JPY strength adds to global uncertainty and the case for gold

The rise in JPY is highlighting global risk aversion that may persist for several months. A key contributing factor may be increasing fear leading up to the Brexit vote, removing EUR as a potential save haven. While Japan may threaten intervention to prevent excessive and rapid moves in the JPY, few see this policy being used to draw a line in the sand. A strong JPY may induce more aggressive policy easing by the BoJ later this month, placing further downward pressure on global yields. The market will continue to doubt the Fed will hike rates even if its economy performs well in light of heightened global uncertainty. Low yields may tend to underpin global asset markets but choppy and directionless trading appears likely. The skittishness of global markets may increase volatility and make it difficult to trade with conviction on fundamental developments, perhaps leading to surprising and counterintuitive moves, including a deeper fall in USD/JPY. In this environment we continue to see a case for long gold positions.

Japan kicks an own-goal

There has been much virtual ink spilled on the sudden surge in the JPY. A good deal of it on what comments have been made by Japanese officials and the probability of FX intervention.

Leaving aside for the moment why the USD/JPY is falling anyway with negative yielding 10 year government bonds, gross government debt of 249% of GDP and net debt of 128% in Japan, since the BoJ/MoF failed to back-up its move to negative rates policy on 29 January with efforts to stem the rise in the JPY, the market has come to the conclusion that the Japanese authorities have shelved FX intervention more permanently.

Some thought that nearer 110 Japan might dust off the intervention tool; after all the JPY had reversed all of its fall against the USD since the 30 October 2014 BoJ policy bazooka was fired, and it had risen by around 13% from its high in 2015.

Furthermore, it could be argued that it had lived up to its part of the bargain with G20 to refrain from competitive currency devaluation. It could argue that the rapid rise in the JPY was moving into the realm of excessive volatility and disorderly movement that might justify FX intervention.

But alas this was not the case and after a period of consolidation above 110 for over a month since early-February, the USD/JPY lurched through this level in recent days.

A Wall Street journal article on 5 April quoted the Japanese PM as saying, “Whatever the circumstances, we must definitely avoid competitive devaluation, and I think we should refrain from arbitrary intervention in currency markets,” (Shinzo Abe Says Countries Must Avoid Competitive Currency Devaluations – WSJ.com). While he was presumably referring back to the G20 summit communiqué, by emphasizing this point at the time when USD/JPY was hovering above 110, suggested to the market that the Japanese government did not have its eye on the ball.

The policy goal-keepers back in Japan, officials at the MoF and Chief Cabinet secretary Suda, tried to save the own goal booted in by PM Abe with stock standard verbal intervention, but the market was understandably skeptical that they were yet close to actual intervention.

No line in the sand

Japan has not used FX intervention since 2011 (at that time using it to support the USD/JPY below 80). It has not needed to in recent years with its QQE policy since 2013 and 2014 contributing to a much weaker JPY. It probably hoped that adding NIRP on 29 Jan this year would be enough to keep the JPY relatively weak. However, it did not and the rapid rise in the JPY has the market wondering what now?

Policymakers in Japan may have felt that intervention was something they would hardly have to think about in an environment of supercharged quantitative policy easing, now with negative rates. In the mean-time the government and the MoF – chiefly responsible for intervention – aligned themselves with a hands-off currency intervention approach in coordination with the G7. All up Japan appears to have made a decision some time ago that aggressive FX intervention was not a viable policy option.

Some analysts have noted Japan may be less inclined to intervene at this time because it is hosting the G7 summit this year, kicking off with foreign ministers meeting on 10/11 April, ahead of a range of other ministerial meetings culminating in the meeting of finance ministers and central bank governors on 20/21 May and leaders on 26/27 May (G7 Summit – japan.go.jp). The IMF and World Bank annual gathering in Washington, USA is also starting next week, bringing together officials from the G20, sure to draw attention and caution on FX intervention activities (IMF/World Bank Spring 2016 Meetings – IMF.org)

As, such, even if they were to use intervention now to prevent an excessive rise in the JPY, the market would be skeptical of its resolve. Already many FX analysts on the street have been quoted arguing that invention might only provide a short term reprieve and have little lasting impact on the JPY.

There is no perceived line in the sand (exchange rate level) that the market expects the government to defend with FX intervention. It might expect the BoJ/MOF to use some intervention to prevent further sharp moves lower in USD/JPY, but it senses that their heart is not really in it. Perhaps nearer the 100 level the market might wonder of officials would consider setting up the barricades, but that is still far from clear.

More BoJ easing likely in response to a stronger JPY

While lacking credibility on intervention, the BoJ still has scope to ease monetary policy further and JPY strength is likely to firm up expectations of more decisive action at the BoJ meeting on 28 April. As the BoJ statement on 15 March reiterated, it will “take additional easing measures in terms of three dimensions — quantity, quality, and the interest rate — if it is judged necessary for achieving the price stability target.”

As such we should expect a further rate cut and more asset purchases. Certainly the economic activity and inflation data could justify more action and the rise in the JPY is likely to make this seem more urgent, especially if the government is reluctant to use FX intervention.

Losing faith in Abe/Kuroda

A key question is why the heck is the JPY so strong at this time when Japan is pursuing aggressive policy easing and prepared to ease further.

At some level it appears Japanese investors are no longer as convinced that Kuroda, Abe and the official establishment is so eager to achieve the 2% inflation target.

Japan is already doing a heck of a lot of asset purchases, it is generating some dislocation in the normal functioning of the capital markets with distortions generated by negative rates. Some officials and commentators are getting concerned that more QE and deeper NIRP would course more problems than they solve.

Others are wondering if Japan might be better off targeting lower inflation, say only 1%, thinking this may be more appropriate for a society that has low growth potential and is accustomed to falling prices. There is a sense among some folks in Japan that 2% inflation is not a feasible sustainable target.

There may also be a view developing in policy circles that QQE over several years has failed to fulfil its goals and the structural issues holding growth back have not been adequately broken down. They worry that yet further QQE/NIRP policy expansion will fail and instead they need to work harder to address structural rigidities and take the pressure of monetary policy.

The BoJ led by Kuroda is still saying it is prepared to go further to achieve its 2% inflation goal as soon as is practical, but there are creeping doubts that he is prepared to take a much longer view on achieving these goals and will not take policy to much greater extremes.

I don’t think Kuroda has given up on achieving inflation. I expect further decisive action as soon as 28 April. However, it would be understandable if he were becoming a bit jaded and hassled by the lack of success in raising inflation expectations and corporate and public actions in response to his already aggressive high-stakes policy action.

Global risk aversion and Brexit Fears

While the market has lost some faith in the Kuroda/Abe juggernaut that took the country by storm in 2012/13, a key reason for strength in JPY at this time is a lack of global alternative investments exacerbated by global risk aversion.

Japanese investors are reluctant to take on foreign exposure. Brexit fears may be playing a bigger role in discouraging capital outflow. GBP has been especially weak, and this may be spilling over to EUR and worries about Eastern European markets. Betting markets are placing the odds of Brexit going ahead at around 30%, polling is closer at around 50%, and there is heightened uncertainty as we approach the 23 June referendum.

The Brexit debate is channeling a deepening underlying dissatisfaction with cooperation among nations in Europe and even globally as popular support for trade barriers appears to be rising. If the UK were to pull out of the EU it may have wide-ranging implications for the EU and globally, increasing fears that the EU itself might be in peril and damaging confidence in global institutions ability to deal with future financial and economic crisis.

The G20 summit in Shanghai in February highlighted Brexit as a potential downside risk for the global economy in its communiqué. It said, “Downside risks and vulnerabilities have risen, against the backdrop of volatile capital flows, a large drop of commodity prices, escalated geopolitical tensions, the shock of a potential UK exit from the European Union and a large and increasing number of refugees in some regions.”

Some may argue that this is melodramatic and in or out of the EU, the UK, EU and global economy will move on. But anxiety is high, the GBP is already one of the weakest currencies and the EUR has stalled as JPY has continued to rise. EUR/JPY has dropped back sharply in recent days.

Big Japan institutional reallocation to foreign assets is over

The rise in JPY since mid-2015 reflects a sustained and increasing level of global risk aversion, but it also comes after the big financial institutions including the Japanese Government Pension Investment Fund have largely completed a major reallocation of its funds to foreign equities and bonds. This outflow probably contributed to a weaker trend in JPY in 2014 and early 2015, driving JPY into an essentially oversold position. With this flow largely spent, Japan is lacking a clear and sustainable capital outflow. As such the JPY may now be reverting to an underlying stronger trend.

Foreign investors that bought into the Kuroda/Abe agenda for inflation and structural reform and amassed large long Japan equity/short JPY positions since 2013 may also be in the process of squaring these positions up.

The persistent and now rising trend in JPY essentially since mid-2015 is making it hard to stick with a short JPY positions even if you retain faith that QQE/NIRP will eventually work. As such big picture fundamental views for a weaker JPY are being closed down.

Hardwired home bias

Japanese investors still appear to have a hard-wired home bias that has come back to dominate. Even as the Japanese economy and inflation appears to have stalled, making it seem risks are high that government debt dynamics are becoming unsustainable, the default position of Japanese investors is to bring funds home, mainly it seems fearing being caught out by a rising trend in JPY.

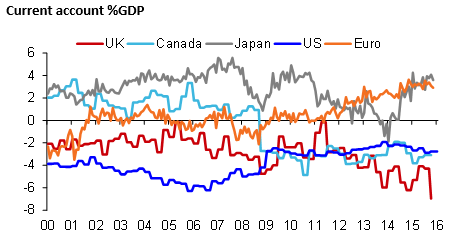

Japan has a large current account surplus and the presumption is that if capital outflow is not happening, then exporter demand for repatriating foreign export earnings will push JPY higher.

The rising trend in JPY has developed a life of its own, to some extent it can be justified by a shift in global flow dynamics, although the reasons for this may not be completely rational.

JPY rise adds to global risk aversion

One of the consequences of this trend is that it is adding to global risk aversion by generating its own level of uncertainty, and highlighting that Japanese investors are becoming more risk averse. It makes it seem that funding currencies (the lowest yielding currencies) cannot be safely utilized to fund bets in higher yielding risky assets, including the Japanese stock market.

It increases the odds of more monetary policy easing in Japan, probably yet more negative interest rates. This creates downside pressure on global bond yields. This may then tend to boost global asset prices or at least underpin them, but in a manner that leaves the market deeply unsure over the sustainability of stability in financial markets and global growth.

Earlier this week I described the AUD as in no man’s land, and indeed it has chopped around in a wide range lacking a clear direction. Copper prices plunged today, adding to the sense of insecurity in global markets.

It feels like we may continue to see a lot of churn in global markets. My attention continues to turn to gold, anticipating demand as a store of value against negative and low yielding currencies and volatile asset markets. However, admittedly, even gold has been volatile and lacking clear direction.