RBA Rate Hikes in View, Tail Risks a Distraction

Australian Employment growth has surged in the last three months to the fastest rate since 2004, and the unemployment rate has fallen to recent lows. Forward-looking employment indicators have accelerated in recent months, and the labour report on Thursday may again beat albeit somewhat elevated expectations. The market is still being distracted by the tail risks related to housing and China, doubting that the RBA will raise rates, but the reality is that housing prices and sales activity have reaccelerated, macroprudential measures have had a modest dampening impact, and Chinese activity and iron ore prices have also strengthened in recent months. Consumer spending has also recovered in April and May from a weak Q1 and may be supported by stronger employment growth. The RBA minutes note the upswing in government infrastructure that has begun and the positive spillover to the private sector. Wage price indicators may have bottomed and the surge in electricity prices will filter through to higher inflation outcomes this year; perhaps as soon as the Q2 report due next week. Slack remains in the labour market, and inflation remains below its target range. However, the RBA’s own research suggests rates are very accommodative; 200bp below neutral, and it appears that significant progress is now being made towards returning to balanced growth and higher inflation. The RBA minutes further noted the improved outlook in the global economy. Currency strength may again delay an RBA hike, but the balance of risks suggest that a hike within the next few months is by no means out of the question, and hike before year end or early next year seems likely. The New Zealand CPI was below expected and the RBNZ appears more likely to stay on hold for the foreseeable future as its macroprudential measures prove more effective.

Australian rate hike expectations are still modest

The RBA policy minutes helped trigger a further rally in the AUD, and rates are modestly higher. The lift in Australian rates has probably been curtailed by the strength in the AUD.

The market is pricing in some odds of a hike later this year, although it is still pretty modest (7.3bp; 27% of a 25bp hike) by the last meeting of the year in December. A full 25bp is not priced in until the second half of 2018.

This is still a relatively conservative assessment considering the strength of recent economic reports, including stronger growth outcomes in China in Q2 and higher iron ore prices. It is fair to say that the market retains a high degree of fear that housing market and household debt excesses in Australia, and/or financial risks in China, yet return to undermine the economic outlook in Australia. While we have sympathies for these views, the RBA may feel it necessary to give a clearer warning before long that it may need to hike sooner to deal with the current realities rather than tail risks that may or may not materialize in the next year.

Policy is a long way from home

The RBA staff have been presenting on some special issues to the Board at their monthly meetings, and on 4 July the staff reported on its research into the neutral policy interest rate. It may be just a coincidence that this discussion was tabled in July, just at the time when a number of other central banks had turned less dovish, discussing removing policy accommodation and normalizing policy, but it suggests that the RBA too is thinking about normalization.

As we wrote in our report yesterday, with the Fed moving into phase II of its policy normalization that includes QE portfolio run-down, at the same time as the US economic and inflation outlook appears more subdued, even subtle hints of policy normalization in other countries, especially involving rate hikes, may significantly boost their currencies. The RBA provided a subtle hint by tabling its discussion on rates normality.

The RBA staff research came up with a real neutral policy rate of 1%. This was estimated to have fallen from 2.5% before the 2008 Global Financial Crisis, typical of the experience and research in other major countries of a new lower normal rates. The RBA argued that medium term inflation expectations were well anchored at the mid-point of its inflation target (2.5%), giving a neutral nominal rate of 3.5%. This suggests that the current policy setting (1.5%) is quite accommodative, 200bp below neutral.

One meeting at a time

The RBA has concluded in recent statements that, “at this meeting” … “holding the accommodative stance” unchanged is appropriate. There is no guidance and policy is being considered one meeting at a time. The RBA is less inclined than other central banks to provide policy guidance, but it does do so, and the market has perhaps been a bit dismissive of RBA’s lack of policy guidance. It has left its options open in part because it can see the possibility that it may want to move rates soon. With policy so clearly accommodative a move is much more likely to be up than down.

Housing tail risk, but prices have reaccelerated

The RBA has also concluded in recent meetings that “developments in the labour and housing markets…warrant careful monitoring”

The high level of household debt (above 190% of disposable income) has been elevated as a major policy concern by the RBA since Governor Lowe placed his stamp on policy since around Q3 last year. It is evident that he has enlisted the help of financial regulators (APRA and ASIC) to rein in bank mortgage lending standards further since early this year. The RBA is carefully monitoring what impact this has on household borrowing and consumer spending. An important related variable is housing prices, the main asset of households both as owners and investors.

This obvious risk faced by the RBA is that tightening lending standards that have resulted in some rises in mortgage lending rates for investors (much less so for owner-occupiers) spill over to weaker house prices, lower household wealth, weaker consumer confidence, and a desire to consolidate debt.

Many commentators doubt that the RBA will hike rates, or will do so in a very limited way, because doing so could trigger a negative housing feedback loop. PIMCO expressed this view last week.

Record household debt locks RBA in to low rates: PIMCO – SMH.com.au

It is true that the high debt levels and housing market, in a medium term sense, will tend to prevent the RBA from hiking rates as fast as previous cycles. It may even be the case that the new normal interest rate is lower than its estimate of 3.5%. However, this sentiment is distracting many in the market from the significant improvement in current economic conditions.

House Prices have risen rapidly in Sydney and Melbourne in recent years to levels that appear high compared to many other countries and domestic income. However, property prices have been rising rapidly in many parts of the world, as have asset prices in general; comparatively, developments in Australia are not unique.

Australia’s major cities are experiencing population growth. Like other major global cities, they have limited space and are considered premium places to live. Wealthy people around the world, in particular newly minted Chinese investors, are willing to pay up to get in. If we compare Sydney and Melbourne to New York, London, Hong Kong, Singapore, Shanghai, Vancouver, Toronto, etc, their high prices are not that special. There are many highly variable factors that determine the fate of the housing market. The RBA can ill afford to sit on its hands and wait for it to self-correct.

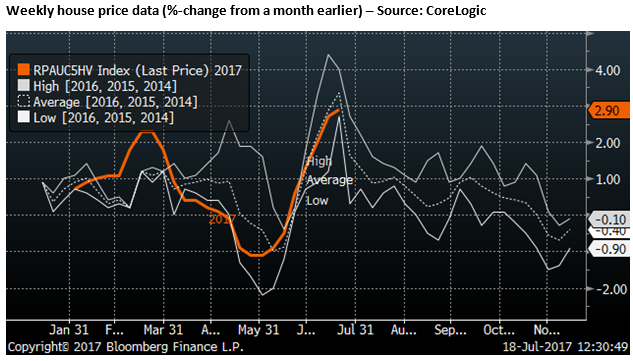

Housing indicators in Australia are still quite buoyant. CoreLogic prices have re-accelerated in the last month. Overall housing lending is stable (6.6%y/y), investor loan growth has ebbed, owner-occupier lending has picked up a bit. It is still running significantly above income growth, from a higher base.

The RBA noted the mixed nature of the housing market activity. It said, “Auction clearance rates in Sydney and Melbourne had softened recently, suggesting that conditions in these markets had eased somewhat.”

However, since the 4-July meeting, weekly auction clearance rates have firmed again, and in any case remain above the 5-year average.

Similarly, house prices have rebounded from falls in May and June, to solid gains later in June and July. The housing market experienced well above 5-year average prices gains early in the year, below average price gains in April/May, but has been running close to the average price gains in June and July. There is little evidence of a significant slowdown in house price growth.

The CoreLogic monthly Australian median city house price index for Australia showed a fall in annual growth from a peak since 2010 in March this year of 13.0%y/y, to 8.3%y/y in May, but rising to 9.7%y/y in June. Their weekly series suggests this will rise further in July. Overall it appears that the housing market remains relatively strong.

The RBA said in the minutes that “Conditions in established housing markets had continued to vary considerably across the country. Members recognised that it was too early for the prudential supervision measures announced by the Australian Prudential Regulation Authority, which were designed to help address the risks associated with high and rising levels of indebtedness, to have had their full effect.”

It may be too early, but it has been coming on six months. The impact has not been severe. A downturn in the housing market does not appear to be an imminent restraint on the RBA raising rates.

Lessons from Canada

Concern over the housing market and mortgage debt has resulted in a one-notch downgrade by Moody’s of Australian banks in June. However, consider the example of Canada recently. In April, a lower-quality mortgage lender Home Capital Group ran into financial difficulty in April, Moodys followed with across the board major Canadian bank downgrades in May. At the time the CAD was relatively weak, and the market had little expectation that the Bank of Canada might raise rates for the foreseeable future.

However, Canadian house prices have continued to surge, notwithstanding some modest macroprudential measures introduced late last year, and significant local government taxes on foreign investors. The Bank of Canada has hiked rates and the market is pricing in more hikes ahead. The CAD exchange rate has surged.

The market was distracted by the housing market and debt issues and paid little attention to actual evidence of economic recovery, and was wrong-footed by the Bank of Canada policy shift.

The Bank of Canada experience has been a bit of a wake-up call for the Australian market. But excessive fretting over the housing market is still proving to be a significant distraction for investors following Australian rates and currency.

Retail sales rebound in Q2

Retail sales were weak in Q1 in Australia. The RBA minutes noted that “The value of retail sales had increased in April, consistent with liaison reports that suggested conditions in the retail sector had improved. Members noted that the recent pick-up in growth in employment should also support a pick-up in household income growth, and therefore consumption growth, in the period ahead.”

Indeed, since the 4 July policy meeting, May retail sales also surprised to the upside, helping further reduce concerns that high household debt and macroprudential tightening were significantly dampening consumer spending. Annual growth in retail sales fell to a low since 2013 of 2.3%y/y in March, and has recovered to 3.8%y/y in May.

Government spending to boost economy

The RBA minutes from the 4 July policy meeting acknowledged for the first time the boost in demand from increased government spending on infrastructure. It said, “The most recent Australian and state government budgets suggested that fiscal policy would be more expansionary in 2017/18 than had previously been expected. Some of this expansion was expected to come from more spending on public infrastructure, particularly in New South Wales. Reflecting this, work yet to be done on public infrastructure had increased in recent quarters to a relatively high share of GDP. Members noted that infrastructure investment was expected to have significant positive spillovers to other parts of the economy. Non-residential building approvals had also risen in recent months.”

The government is already delivering on higher capital investment. In Q1 real Public Gross Fixed Capital Formation was up by 15.3%y/y, rising from relatively flat growth a year earlier (contributing around 0.75% to overall GDP growth). With the decline in investment from the mining sector largely complete, and expected improvement in non-mining private investment, the lift in government spending will help lift total economy investment in coming years. However, residential investment that has helped sustain the overall economy through the mining investment downturn is peaking.

Employment growth rebounded in recent months, but slack remains

In their June policy statements, the RBA tended to dismiss the improvement in employment growth as being driven by part-time jobs, and hours worked were lower. However, in July that picture had turned around. The July minutes said, “Members noted that growth in the preceding few months had been driven entirely by full-time employment and that total hours worked had trended higher as a result.”

However, it continued to point to slack in the labour market. They said, “The unemployment rate had declined by 0.3 percentage points over the previous two months, to be at its lowest rate since early 2013. However, the underemployment rate, which measures the number of part-time workers wanting to work more hours, had remained elevated.”

The unemployment rate has fallen to a more respectable 5.5% in May, modestly above levels around 5% considered close to full-employment. But the under-employment rate was 8.6% in May, down from a peak in the quarterly data of 8.8% in Feb. The under-utilisation rate, combining the un-and under-employment rates was 14.4%, still well above levels that appear near full-employment; perhaps around 12.5%.

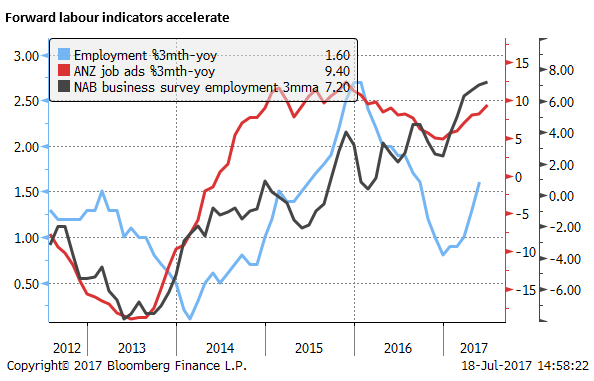

Forward looking labour indicators accelerate

The June employment report is due on Thursday this week. The pace of jobs growth has picked up in recent months, averaging 47K over the last three-months to May, the largest rise over three months since 2004. The long-run average monthly increase is around 15K.

As such, it is possible to see some pay-back fall in jobs growth in June, and this may disappoint market expectations for a 15K increase.

Nevertheless, the RBA has continued to note in its statements for some time, that the recent improvement in employment growth is consistent with “forward-looking indicators.” These include vacancy data and business surveys.

These forward-looking indicators may even have accelerated a bit in recent months. ANZ job ads have accelerated from around 5%y/y and end-2016 to 9.4% 3mth/yoy in June. The employment component of the NAB business survey rose to a high three-month moving average since 2010.

As such, we would not discount another stronger than expected increase in employment in June. The market is looking for the unemployment rate to tick back up to 5.6%, retracing some of its fall since March from 5.8% to 5.5% in May. But the stronger trend in employment indicators suggests this may be too pessimistic. There will be no update this month on the quarterly under-employment measures.

Wage growth low but bottoming

As with many countries, wages growth in Australia has been running below normal levels. But the RBA July minutes noted a larger increase in the minimum wage coming in Q3. It said, “Wage measures in the March quarter national accounts had continued to suggest that labour cost pressures remained subdued. The Fair Work Commission had announced a 3.3 per cent increase in award wages and the national minimum wage, effective from 1 July 2017. This followed an increase of 2.4 per cent in 2016 and was likely to affect the wages of around two-fifths of workers.”

The quarterly Wage Cost index rose a feeble 1.9%y/y in Q1, unchanged from Q4 a low in the nearly two-decade old series, suggesting real wage growth is around zero. The RBA could afford to see it increase significantly even if productivity growth is relatively low, perhaps a little above 1%.

The slack in the labour market, mainly in underutilisation measures, suggests that wage growth may not pick-up all that much soon. Nevertheless, the NAB business survey showed a 1.2% 3mth/3mth increase in its labour cost measure, a high since Feb-2014, and on a three-month moving average basis, this index was at a high since 2012.As such, even the low wage indicators may be bottoming out.

Australian inflation lift from electricity prices

The New Zealand inflation data was significantly weaker than expected for Q2, but the Australian data may be more robust when released next week. Electricity prices have surged in Australia, and this is starting to filter down to consumer prices. The impact may be more evident in Q3, but may start to show up in Q2.

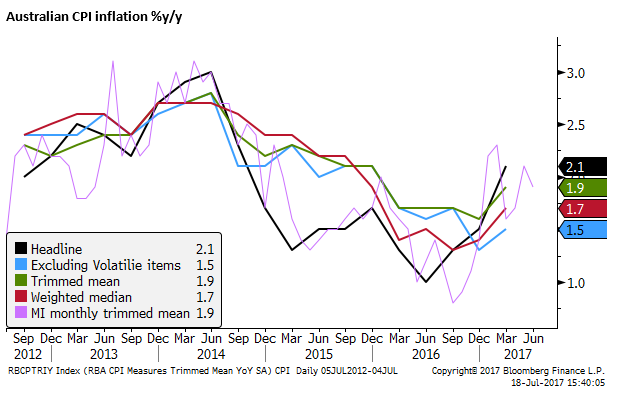

The monthly Melbourne Institute (MI) CPI measure averaged 2.6%y/y in Q2, up from 2.1% in Q1. This points to upside risk for headline quarterly inflation that was 1.9%y/y in Q1. The chart below shows the MI monthly headline reading, the National (ABS) quarterly reading, and a wholesale electricity price indicator.

The RBA pays closer attention to the underlying measures. The MI also produces a monthly estimate of the trimmed mean. It has averaged 1.9%y/y in Q2, down a touch from 2.0% in Q1. This suggests that the official national ABS reading may be little changed from its 1.9%y/y reading in Q1.

This would still leave inflation below the RBA 2 to 3% target. Another reason not to rush to hike rates. Nevertheless, it might help cement the view that inflation has bottomed out and improving from the lows in 2016.

New Zealand CPI weaker in Q2

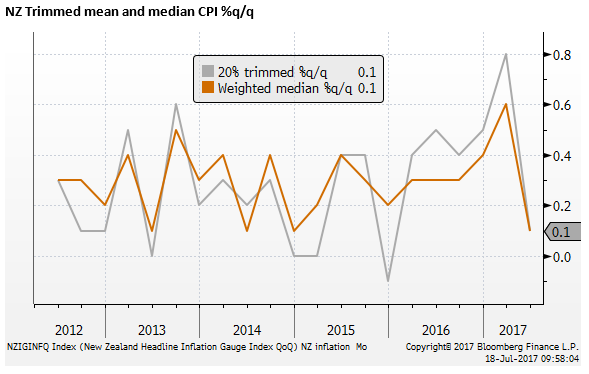

One of the ouch factors for the lower than expected NZ CPI Q2 outcome was that the Sector Factor Model, the most stable of the underlying measures, and most followed by the RBNZ ticked lower from 1.5% to 1.4%y/y.

The 20% trimmed mean and weighted median underlying measures had particularly low quarterly increases of only 0.1%q/q, a come-down from the relatively high readings in the previous three-quarters (between 0.3 to 0.8%q/q) that had started to give the impression inflation might be getting back to the the 2% target. The trimmed mean fell from 2.1% to 1.8%y/y, and the weighted median fell from 2.2% to 2.0%y/y.

The RBNZ forecast a 0.3%q/q Q2 increase in their May MPS, compared to the 0.0% actual headline result today. However, the RBNZ was already quite subdued in its medium term outlook for inflation, reacting less than most expected to the evidence of rising inflation last year and in Q1 this year. As such, this result probably doesn’t change their view much. In May they were not forecasting a rate hike until deep into 2019.

A number of other central banks have shifted attention somewhat from low inflation readings to tightening labour markets and financial stability concerns, justifying some recent policy tightening. This includes the Bank of Canada last week and the Fed in mid-June. However, the RBNZ has employed macroprudential policy measures with significant effect to control its housing market this year. As such it appears they may be one central bank that will not be shifting its rates policy for some time.