May’s bid to boost power, Trump’s words lose power

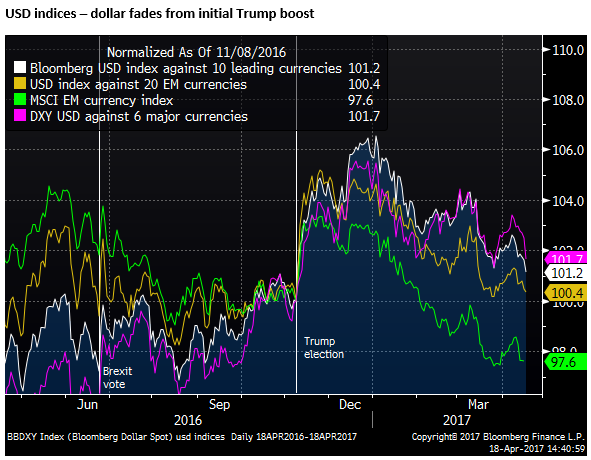

The USD has given back its initial Trump inspired rally. Confidence in Trump’s capacity to deliver on his ambitious agenda has faded. Economic recovery outside of the US has gained momentum, attracting capital flow to emerging markets. Geopolitical risks have boosted JPY and gold, while lessened Trump’s desire to pursue trade restrictions against China. US economic activity in Q1 has been sub-trend and recent inflation data has softened, lessening the urgency for Fed policy tightening. Trump has called for a weaker USD and said he likes low-interest rates, reversing his pre-election basis for criticizing Fed Chair Yellen. UK PM May has inspired a break-up in the GBP that may build momentum if she can campaign effectively and strengthen her grip on power. The first round French election this weekend may help lift political uncertainty and spur a recovery in EUR. On Tuesday, Trump again promised big policy strides on tax, infrastructure, and healthcare, railed against NAFTA, and signed an executive order to review the USA skilled visa program and renew a Federal policy to buy and hire American. Early in his still short presidency, such actions might have boosted the USD and US equities. The market is now more focused on results rather than rhetoric.

GBP breaks-up

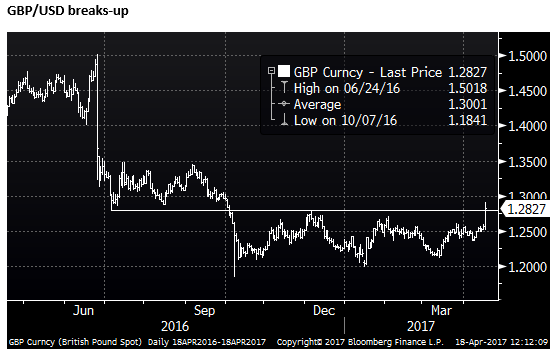

GBP has surged over 2% on a gambit by UK Conservative Party leader and Prime Minister Theresa May to call an early election. More broadly this appears to have helped drag the USD somewhat lower.

GBP/USD has busted up out of its range since the flash-crash in early-October last year that appeared to follow confirmation that the UK government would seek a so-called hard-Brexit, leaving the single market and giving up banks’ passporting rights, undermining the future of London as the financial hub for Europe.

The UK government will still pursue a hard Brexit and the form of new trading relations with Europe remain highly uncertain. Nevertheless, excessive pessimism over the future of the UK economy outside of the EU has apparently faded significantly with this simple surprise announcement for a fresh mandate by the UK PM May.

PM May was selected as leader by her Conservative Party peers in the wake of the 23 June Brexit vote. A fresh election would give her a firmer status as party leader and PM, giving her a mandate provided by the people. The Conservatives hold a commanding lead in opinion polls suggesting that PM May will be able to lead her party to a larger majority in parliament.

A stronger electoral mandate would increase her capacity to lead Brexit negotiations with the EU with less interference from varying opinions within her own party and across parliament, and less electoral pressure, extending the term of parliament from 2020 to 2022, well beyond the 2-year timetable for Brexit negotiations.

PM May must achieve a two-third vote in favour of her motion for an early election. The vote is scheduled for Wednesday, but the main opposition parties have indicated they will support the motion, paving the way for the early election called for 8 June.

The UK House of Commons, the lower house, where the government is formed has 650 seats. The elections are normally held every five years. The Conservative party currently holds 330 of the 650 seats, an outright majority, ahead of the Labour party with 230 seats.

A recent opinion poll by ComRes for The Independent newspaper placed the Conservatives with a commanding 46% share of the vote, ahead of the Labour party with 25%; the Liberal Democrats (pro-EU) had 11% and UKip (anti-EU) 9%.

The market appears to see the Conservatives as placed to be returned with an increased outright majority of seats.

Given the close referendum vote in favour of Brexit on 23 June (51.9% for, 48.1% against) one might wonder if the election will serve as a kind of referendum do-over. However, the main opposition party – Labour – does not have a clear position on Brexit, and many Labour voters are in favour of Brexit.

Labour Leader, Corbyn, did not mention Brexit as a campaign issue in his first response to the call for an election. He is not popular and Labour is expected to lose a significant number of seats.

The Liberal Democrats hold only 8 seats in Parliament, down from 57 seats in 2010, when they formed a coalition agreement with the Conservatives to help form government. The LD will run as a pro-EU alternative and this may help them boost numbers in parliament.

There is some risk that they gain enough seats to hold a balance of power and block the ambitions of PM May to deliver a hard Brexit. However, recent polling shows them well behind with only 11% public support.

The Scottish National Party has 54 of 59 possible seats in the UK parliament, making it the third largest party. It has called for a fresh Scottish independence referendum essentially because it is pro-EU. It is likely to maintain a commanding hold of these seats as Scottish voters express their displeasure with Brexit. PM May has denied their calls for a fresh referendum until after Brexit is negotiated. At best the SNP can only gain 5 more seats, so it appears unlikely to sway the odds by much against an increased majority by the Conservatives.

The prospect of another Scottish independence referendum continues as a potential negative for the GBP. However, it has been on the cards for some time, and is unlikely to happen ahead of Brexit, by which time the Scots may again decide it is better the stay with the devil they know.

PM May may have calculated that many moderate pro-EU voters will see Brexit as inevitable and vote for the Conservatives to give them a stronger position from which to negotiate a better deal and a clearer path for the UK in a reasonable timeframe. This might be preferred to a mixed vision of Brexit that lacks broad parliamentary support and leaves the UK in a poor negotiating position that drags on and risks the UK being dropped out of the EU without any new trade deal in sight.

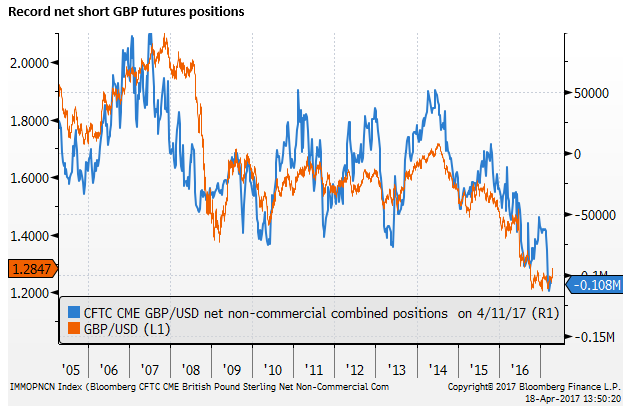

The market is coming from a position of having factored in a significant degree of downside risk for the UK economy. The GBP has fallen significantly in the lead up to and after the Brexit vote. The futures market suggests that traders are significantly short GBP, but near a record margin.

As such, if the Conservative Party and PM May campaign effectively and maintain or increase their majority in parliament, the GBP has scope to post a further recovery of its losses since the 23 June Brexit referendum.

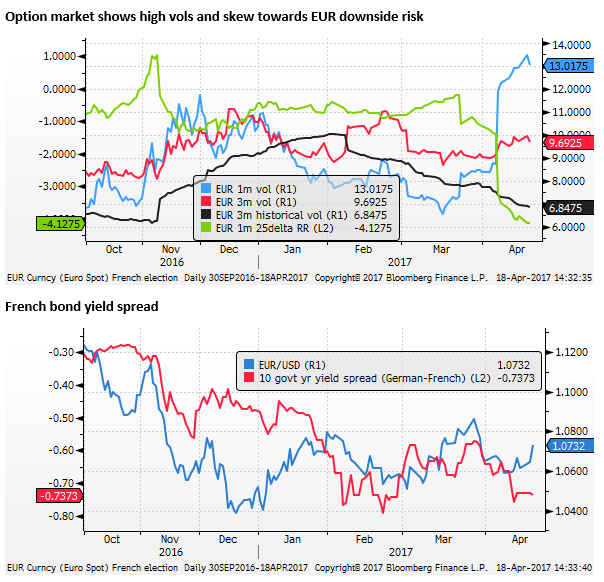

EUR hangs in the balance

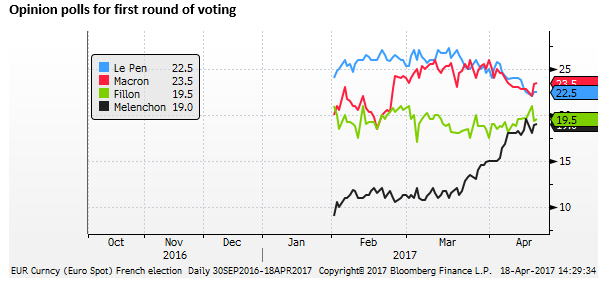

The EUR continues to hang in the balance ahead of the first round of the French election this Sunday. EUR remains somewhat depressed by the risk of an anti-EU candidate.

Polls for the first round are close across four candidates, two pro-Euro candidates, Emmanuel Macro (En Marche!) first in the opinion polls (23.5%) and Francois Fillon (The Republicans) third in the polls (19.5%). And two anti-EU candidates, Marine Le Pen (National Front) second in the polls (22.5%) and Jean-Luc Melenchon (Unsubmissive France) fourth in the polls (19.0%).

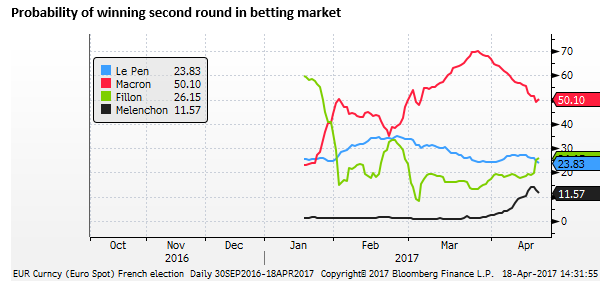

Each of the four has a chance of making it to the final head-to-head run-off election on 7 May. The most likely outcome is Macron (pro-EU) vs Le Pen (ant-EU). In this event, Macron would appear to be in a very good position to win the final second round vote as the moderate candidate. The betting market still has Macron as a favourite, significantly ahead of the other candidates

If Macron gets through to the final round we should start to see his probability of winning rise and the EUR strengthen.

Trump makes more big economic promises

The USD has retraced much of its gains since the Trump election on 8 November. Some of this fall reflects lost confidence that Trump can deliver on his election rhetoric to cut taxes, boost infrastructure spending and engineer strong growth and employment with his America First policies.

The USD has also lost ground as global recovery has gained traction. Capital appears to be flowing to a number of emerging markets as their growth prospects improve. In a relative growth analysis, the USA no longer stands out as exhibiting the strongest or most stable growth outlook.

JPY and gold have benefited from some heightened political and geopolitical risks as the French election draws near and the US takes a more aggressive posture with Syria and North Korea.

President Trump himself said he thought the USD was too strong and liked the Fed’s low interest rate policy; contrasting with his pre-election criticism of Fed Chair Yellen for keeping rates low.

Brexit uncertainty may now be easing, and the French election may pave the way for EUR to strengthen, pointing to potential upside for GBP and EUR in the coming weeks.

The Fed’s urgency to raise rates may appear dampened by the softer CPI reading in March and modest Q1 growth indicators; even though survey data continue to point to a solid recovery in the USA.

Undeterred by setbacks and roadblocks in Congress, in a speech on Tuesday, President Trump continued to promise big policy strides, very soon; including tax cuts, infrastructure spending, and a healthcare bill.

The speech followed an executive order signing to review the H-1B visa program for skilled workers and direct Federal agencies to buy and hire American. He did so in front of employers of manufacturing company at Snap-On Tools.

Such rhetoric earlier in his still short presidency might have given the USD and US equities a significant boost. However, the market has become more skeptical and is more focused on results.