New Zealand Election still hangs in the balance; Preview of Australian labour data

The Australian business survey was mixed, but showed significant improvement in labour components, suggesting upside risk for the Australia labour report out on Thursday. The latest New Zealand poll suggested that the chances of a return in the National government have increased greatly. However, a closer look at the trends and betting odds suggests the election hangs in the balance.

New Zealand election poll boosts National’s chances, but still too close to call

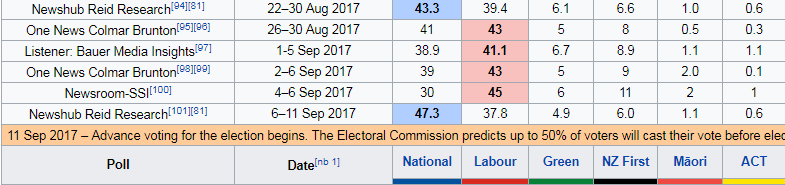

The NZD rebounded after the latest Newshub poll showed a sharp rebound in support for the ruling conservative National party last week from its poll taken a month earlier.

- National +4.0 pts to 47.3%

- Labour -1.2 to 37.8%.

- NZ -0.6 to 6.0%

- Greens – 1.2 to 4.9%

- TOP – 0.3 at 1.6%

- Maori +0.1 at 1.1%

- ACT no change at 0.6%

The sink in the small parties close to the 5% threshold (especially the Greens), threatens to leave them out of parliament (since they are not contesting any electoral seats). This will push seats proportionally to the other parties. Since Green seats would normally all support a Labour claim on forming government, a failure to reach 5%, would take some of those seats and push them to National, increasing its chances of reaching the 61 seats needed for an outright majority.

Based on this poll, assuming Greens fall out of parliament, Nationals would get 61 seats and outright majority.

The jump in Nationals performance is thought to be related to a scare campaign from the National’s last week that Labour has a large fiscal hole in its budget, and a lack of clarity from Labour on their taxation plan.

A poll taken the week before by 1 News Colman Brunton had the result much closer, and had Labour in the lead (Labour 43%, National 39%, NZ First 9%, Greens 5%, Maori 2%, TOP 2%).

These polls appear volatile, so it is hard to draw too much from any one poll. The table below shows that the NewsHub poll, released today, tended to favour the Nationals last time as well, and was less supportive of Labour and NZ first than the other polls. As such, it may have over-estimated the support for Nationals. However, all recent polls suggest Greens are close to the 5% threshold.

Recent poll results (Wikipedia.org)

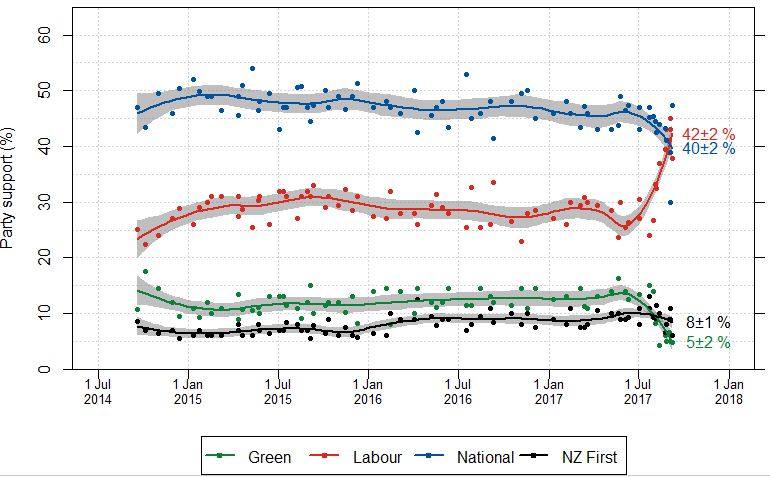

The chart below from Wikipedia helps show the trend in polls. It suggests that the race is very close and that NZ First is still highly likely to be a king-maker in this election; even if Greens drop out.

Ladbrokes betting company is paying $1.75 for a $1.00 bet for a Labour PM, and $2.00 for National PM. This implies that the probability of a Labour victory is 36% and a National Victory of 33%.

The odds, however, show no clear favourite and suggest there is a high level of uncertainty with the sum of the probability for the only real contenders much less than 100%.

NZ political odds – Ladbrokes.com.au

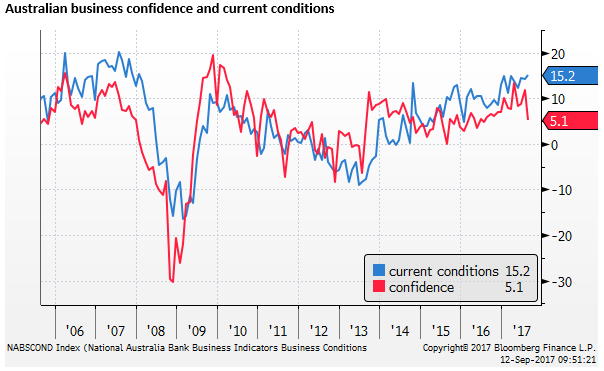

Australian Business survey – mixed outcome, labour indicators strong

Australian business confidence dipped sharply back to its long run average (from +12 to +5 in Aug). However, current conditions firmed from 14 to 15 in Aug, a high since 2008.

According to Mr Alan Oster, NAB’s Chief economist, “It is probably too early to read much into the drop in confidence this month. While external shocks, such as the escalating tensions with North Korea, may have had some impact, we have actually asked for the first time in the Survey what firms see as being the most influential factors impacting confidence. For those indicating deterioration in confidence, the biggest concerns appear to be customer demand, government policy, as well as cost pressures – both energy and wages”.

NAB Monthly Business Survey – business.nab.com.au

Retailing weak, construction strong

The weakest sector was retailing (conditions near flat and falling in recent months), consistent with subdued consumer confidence. The strongest sector was construction, consistent with the pick-up in infrastructure spending, and non-residential building approvals, and resilient residential approvals.

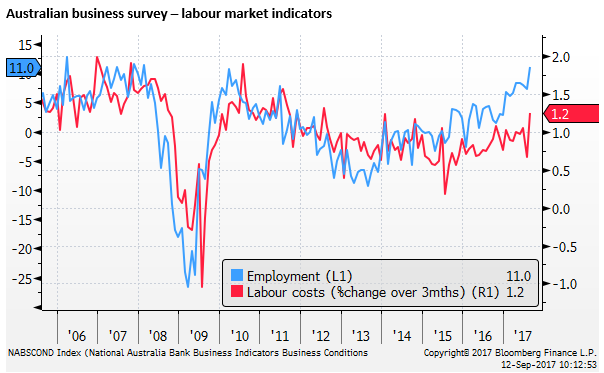

Labour market indicators strong

Labour market indicators were stronger – the employment component rose sharply from +7 to +11, a high since 2008.

The labour cost index rose 1.2% 3m/3m in Aug, a high since Oct-2014, reversing a dip in July. The 3mth average in this series was 1.0%, equaling the peaks since 2012. This may in part reflect the lift in the minimum wage from 1 July. The fall in business confidence survey suggests higher energy and wage pressures have squeezed margins and thus may lead to some inflation pressure.

Trading (+18) and profitability (+15) were down a touch, but remain around recent highs since 2008.

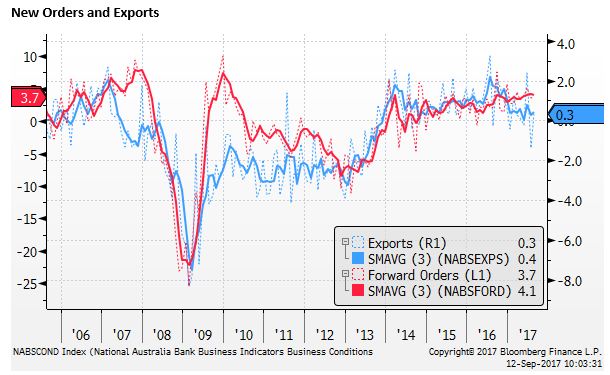

Orders were steady at +4, around highs since 2008. Stocks were also steady at +1, close to its long run average, such that the order/stocks ratio was above average.

The Export component has deteriorated since a peak around mid-2016, although still above average, suggesting domestic demand is supporting orders, but the rise in the AUD may be dampening export conditions.

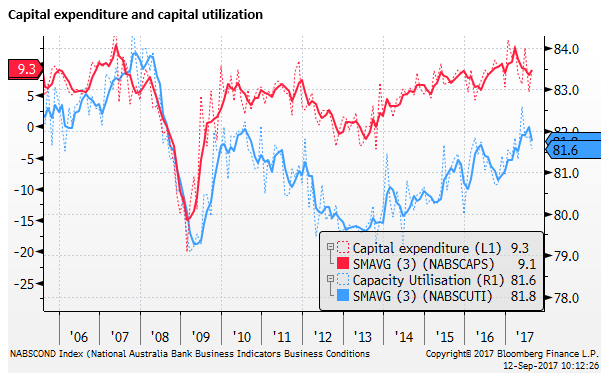

The Capital expenditure component rose in August but is down from the peak in around Q1. Capacity utilization is weaker in recent months but is around the highs since 2010, although still significantly below pre-2008 levels.

Australian Labour market data this week may be strong

The recent strength in business conditions, especially the employment component, and the acceleration in job ads suggests we may see further improvement in the labour market data on Thursday.

The market is expecting a fairly standard 20K rise in August jobs, somewhat above the long run average around +15K, and a bit below the 3mth average of 29K, and the six month average of 33K.

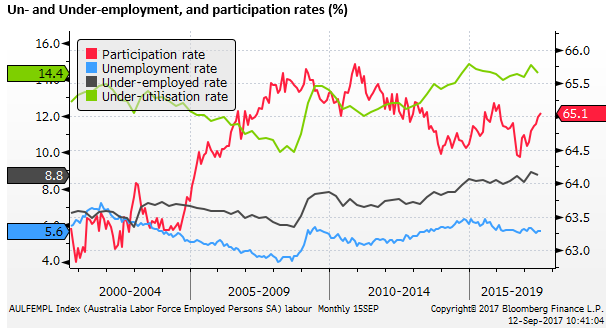

It is forecasting a steady unemployment rate of 5.6%, slightly up from the low in May of 5.5% (the low since 2013).

The RBA says that there is significant slack in the labour market. The neutral unemployment rate is thought to be near 5.0%. Contributing to the slack is more elevated under-employment that remains near its record high (Quarterly data 8.8% in June). Although there may be a structural element to the rising trend in under-employment.

The unemployment rate has been held steady in recent months, despite stronger employment growth, by a rebound in the participation rate from a low in Sep-2016 of 64.4% to 65.1 in July.

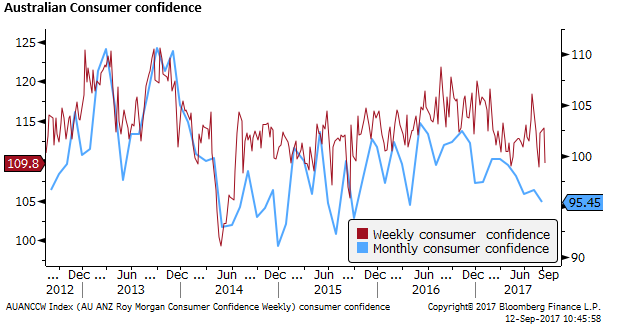

Consumer confidence may not improve much

Ahead of the labour data, the monthly consumer confidence data is released today. This was surprisingly weak last month; feeding the narrative that high household debt, a slowing housing market, weak wages growth, and higher electricity prices are weighing on consumer demand.

In August, confidence fell to around the lows since 2015; at 95.5, it is well below the long run average around 105. The weekly data released yesterday do not give much hope that the monthly reading will improve much, although the gap between the two is relatively large.