RBA may outline a more dovish agenda

The base line view of many economists and commentators is that the RBA statement does not need to change much, and the RBA can stick to its current economic forecasts. This is true, but the risk is that the RBA provides a more accommodative policy guidance to further boost growth and to address the increased risk of a deterioration or undershooting its inflation target. The RBA is likely to retain a sense of confidence that the rebalancing of the Australian economy is proceeding well. But the risk is that it sends a signal that it can afford to grow faster. The RBA might also highlight the advantages of a lower AUD to help sustain the recovery.

RBA has the opportunity to reset policy guidance this week

This an important week for the AUD with the RBA quarterly monetary policy statement at end-week. This provides the RBA with an opportunity to re-set the policy agenda for the year ahead.

Towards the end of last year, the RBA took a relatively optimistic tone, noting the steady improvement in business confidence and the labour market. And highlighting evidence of a strong service sector providing an offset for the down-turn in the resources investment cycle. While business investment remained weaker than hoped, it foresaw the conditions that might see it pick-up over the year ahead.

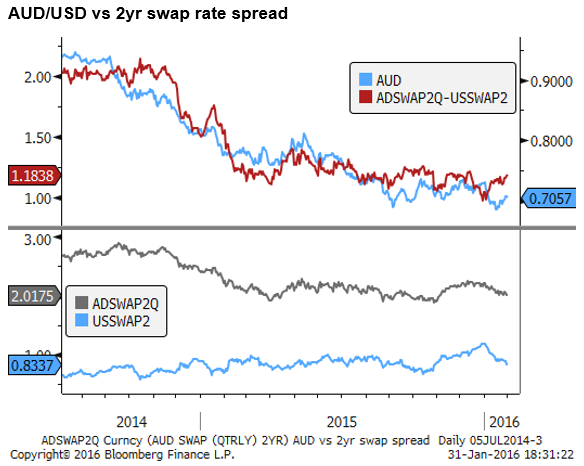

The RBA said, low inflation afforded it scope to cut interest rates if it thought the economy needed it. But this appeared to be a relatively soft easing bias, and most analysts think rates are quite firmly on hold for the near term. As a consequence, the AUD has picked up yield advantage over the USD since the beginning of the year, despite the turmoil in China and oil prices that might normally feed negative sentiment in Australia.

Most economists and commentators, presume that the RBA still holds this glass-half full view and prefers to keep rates steady and avoid saying too much on the exchange rate. Consequently, the AUD has lifted recently in line with a recovery in global risk appetite.

RBA Governor Glenn Stevens does like to display a laconic calm in the face of market volatility. He has played that game for several months now, perhaps designed to help bolster broader economic confidence in Australia. However, in considering his next move, it may be time to show he is watchful of global risks and can afford to ease policy to help boost growth above potential without threatening an inflation break-out, and even to counter the risk that inflation undershoots the target for too long.

The RBA is likely to retain a sense of confidence that the rebalancing of the Australian economy is proceeding well. But the risk is that it sends a signal that it can afford to grow faster. The RBA might also highlight the advantages of a lower AUD to help sustain the recovery.

The base case on the street is a fairly bland steady as she goes policy statement and set of economic forecasts. However, if there is a risk to this scenario it is that the RBA places more emphasis on its capacity to ease policy to spur growth.

Weaker trading partner growth and greater global risks

In recent months, the economic data from China has ebbed further, particularly for the heavy industry sectors that are the most relevant the Australian resources sector.

There are more risks generally related to demand from China as it potentially tightens-up capital outflow.

The IMF has down-graded the global growth outlook somewhat this year, related mainly to emerging markets. And the US economy posted a relatively weak Q4.

The BoJ has enacted and the ECB telegraphed more policy easing at least in part to counter a weaker global economic environment. The Fed highlighted greater global and financial market uncertainty, and the RBNZ also re-instated an easing bias, highlighting greater global uncertainty.

The RBA already downgraded its trading partner economic outlook in November last year, and highlighted increased downside risks from China. As such, it does not necessarily need to further allude to global uncertainty. But these considerations were treated as risks and did not play a big role in setting the tone for policy direction. They may cast a somewhat bigger shadow over the RBA policy outlook in their statements this week.

Some moderation in domestic indicators

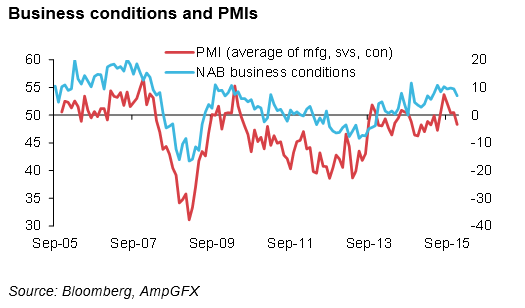

As far as the domestic economic data goes, there has been modest ebbing in forward looking indicators. The PMIs for services and construction dipped back below 50 in recent months, although the manufacturing PMI has remained above 50.

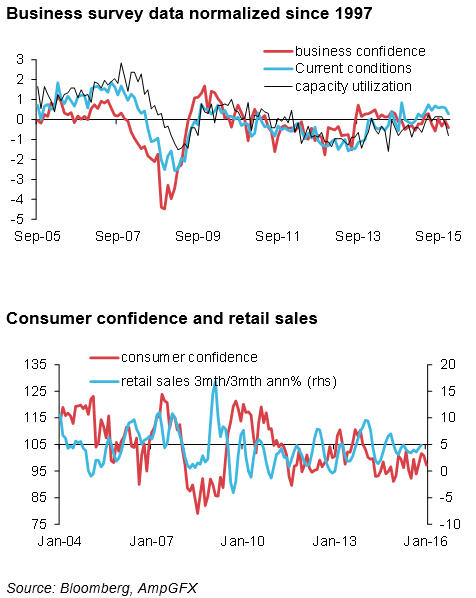

The NAB business survey showed a dip in conditions in Nov/Dec, but still remains just above the long run average. Confidence and capacity utilization also fell a bit below the long run average. But there is still an improving trend over the last year or two. Some recent ebbing in confidence may be understandably given weaker global equity markets and news surrounding market developments in China and oil. The degree of deterioration in these survey data is not enough to demand a change of core view on the economy, but it may be enough to shade the risks towards more easing.

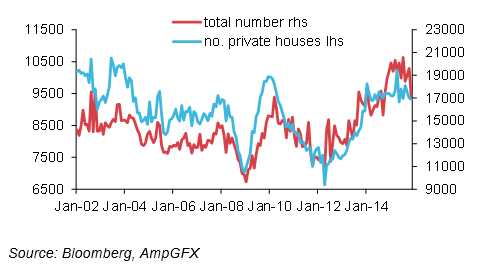

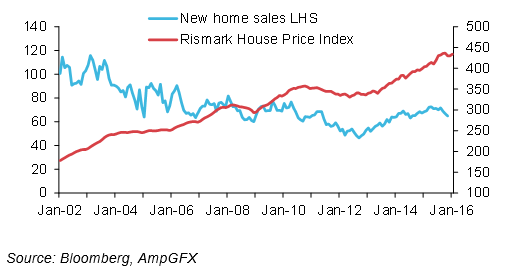

Total building approvals, led by the apartment sector have fallen back in recent months. And the number of residential house approvals has been stable for almost two years, at a relatively high level. Residential construction is providing significant support for the economy, but this is likely to wane toward the end of 2016.

House price growth also appears to have levelled off over the last 5 months, which may be a sign that the market is responding to macro-prudential tightening, some increased enforcement of foreign investment rules, slower immigration, and affordability limits. Such considerations may at some point open the door to more rate cuts. But the RBA will be cautious about encouraging faster household debt growth.

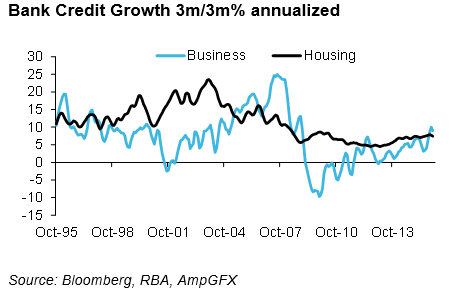

Bank credit growth has picked up for businesses to a solid pace of 9.0% 3m/3m annualized in December, surpassing overall housing credit growth of 7.4% 3m/3m annualized. The RBA would be relatively pleased with this switch to more business credit growth as a sign of improved confidence and some evidence of increased business investment.

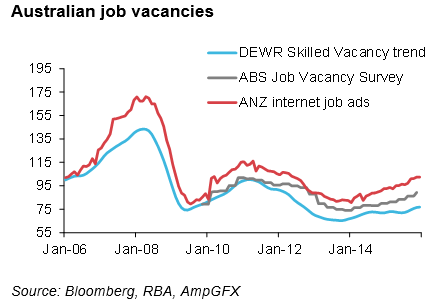

The labour market has shown improvement through the last year, and indicators of job vacancies continues to show a steady improving trend.

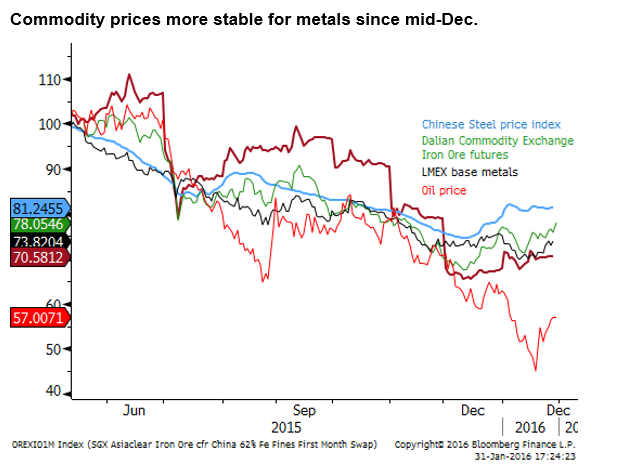

Even though oil prices have fallen significantly since last year, iron ore and steel prices in China have improved modestly since mid-December.

Low inflation affords scope, or risks undershoot?

The base line view of many economists and commentators is that the RBA statement does not need to change much, and the RBA can stick to its current economic forecasts. This is true, but the risk is that the RBA sets course for a more accommodative policy guidance to further boost growth and to address the increased risk of a deterioration.

The key message from the RBA in its recent statements is that; “the prospects for an improvement in economic conditions had firmed a little over recent months and that leaving the cash rate unchanged was appropriate. Members also observed that the outlook for inflation may afford scope for further easing of policy, should that be appropriate to lend support to demand.”

The market seemed to take a strangely positive spin on the recent inflation data, even though the weighted median underlying measure was 1.9%y/y, below 2.1% expected, and below the 2-3% target band. The other closely watched underlying measure, the trimmed mean was only as expected at 2.1%y/y.

Certainty the low inflation data continues to “afford scope” to ease further. But it is also the case that inflation is so low that the RBA cannot afford to let the recovery momentum slip significantly. There is an argument that it should attempt to counter the increased risks to the downside for growth by easing policy further.

Since August, the RBA has said, “The Australian dollar is adjusting to the significant declines in key commodity prices.” This may be broadly true, and the RBA may retain this assessment. However, there is a risk that it tweaks the statement to help bolster growth. It could comment that a weaker AUD would be helpful in strengthening and supporting the ongoing rebalancing of the economy.