Phase II of Fed Policy Normalization May See Bigger Dollar Fall

The Fed is moving into a new phase of its policy normalization where it begins its QE portfolio run-down. Even though the Fed says it hopes this will run on autopilot in the background, it is a form of policy tightening, and further rate hikes will be done more cautiously. In fact, the timing of the next hike is much more uncertain, and it is possible there is a prolonged pause. The recent fall in inflation has extended for a fourth month and is not as temporary as the Fed described. Yellen has emphasized it in watching inflation closely, and a significant cohort of FOMC members are expressing reluctance to hike further, especially now that the Fed is prepared to begin the QE portfolio run down this year. The USD is approaching the base of a wide trading range over the last two to three years. In this new phase of Fed normalization, the USD is more vulnerable to breaking key technical supports. A number of other countries’ central banks appear to have delayed policy tightening, hoping to lag behind Fed rate hikes and avoid currency appreciation. This strategy contributes to a buildup in financial stability risks and no longer appears viable. Any hints towards policy normalization in other countries, especially involving rate hikes, may spark significant exchange rate gains against the USD. The market will be watching for any subtle hints in the ECB and BoJ meetings, and RBA minutes later today. The US recovery this year may be stalling, and failure by Congress on key legislation threatens to send the USD into a tailspin. The Healthcare bill remains a key test for Congress.

Rate hikes appear much less certain

The Yellen testimony and commentary from a range of other Fed members in the last week indicate that a significant cohort of members are not comfortable continuing to hike rates until inflation shows signs of recovering from its sharp fall in the four months to June. Most are prepared to start the run-down in the Fed’s QE asset portfolio, but this further reduces their appetite for rate hikes.

Yellen has said that rates will be the main policy instrument and the Fed would like to see the QE asset portfolio run-down occur in the background. Some more hawkish members argue that they don’t expect the portfolio run-down to have much impact on the pace of future rate hikes. However, there is little doubt that reducing the QE asset portfolio is a form of policy tightening and will cause the Fed to raise rates more carefully.

It is possible to conceive that the Fed now goes into a long pause on rates while it begins the QE asset portfolio run-down. On the most recent economic reports, suggesting growth momentum has failed to pick-up as much as earlier expected from a relatively weak Q1, and sudden reversal of inflation gains, rate hikes are likely to be off the agenda until further notice.

Yellen and Fed statements have said that once the QE portfolio run-down begins, the Fed may halt it or even reverse it if economic conditions deteriorate significantly. However, the Fed will be reluctant to adjust their stated plans for the pace of QE run-down, and will adjust rates as much as possible to calibrate policy. As such, a pause on rate hikes, which may turn out to be prolonged, would be the first response to the recent lower inflation trend.

Phase II may weaken the dollar

In a sense, the first stage of Fed policy tightening, where it had been just raising rates, is over. It is moving into a second phase where it is running down its QE asset portfolio. During this phase, the hurdle for further rate hikes is higher, and it is possible that rates have plateaued for a prolonged period, or will be raised more slowly.

If rate rises in the US appear less certain, the USD outlook may appear weaker. From 2014 to 2016, the USD was viewed as a strong currency as the market focused on diverging central bank monetary policies. However, now that the Fed has essentially completed phase one of its tightening, and a number of other central banks are moving closer to normalization, policy is no longer clearly diverging. In some cases, including most notably Canada, policy is converging.

The USD proved to be quite pre-emptive in adjusting to monetary policy divergence. Most of its rally occurred in 2014, well before the first hike in December 2015. It has been more ranging since early 2015, but rose to a new peak at end-2016 as the Fed enacted its second policy hike. However, it has fallen this year, even as the Fed has delivered its third and fourth hike on a faster three-month schedule.

You could argue that the USD has already begun to fall in anticipation of its second phase of policy normalization where the Fed begins its QE balance sheet wind-down later this year. As such, we should be cautious predicting ongoing USD weakness on a pause in US rate hikes. Nevertheless, if other countries continue to move towards policy normalization, further unwinding of the USD gains in 2014 to 2016 appears likely.

The chart below is the Bloomberg USD index against ten leading currencies, based on shares of international trade and FX liquidity. It provides one of the better overviews of the USD. It illustrates that the USD surged between June-2014 and March-2015. Since then it has mapped a wide ranging but more stable pattern. It is now approaching the base in that period, lows made in May/June 2015 and Apr/Aug 2016. It is possible to imagine as we move into a new phase of Fed policy and some policy convergence that the USD breaks these lows made on 2015 and 2016.

It is also fair to say that in the last two years the US economy has gone through lulls in its moderate recovery path, contributing to periods of weakness in the USD. Again more recently, the US economy has shown a mixed performance, contributing to doubts over further rate hikes.

USD index ebbs to low end of range

Political risk looms over the USD

The strength in the USD early in the year owed a good deal to expectations that the US government would enact a significant tax cut, and boost infrastructure spending.

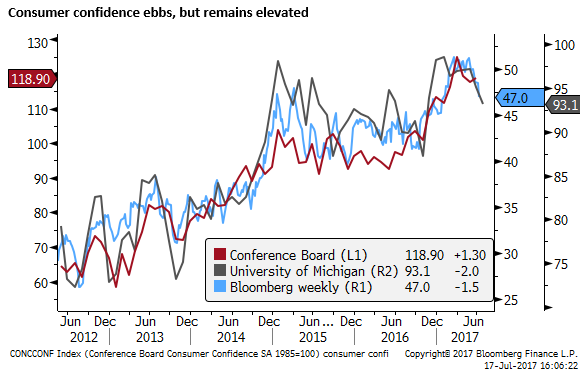

Some confidence appears to remain in surveys of small business and consumers. Hope has not been dashed that Congress will deliver on tax reform, perhaps now early next year. However, the risk is that confidence in the US government deteriorates further in coming months.

Frustration is increasing and was captured aptly in the widely reported outburst by JPMorgan CEO Jamie Dimon during his company’s earnings conference call.

Jamie Dimon Is Right to Raise the Alarm – Bloomberg.com

A key test this week, or perhaps next, is if the Senate can pass its version of the Healthcare bill to repeal and replace Obamacare.

Other tests will be how quickly Congress can pass a funding bill for the new fiscal year starting 1 October and raise the debt ceiling. September/October will sharpen the focus on these issues which threaten to shut-down government departments if they fail to be resolved in a timely manner. The Administration also hopes to at least table its tax reforms around the same time. If Congress cannot make progress on the Healthcare bill, the market will lose confidence in its capacity to deal with these other issues.

At the same time the Administration is fending off controversy over its connections to the Russian government, and Russian meddling in the 2016 election, Congressional committees and DoJ appointed special counsel are running ongoing investigations that threaten to interfere with progress in Congress; not to mention foreign policy issues that continue to distract the administration.

There remains a high level of uncertainty over the delivery of key policy reforms. If progress on tax reform appears to stall more permanently, the November 2018 mid-term elections will loom large over political environment.

Arguably, still elevated levels of business and consumer confidence are not translating into higher levels of business investment and consumer spending, because business and households are waiting for clarity on tax reform before committing to actual spending. If so, the modest recovery underway may persist for some time.

Lagging the Fed no longer a viable policy strategy

A number of other central banks have been hoping they could delay rate hikes and lag behind policy tightening by the Fed, so as to avoid unwanted appreciation in their exchange rates. However, this now appears to be a less viable strategy. The longer they delay policy tightening, the more they risk building up financial stability risks.

In this second phase of Fed policy normalization, further Fed rate hikes are much more uncertain. Moves towards policy normalization abroad, especially involving rate hikes, may see a sharp rise in these currencies against the USD. We have already seen this in the case of the CAD, dragging up the AUD by association. The EUR and GBP have also appreciated to be testing key resistance levels.

The market will be watching policy statements by other central banks more closely and pouncing on even subtle hints towards policy normalization on the horizon.

The EUR is edging up this week, even though most on the street have forecast that the ECB will avoid talking about its QE plans at its meeting this week. RBA policy minutes will be combed carefully today, and the BoJ policy meeting later in the week will also be watched closely, although they are expected least of all to discuss policy normalization.