Rebounds in Asian Currencies and AUD may be short-lived

Time to step back and take a breath in the FX market. It lacks conviction, is displaying inconsistent correlations and being whipped around by competing news and views on uncertain events. The market can no longer rely on the US government to act as a source of stability for global markets. The rebound in Asian currencies is counterintuitive as US pressure mounts on Chinese trade and economic relations. But it may reflect position adjustment, a pull-back in US yields, and US policy uncertainty. The AUD continues to be supported by strong commodity prices, but domestic, Chinese and global financial stability risks, exacerbated by rising US rates, accounts for its weakness this year; we continue to see downside risks dominating

FX markets lack conviction

It is pretty easy to lose money in FX these days; there is a considerable amount of whippy price action even if in some cases there may be a discernible trend when you step back a few feet. There are some rather inconsistent correlations between FX and other markets like rates, commodities, credit spreads and equities, which suggest there is a fair bit of random price action.

There is a lot of contradictory news around big uncertain political events like Brexit, Italian budgets, elections and trade policy contributing to whippy price action. Trump continues to keep investors off-kilter with attacks on the Fed, deft manipulation of the media, and an unconventional approach to international relations. The market can no longer rely on the US Administration and Congress to provide a source of stability for global finance.

In examples of whippy price action on questionable fundamental grounds, the USD appeared to reverse gains and weaken significantly recently after USA UN ambassador Nikki Haley resigned, and after Trump called the Fed crazy for raising rates.

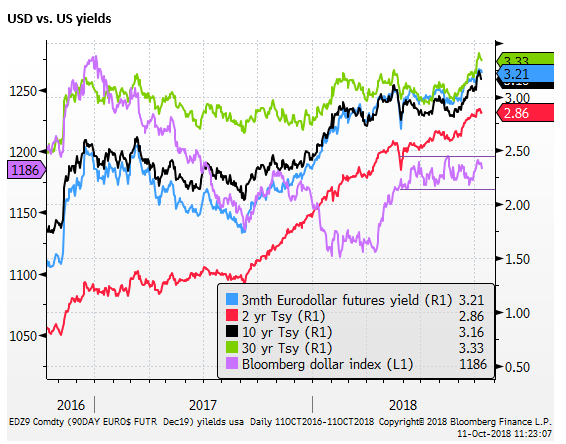

While the USD is stronger this year, supported by rising US rates and yields, the gains have been tepid. In fact, the USD has largely only recovered a part of its losses through last year. It rebounded sharply in Q2 amidst a heady mix of factors; including unsettled emerging markets, tariff and sanctions policy, Brexit uncertainty, Italian politics, and spillovers to a correction in the EUR.

However, the Bloomberg dollar index has largely moved in a sideways range since mid-year. The recent surge in US real and nominal yields to new highs for the year only served, so far, to return the USD to the top of its range.

Counter-intuitive rebound in Asia

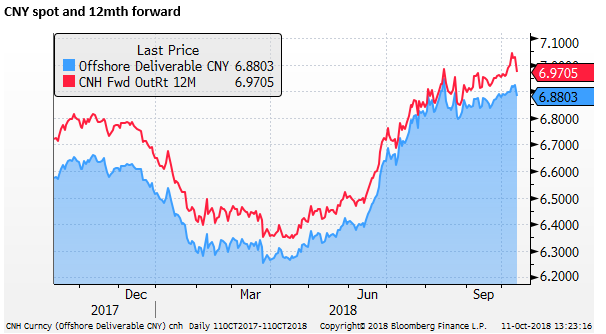

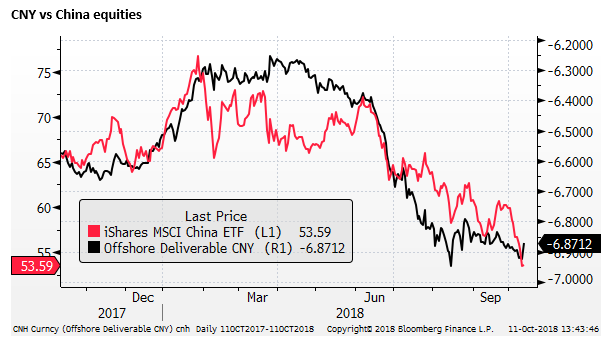

The CNY led a counter-intuitive rally in Asian currencies on Wednesday. The rise occurred despite a deep fall in tech stocks globally, including falls to new lows for the year in Asian equities, led by China equities.

The market could argue that the gains in Asian currencies may have been helped by a deeper fall In US equities on Wednesday and some retreat from the recent rise in US government bond yields. Trump’s aggressive criticism of the Fed’s rate policy, blaming it for the stock market correction also helped undermine the USD, including against Asian currencies.

The rebound in CNY also comes after it had recently fallen to near its mid-August lows in the spot market, and to new lows for the year in 12-month forward contracts. As such, its gains may reflect, in part, a correction in a down-trend, and fear of Chinese government efforts to stabilise the exchange rate to help engender broader Chinese financial markets stability.

However, the fundamental case to buy CNY would not have been helped by news that the US government had extradited a Chinese government spy, lured to Belgium for a fake meeting, to face charges of corporate espionage. The story comes after Bloomberg news reports alleged Chinese state-based espionage on a grand scale by adding chips to motherboards manufactured in China, and the US administration has accused China of widespread interference in US politics. The evidence of a toughening US government policy towards China suggests that it will continue to raise tariffs and harden its effort to stymie the Chinese economy and global reach.

But in an example of how news flow on uncertain events can keep the market off-kilter, reports that Trump plans to meet Chinese President Xi to “devise a way out of the trade battle” according to a WSJ report, on the sidelines of the G20 summit in November may have supported the CNY.

There is a lot of financial market media interest in whether the US Treasury will label China a currency manipulator for supposedly deliberately weakening its currency this year. It’s not clear if this would have any impact on the currency or financial markets, but it might be seen as an escalation of trade and geopolitical tensions between the super-powers. The fact that the US administration would consider this action speaks to the ingenuousness of the administration that is contributing to global market uncertainty. They surely know that China has if anything being supporting its currency this year.

We might conclude that the rebound in Asian currencies could be short-lived. But the uncertainty that surrounds global markets suggests caution and patience before selling.

China policy offsets may support other Asian economies

There are a number of investors that remain confident that China can use fiscal and monetary policy to cushion the economy adequately. Some see the boost to Chinese domestic-driven demand will help support demand in the region. Furthermore, it could be argued that as China shifts demand from the US to other nations (in retaliation to tariffs), and the US trade sanctions shift US demand towards other countries, other Asian nations may see stronger demand.

If China boosts infrastructure spending, it might increase support for steel-making commodity imports from Australia, lift commodity prices and help support the AUD.

Australian commodity prices support the AUD

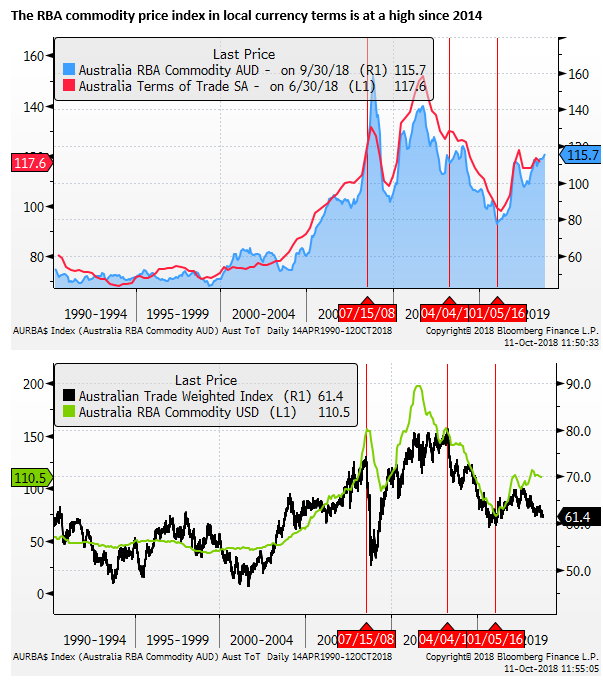

As it turns out, Commodity prices important for Australia have tended to rise this year. With the AUD falling this is providing a significant income boost for the Australian economy, coming largely through profitability in the mining sector.

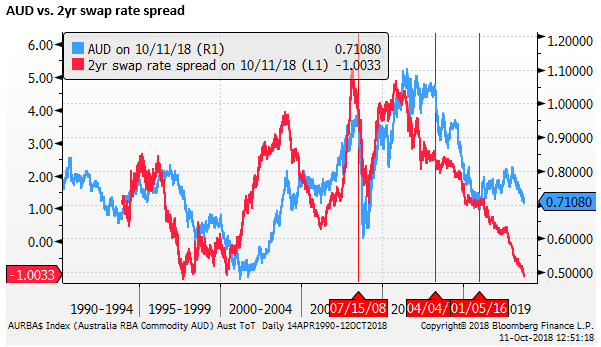

Three factors that account for a weaker AUD

As the chart above shows, the AUD has significantly underperformed the RBA commodity price index this year. However, three factors might explain this divergence. The first one is the fall in the AUD yield advantage. The chart below shows that the 2yr rate spread has fallen to a near a record low. However, as we have noted above, the USD is not getting as much support from its higher rates as might have been expected.

The second reason for a weaker AUD appears to be that it is acting as a proxy for financial and economic stability in China. It is arguably building in a risk premium for weaker financial stability in China as it deals with shadow-banking and broader credit excesses. And the additional layer of risk generated by US trade policy action against China.

The lower AUD may also reflect a higher risk premium for the additional risk of financial instability in Australia that arises from a weaker property market, high household debt in Australia, and tightening financial conditions related to increased regulatory scrutiny on Banks and the Hayne Royal Commission into the financial services sector.

The rise in US rates and yields may not be directly undermining the AUD. But they may be doing so indirectly by increasing the risk premium attached to the AUD. Higher US rates may heighten both the financial stability risks for China and other emerging markets, and the financial stability risks in Australia, forcing up funding costs for Australian banks.

The case for a higher AUD may build if the high terms of trade continues to boost the economic outlook and brings forward rate hike expectations in Australia. There is evidence that this is indeed happening, with the Australian economy growing above trend, unemployment falling, and government fiscal deficit narrowing more rapidly than expected. The weaker housing market has not yet appeared to have significantly undermined consumer confidence and spending.

Which way the AUD goes from here remains to be seen. We can see it going either way, but for the time being, we are more concerned that the risk premiums related to financial stability in China and Australia, exacerbated by rising US rates, will continue to dominate support from a higher terms of trade.