More stable oil and EUR to underperform commodity currencies

More stability in oil prices, anticipated policy easing by the ECB, intensified efforts in China to control its currency, and a Fed that is keeping its policy options open and likely to delay policy tightening on recent ebbing trends in US growth and global market uncertainty are likely to combine to support global equity markets and risk appetite. We anticipate a lengthy consolidation in equities after a tough start to the year, and some recovery in commodity currencies, mostly against the EUR. Weak Chinese economic growth and more volatile Chinese equities, indicative of domestic financial stress, pose the biggest threat to this more benign near term outlook. However, a good deal of the negative outlook for Chinese commodity demand may be baked in the cake.

The risk sapping slide in oil may be over

Oil prices may have formed a base for the time-being, bouncing relatively sharply late-last week and showing some bounce again on Tuesday after a pull-back on Monday. News that Saudi Arabia and Russia may collaborate to reduce their supply and encourage both OPEC members and non-members to do the same has helped support prices. It remains to be seen how genuine or successful these key figures in the oil industry will be in controlling the oil market, but after the rapid risk-sapping slide over the last two months, the market is ripe for a bit of consolidation.

ECB most moved by oil

The rapid fall in oil prices over the last two months set-off a considerable amount of global risk aversion and moved at least one major central bank to talk about further easing monetary policy – namely the ECB.

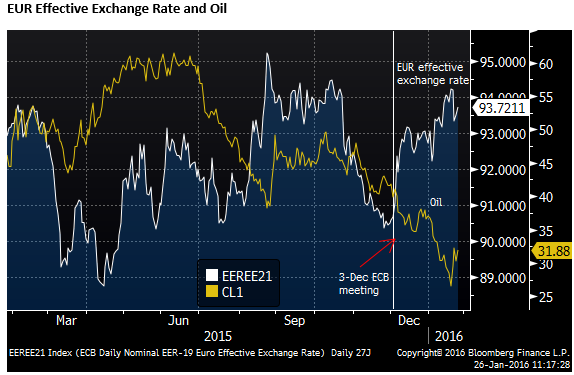

ECB President Draghi last week highlighted the rise in the EUR effective exchange rate as one of several factors that point to the need to enhance its monetary easing.

Of course a big part of that rise came in the immediate aftermath of the ECB’s policy easing on 3 Dec that was less impressive than advertised.

But some of the rise has occurred as a result of risk aversion boosting the EUR on a reduction in leverage or carry trades funded by shorting the EUR.

As falling oil prices contributed to falling risk appetite (rising risk aversion or risk premia), EUR became somewhat negatively correlated with oil (rising as oil fell), thus doubling the downward pressure on inflation expectations in the Eurozone.

The ECB has tried, either consciously or subconsciously, to break this negative correlation between oil and EUR, by making oil prices a significant factor in its monetary policy decisions. More than the other major central banks, the ECB has argued that the fall in oil prices is and can have a significant impact on long term inflation expectations.

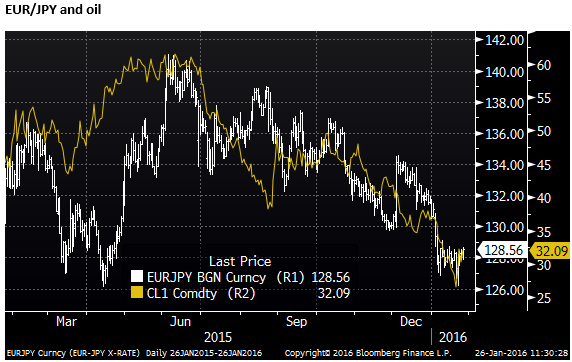

This has been a significant factor in the fall in EUR/JPY since Q3 last year. In contrast to the ECB, the BoJ has tended to down-play the impact of oil prices on inflation expectations. Again last week, at Davos, BoJ’s Kuroda thought inflation expectations had not moved much and continued to argue that oil prices would not have a long-lasting impact on inflation.

So now that oil prices may have bottomed, should we expect the ECB to back-off from its easing rhetoric? And will the EUR become positively correlated with oil?

On the first question, central banks can’t afford to swing views back and forth with market prices at a whim. The ECB, for a range of reasons, appears to have decided they will further expand policy easing on 10 March.

In some respects it may be the case that the ECB wants to make up for not delivering as much as expected on 3 Dec. It has seen its currency strengthen since 3 Dec, probably more than it thought it might. This may have moved more of the council members to get behind ECB President Draghi and display unity, allowing him to set the tone and control market expectations.

A problem with the 3 December policy outcome was not so much about the size of policy easing delivered, it was the perception of disunity in the Governing Council and the threat that a more hawkish group had high-jacked the agenda from Draghi; weakening his capacity to drive policy aggressively towards boosting inflation.

Last week, Draghi linked policy to oil, but he also suggested that he had wrestled back the policy agenda from the hawks.

As such, the oil price would have to jump a long way to walk that easing guidance back. At best we might expect some moderation of the policy easing, but the ECB, in my view, is likely to err on the side of making up for the 3 Dec disappointment. I expect the ECB to aim for a significant easing in financial conditions that persists after the 10 March meeting, a key part of this metric is likely to be a fall in the EUR effective exchange rate.

This begins to answer the second question – will the EUR start to become positively correlated with oil? The answer is no, since modestly firmer oil prices are unlikely to discourage the ECB from easing policy on 10 March, and a firmer oil price should tend to help improve global risk appetite and encourage more shorting of the EUR to fund higher yielding investment. We expect the EUR to under-perform most currencies in an environment of stable or a partial recovery in oil prices.

Fed-Watch

Market commentators are suggesting that the modest risk rally (and rise in gold) is related to expectations that the Fed will sound less hawkish in its FOMC statement tomorrow. There may be some element of this, however, I think the FOMC statement is not crucial to the current consolidation in global markets. It is probably true that the market senses that the Fed will hold rates steady for longer (passing on March to hike again, and possibly waiting to the second-half of the year). Certainty the market is pricing only a very slim chance of a hike in March. This is a reflection of the flexibility that the Fed has declared in its policy statements for some time. It has consistently said policy tightening is expected to be gradual and will depend on the data. Recent data have moved the odds of a hike in March lower.

However, the Fed will still want to keep its options open, and the statement tomorrow is likely to sound ambivalent. It might edge somewhat less hawkish, but it is unlikely to give and clear guidance on March, and still express some confidence in the underlying trend in the economy. I doubt this will un-nerve global investors much, if at all.

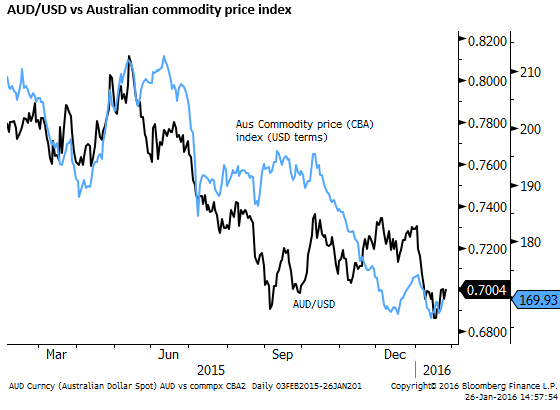

Some resilience in ex-oil commodities to events in China in recent months

There is no doubt that Chinese economic growth has slowed, especially in commodity intensive areas. Steel, cement, and electricity output are in persistent decline over the last year. However, what we haven’t seen in recent months is this spilling over to deep further falls in iron ore or coal prices. Base metals prices have also been relatively stable. In light of deep falls in oil and weak global equities, these other commodities have been relatively stable. The AUD has also held up relatively well in the face of global risk aversion. This suggests that the negativity for iron ore and coal is already in the price to a large extent. This is hardly a glowing endorsement to buy commodities, but suggests that their downside on weaker Chinese commodity demand expectations may now be limited.