Regime change for the USD; AUD breaks down

It is easy to be cynical about newfound USD bullish sentiment, where suddenly yields and rates matter for currencies. However, rates and yields have more often played a dominant role in currency markets. Now that the equity market has become more volatile and confidence in the global economy has ebbed, we may see the USD continue to reconnect to its interest rate and yield differentials. In more automated and index driven markets, we may see a surprisingly rapid rebound in the USD with limited retracement. Political uncertainty has weighed on the USD over the last year, but Trump has gained traction with tax reform, trade policy, progress in Korea, and can claim credit for stronger economic momentum. A more assertive policy towards Syria and Iran may help improve Trump’s approval at home while increasing geopolitical uncertainty. It is too early for the market to be fretting about twin deficits. It needs to wait until there is a clearer picture of how Trump’s policies influence potential output, and the peak in US rates and yields are in sight. AUD/USD has broken key support and maybe reconnecting to its now negative yield spread across its entire yield curve. It faces headwinds from protectionist trade policies, tightening Chinese financial sector oversight, a weaker housing market, rising bank funding costs, pressure on its financial sector from a Royal Commission into its misconduct, and political uncertainty.

Fickle FX analysts go with the trend

It is easy to be cynical when it comes to currency analysis. A month ago the majority of analysts were USD bears, and interest rates and yields were no longer considered very important for its outlook. There was a lot of talk about twin deficits, and demise in the reserve currency status of the USD. Big picture views looking for QE ending in Europe and curve shapes dominated thinking. Now it seems most commentators are bullish towards the USD and see higher US yields as a key driver.

In the end, it seems that most of us, whether claiming to follow charts or fundamentals, are mostly influenced by trends. In the last week or so the USD appears to have broken out of a choppy consolidation over the last few months to be in a rising trend.

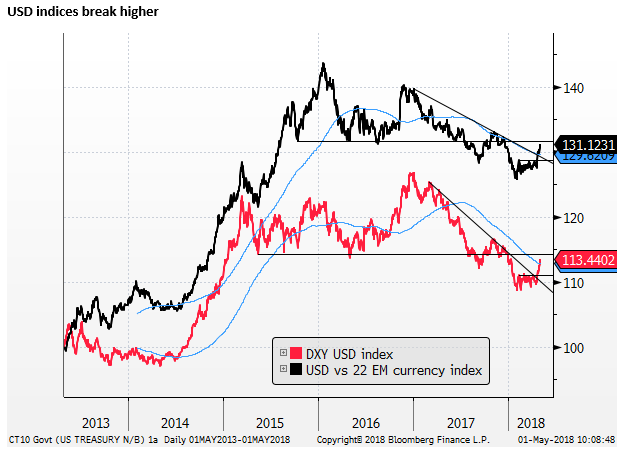

Newfound bullishness in the market follows a breakout of the range over the last few months. The chart below shows USD indices against other majors (DXY) and emerging market currencies. Both indices have broke down-trend lines and their 200 day moving averages.

Regime shift in the USD

It is essential to maintain a healthy scepticism in financial markets, especially FX markets, and it would be dangerous to presume that the USD has moved into a sustained uptrend. But it does appear, judging by market commentary, that there has been a genuine turn in sentiment that may last for a while and help the USD rise further.

We see the potential for a surprisingly rapid move in the USD with little retracement. Capital markets appear to be going through regime shifts that are causing more sustained divergences from fundamentals. This may reflect a shift to more automated and model-driven trading, and towards index investing.

A recent example is the surprisingly stable low vol but rapid rise in equity markets to a peak in January, followed by a regime shift to higher vol choppy trading. The USD fell precipitously through Dec/Jan, despite rapidly rising US rates and yields. It subsequently moved into a directionless but choppy pattern for several months.

We may be now breaking out of this pattern and could start to trend again with little retracement. This time reversing some or all of the weak pattern over the last year. It is possible that this move occurs without the sizeable retracements of recent months, making it hard for investors and traders to enter long USD positions or exit short positions. With a dearth of USD sellers for fundamental reasons or profit-taking, model and system-driven trading may see the USD rise more rapidly cutting through resistance levels with surprising ease.

The chart above is hinting this way with the rise in the USD in the last two weeks occurring rapidly with little retracement. The USD is now approaching or testing resistance levels (previous lows in 2017 and the earlier base from 2015/2017). It will be interesting to see if these prove to halt the USD advance much. I suspect that we may see only a minor pause with little retracement.

Regime shift in equity markets

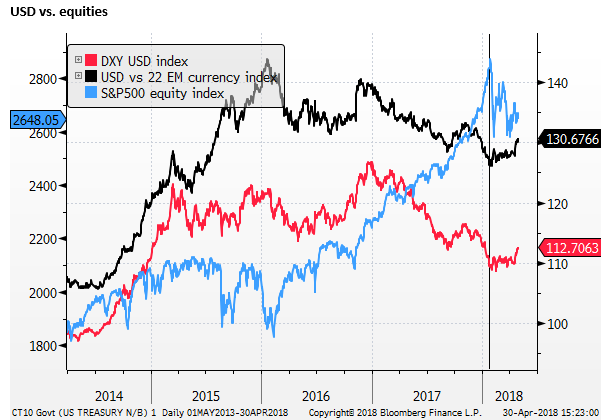

A key factor in the shift in tone in the USD, it seems is the change in regime in the global equity market. Since late-Jan, equity markets have become much more volatile, after a year of so remarkably low volatile but steady rapid appreciation in equities.

During that time equity markets dominated capital flows and interest rate developments barely registered in investors’ decisions. The general refrain was that Fed rate hikes were gradual, likely to be limited and will not derail a global economic recovery.

We can see from the chart below that the turning point for the USD was virtually the peak in the equity market rally in January. It took a while, Feb through much of April, for the USD to fully break out of its bearish funk, but the market is more convinced now that it needs to look beyond the equity market for performance.

We can also see from the chart above that the USD also performed strongly, especially against EM currencies during the equity market upheavals in 2015/2016.

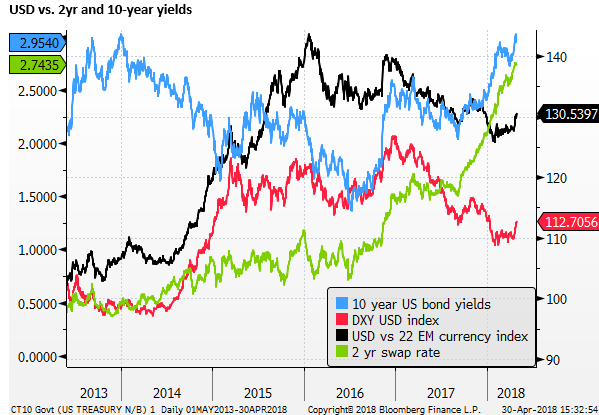

Turning back to rates

The USD was mixed in 2016, rising towards the end of 2016 before peaking in early 2017. Over this period, the equity market was rising, but much more volatile than in 2017, and the USD was probably being pulled in in two directions; sometimes influenced by equity capital flows, and others by rising US interest rates.

The peak for the USD in early-2017 came in the Euphoria of the Trump election as he promised big tax cuts and infrastructure spending while promoting an America First agenda. A combination of which sounded more positive for US growth and company earnings, while posing risks for export-driven economies abroad. US yields rose sharply post the Trump election in November 2016, propelling the USD higher.

Interest rates and yields have more often than not played a more important role in determining FX direction. Afterall, they are the clearest embodiment of central bank policy and inflation and growth expectations. And rates are a direct portion of currency return. The chart above shows that indeed the USD tended to follow the broad direction of rates and yields from 2014 to 2017.

In 2017, the USD started to diverge from rising US rates. However, through the first three-quarters of 2017, 2yr US yields were largely stable, and US 10-year yields fell. Inflation in the US was underwhelming expectations, and the market felt that it had largely factored in further Fed policy tightening. This left the USD ripe to be taken down by other factors such as equity capital flows or US political risks.

Outside of the US, economic recovery was taking hold in a low inflation environment. The fall in the USD was not inconsistent with lower long-term US yields.

The USD did mount a partial recovery in Sep/Nov as the Fed stuck to its plan to hike three times and begin to tighten quantitative policy, and Congress progressed to pass tax cuts.

The real divergence in the USD from rates and yields came from around mid-Dec through much of January-2018, when the USD resumed its downtrend even as both short and long-term US yields rose quite rapidly.

Equity markets went into overdrive during this period, rising rapidly with remarkably little volatility. The market had got used to largely ignoring Fed rate policy and had moved into a deeply bearish view of the USD. The USD had broken through its 2015/2017 base in July/Aug 2017, and most commentators had decided it was expensive and beginning a long-term reversal. There was remarkably little consideration for interest rates and yields in the US.

The sanguine outlook for equities was eventually tested when US bond yields rose sharply in January to the point where they could no longer be ignored.

Politics and the USD

Trump’s economic policies were always potentially quite bullish for the USD – tax cuts and infrastructure spending were likely to boost growth and threaten to push up inflation, creating the potential for faster rate rises. The trade policy also threatens to dampen global growth and boost imported inflation, both of which were potentially bullish for the USD.

From the outset of the Trump presidency, his administration was absorbed with repealing and replacing Obamacare and spending much time on immigration policy. Infrastructure spending was on the back-burner, and it appeared that tax reform would also become stalled.

Furthermore, Trump has been dealing with the controversy over Russian meddling in the election and the Mueller investigation. He has proved to be a highly controversial and divisive President on social issues.

For much of 2017, the market lost confidence in the ability of Trump to deliver on economic policy reform and the market often feared political instability.

Even after Trump and Republicans delivered on tax reform, it has taken the market a while to view Trump’s administration as positive for the economy. Political instability remains with Trump’s approval rating still low and odds favouring the Democrats regaining control of the House of Representatives in the November mid-term elections (if not both houses). The Muller investigation is also tightening the noose around Trump associates and remains a potentially destabilising event for the US government.

A high turnover of Trump’s cabinet and a shift in the policy agenda to trade policy initially exacerbated the sense of political instability and appeared to weaken the USD in March/April. However, trade protectionist policy has switched from a negative to a positive for the USD, via threatening the outlook for global growth, while raising inflation risks in the USA.

Political uncertainty remains, however, the Trump policies that were initially viewed as a positive for the USD in the first months after his election are returning to the foreground.

Trump is also asserting more leadership of his cabinet and proving resilient to media criticism and controversy. He can claim wins on tax policy, increasing spending for the military and gaining more stability in the passage of spending bills. He is arguably gaining traction with his trade policy agenda, and may have helped bring peace on the Korean peninsula.

Political risk in the US remains; Trump remains a polarising leader, but he is making progress on his agenda and contributing to a stronger more confident economy.

Uncertainty is now rising around Syria and Iran, but rather than weakening the political position of Trump, his more assertive foreign policy team may be improving his approval at home while generating more geopolitical risk in the global economy.

When do twin deficits matter?

A key risk for the longer term outlook for the US economy is a growing fiscal deficit and wider current account deficit.

We contend that the market should defer its concern over these big-picture fundamentals to a time when it seems US rates and yields have peaked. And there is a clearer understanding of how the tax cuts, deregulation and trade policy have combined to influence growth and potential output in the USA.

If the deficit becomes a problem, it is likely to first present itself via inflationary pressure and higher US yields. However, if inflation more clearly moves ahead of the Fed’s target, the Fed is likely to raise real rates to slow domestic demand. In this instance, the USD may rise until rates appear to slow demand.

At some point the USA may find itself with large twin deficits, slowing economic momentum and peaking yields. At that time, perhaps from a position of a more expensive USD, we should start to fret about twin deficits and the need for fiscal consolidation even as the economy is peaking.

At this stage of the game, it seems too early to be worrying deeply about a risk premium related to twin deficits driving down the USD.

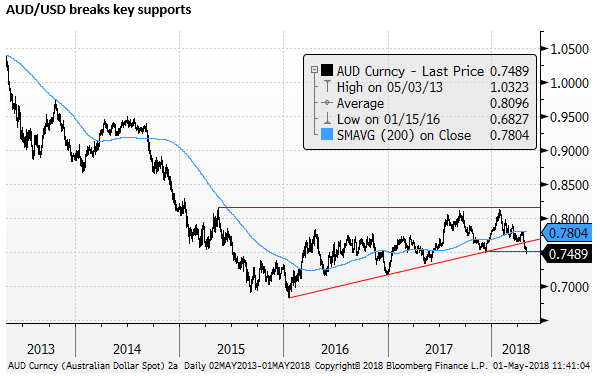

AUD breaks key support

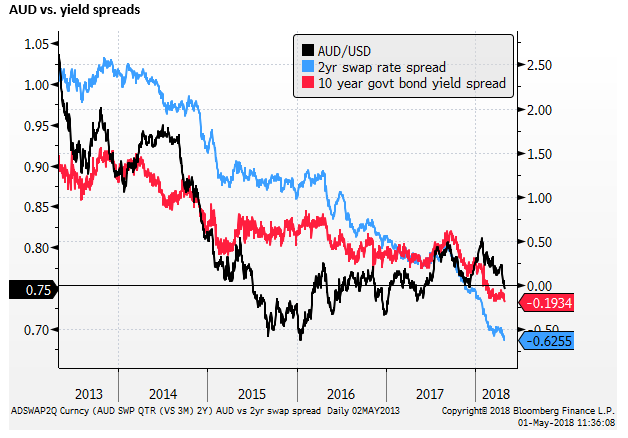

The AUD has exhibited many of the attributes of the USD described above. It has been surprisingly strong given its yield advantage over the USD has been eliminated, but it now appears to be reconnecting to its now negative yield spreads.

The AUD has broken below an uptrend line over the last few years, and below its previous low in December last year (around 0.75), after making a double top in January.

RBA would welcome a weaker AUD

The RBA said in its policy statement on Tuesday that, “The Australian dollar has depreciated a little recently, but on a trade-weighted basis remains within the range that it has been in over the past two years. An appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast.”

Apart from noting its recent depreciation, this has been its standard statement for some time. The RBA is not against further depreciation of the currency, which would help lift inflation that is below its target range.

The RBA said, “Inflation is likely to remain low for some time, reflecting low growth in labour costs and strong competition in retailing.”

RBA Governor Lowe noted in a speech on Tuesday that the target policy cash rate has been unchanged at a record low of 1.5% for a record length of time – 21 months. You get the impression that he is quite looking forward to the day when he gets to hike rates for the first time in his tenure. He has said on various occasions this year that “it is reasonable to expect that the next move in interest rates will be up.”

However, on the RBA’s current forecasts, a hike is not likely for quite some time. Lowe said, “In our discussions today, though, the Board again agreed that there was not a strong case for a near-term adjustment in the cash rate.”

The RBA might quite like a weaker AUD to help bring forward the date when it gets to lift rates. The RBA has in recent years been reluctant to cut rates for fear of exacerbating household debt and financial stability risks.

Uncertainty over RBA rates policy

The AUD is weaker in line with emerging market currencies in recent weeks and faces direct risks from the protectionist trade policies of the Trump administration; including pressure directly on China to reduce steel production and more broadly on Chinese trade policies.

AUD also faces risks from Chinese policy aimed at tightening up on loose lending practices in its shadow-banking sector.

Australian economic growth has been running above potential, supported by infrastructure spending and stronger global growth. Business confidence has been well above average for some time, and the RBA is witnessing a gradual return to full employment and a rise in wage and inflation growth from low levels.

However, risks to a sustained recovery also come from a weaker housing market that continues to face headwinds from rising bank funding costs, political uncertainty ahead of the national election early next year, and pressure on the financial sector arising from the Royal Commission into its misconduct.

These considerations are making the timing of any rate hike much more uncertain.