly results on record from a year earlier in Q1-2016. However, the market is still projecting key core measures to remain below the bottom of the RBA’s 2 to 3% target range.

The median expectation is for the trimmed mean to rise from 1.6%y/y (a record low) to 1.9%y/y in Q1, and the weighted median to from 1.5%y/y to 1.8%y/y.

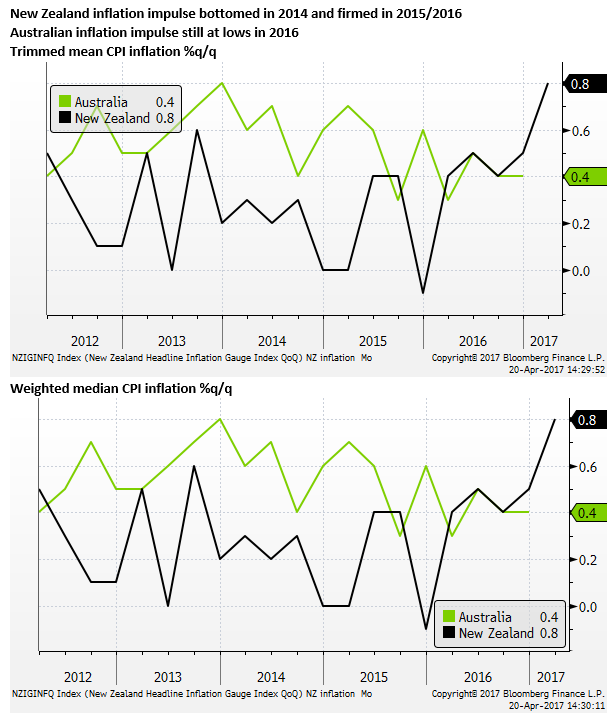

While there may be some bounce back in Australian inflation, it does appear that New Zealand inflation had begun to show more underlying improvement throughout 2016, albeit from a low base and gradually. Whereas Australia’s underlying inflation fell through 2016, and thus is lagging the cycle in New Zealand.

The slower inflation impulse in Australia compared to New Zealand is consistent with the persistently above trend growth in New Zealand in recent years. Australia has experienced a much more mixed set of conditions as it has been transitioning away from mining to other drivers of growth. Both nations have received much support from strength in their housing markets in recent years.

NZD and AUD exchange rates

The prospect of a less dovish RBNZ on 11 May suggests that the NZD may trade relatively strongly barring any renewed uplift in US yields and deterioration in global investor appetite.

We have argued in past reports that the NZD appears expensive compared to its narrowed yield advantage and would be vulnerable to rising global bond yields. The NZD has been mixed over the last nine months. It is unlikely that is will set a dramatically different course in the near term, but firmer rates and firm dairy prices suggest its base is firm for the time being.

NZD to follow US yields, RBNZ to stay out of the way; 21-Mar-2017 – ampGFXcapital.com

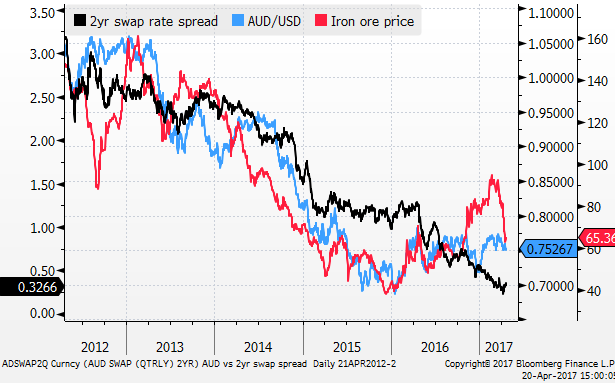

The rates outlook in Australia is relatively stable with mixed economic and inflation indicators, the RBA has indicated it intends to hold rates stable for some time barring significant surprises. The AUD may have been weaker recently due to increasing angst over the housing market and a retracement in much of last year’s rally in iron ore prices. However, with global growth indicators strengthening, led by strong growth in recent months in China, AUD too may hold its recent lows.

Housing angst helping cap AUD; 4-Apr-2017 – ampGFXcapital.com

The AUD/NZD has lost some ground recently, consistent with a somewhat lower 2yr swap rate spread and weaker iron ore prices, while dairy prices have firmed