Short-term pain, long-term gain

China may have decided to bear down a little harder this year in dealing with the necessary restructuring of its economy and market reforms. The accelerated fall in CNY suggests it may allow more flexibility in the currency this year than most thought. This is likely to prove to be a bigger weight on global asset markets and commodity currencies, exacerbated by a large excess supply in oil and metals markets, and we expect further significant declines in the AUD and CAD. The associated more rapid decline in central bank and sovereign wealth fund FX reserves may tend to boost the USD more than expected this year, essentially generating a shortage of dollars. A tendency for a strong USD and sticky US interest rates are likely to add downward pressure on US equities and ensure global risk appetite remains constrained this year. However, low energy prices supporting consumer spending and rapid innovation in the IT sector may offer stability to global growth and asset market confidence. The EUR remains over-valued, in our view, with respect to the extreme policy settings of the ECB, and while it may be supported to some extent by persistently lower levels of risk appetite, it is likely to resume its down trend during periods of consolidation in risk appetite.

Lights are on in Breckenridge Colorado

Amplifying Global FX Capital has turned on the lights in its new office in Breckenridge Colorado and this is our first report for the year after a long break over much of December. It has been a tumultuous start to the trading year with China and oil center stage. This report is our attempt to consider some of the broad thematic trends that will play-out this year.

China is now deep in the process of attempting to re-engineer its economy and deal with the excesses of the boom years in the 2000s it has experienced much greater financial market and exchange rate volatility over the last year and this has spilled over to global asset markets more than at any time in the past.

The actions of the Chinese government over the last year and recent press reports suggest that China may be leaning towards speeding up market reform at the expense of weaker economic growth.

While it has worked valiantly to prevent growth from deteriorating too rapidly, the central government may have decided to accept more short term pain for longer term gain. That appeared to be the message delivered to the market in the ‘People’s Daily’ press report earlier in the week that preceded the sharp Chinese stock market decline and currency sell-off.

The fact that the government has allowed more rapid currency depreciation may be a sign that they are looking to implement more market reform and discipline on the domestic economy. The sharp fall in the Chinese equity market reflects sentiment that the government will not as easily be drawn in to prop up a sagging market.

It is also relevant that the government has been implementing a corruption crack-down for over a year. This may have cleared out vested interests in state-own companies and bolstered the political power of the central government, such that it can proceed with reform and withstand the social and political fallout from weaker economic growth more readily.

If so we should expect China to continue to be a drag on global growth in 2016 and volatility in its financial markets and currency may continue to play an increasing role in global market sentiment, tending dampen asset markets globally.

The Increasing influence of China on global markets

The Chinese economy is moving more clearly through a significant turning point in its long term development. Its heavy industries and construction sector have peaked after a decade of rapid growth and it is seeking new growth engines in the service and high tech sectors led more by domestic consumption as its export markets mature. It also dealing with a run-up in debt associated with the boom times that is now restraining growth potential.

To prevent a wholesale collapse in the economy, the government is being forced to accelerate market reforms and open its economy to find these new engines of growth.

It is also using an arsenal of quantitative monetary policy measures and directives on its financial sector to stabilize internal financial conditions as it attempts to reduce excesses in debt and capacity in heavy industrial sectors.

The Chinese government is both trying to accelerate market reforms but overlay adhoc direct controls and at times underpin capital markets in stress. As such it is often accused of lacking direction and sending conflicting signals.

There are a lot of balls in the air in China, generating market uncertainty, spilling over more significantly to global markets in 2015.

One consequence of this mix of policies in China was a surge in its stock market from around mid-2014 to a peak in June 2015 by around 150%.

The expanding bubble had only a mild positive influence on other Asian and global equity markets. But the pop between June and Sep when the market fell by over a third was much more influential contributing to broader market uncertainty and unsettling global market confidence.

The weak start to this year in Chinese equites reflects fears that the government will not continue to support the market at every turn; again this has spread more readily to global markets.

China’s exchange rate policy conundrum

The weak trend in Asian region and in general emerging market currencies in 2015, after broad-based USD strength between mid-2014 and Q1-2015, was probably a factor that contributed to a sudden devaluation of the Chinese currency in August 2015. The relatively strong CNY, tightly linked to the strong USD, was contributing to a weaker Chinese export performance, exacerbating a weaker growth trajectory for the Chinese economy.

But a stable CNY policy was also helping contain capital outflow and support the government’s efforts to sustain adequate domestic money market liquidity.

In August, China took a risk and changed tack, allowing the currency to fall sharply and then gradually implement a policy of greater flexibility. The aim was probably to take the pressure off its traded goods sectors.

The initial devaluation in August was a shock to the market and contributed to global market upheaval that was already shaken by the pop in the Chinese equity bubble.

China probably accepted that it may have to step in to contain excess volatility in the currency, upping its intervention in August and September, while hoping to reduce intervention over the medium term.

However with the genie out of the bottle, the likelihood is that China will face more capital outflow as the market speculates on how far the CNY may weaken within the government’s new regime of allowing more flexibility and responsiveness to global currency trends.

In more recent months since October, the Chinese government has attempted to step back from intervention and implement its new policy to allow more CNY flexibility. This has resulted in a steady depreciation in the CNY.

The steady depreciation from around end-October established a trend, fueling more negative sentiment, boosting capital outflow. The rise in USD/CNY above key levels (6.5 on the fix and the highs after the August devaluation) appears to further sparked more capital outflow. It suggests that the Chinese government is willing to accept more currency mobility than the market may have thought.

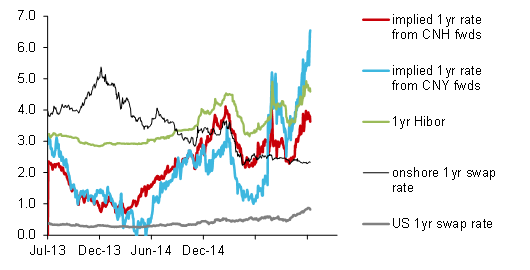

Offshore CNY (CNH) has fallen further than the onshore or non-deliverable exchange rate. And the forward curves in both the offshore CNH market and non-deliverable CNY markets have steepened, pointing to market expectations for further significant depreciation this year and raising the effective borrowing cost for CNY in offshore markets.

Even though onshore borrowing costs remain low and contained by central bank liquidity injections to counter faster capital outflow, less creditworthy borrowers in China that may rely more on offshore funding may find their access to finance more costly.

Effective CNY 1-year interest rates

(Source: Bloomberg, AmpGFX)

The weaker trend in the CNY at this stage has spread to weaker currencies in the Asia region; including the AUD.

As countries in the region and globally now look to China as one of their major trading partners, how their currencies behave with respect to the Chinese currency will depend much on the feedback on the outlook for the Chinese economy.

If the CNY falls as a consequence of a weaker outlook for China in the context of greater uncertainty in its financial markets (as seen in the last week), then regional currencies are likely to weaken in concert with the CNY. If the CNY is weakening in the context of stable Chinese financial markets and stable economic sentiment, then regional currencies may strengthen despite the CNY depreciation.

Commodity cycle to remain depressed

The adjustment phase in the Chinese economy has had a major impact on commodity prices, particularly for industrial metals.

China typically accounted for around half of total world demand for most industrial commodities in the last few years of the commodity boom and many thought the rapid pace of its demand growth might extend for much longer. The levelling off in demand from China in the last year has come just as considerable new production capacity has come on stream. There now appears to be significant excess mining capacity and commodity prices have collapsed.

Prices have fallen to levels that might force higher cost producers to moth-ball their mines and prices may start to stabilize. A moderate rise in commodity prices might ease the strain somewhat, but the commodity boom is now well over and it will take years to absorb excess capacity. The financial stress in the resources sector may linger well into 2016.

The Chinese economy is unlikely to revert to a rapid pace of fixed asset investment for the foreseeable future. We might expect stagnant demand from China for another year or several years, followed by much more gradual growth in subsequent years. Unless other emerging markets, the most likely candidate may be India, can move into a more rapid development phase, then commodity markets are likely to remain depressed. It is hard to say whether they have hit bottom or not, and rallies will be met with skepticism for the foreseeable future.

Sticky US rates and strong USD to undermine US equities

Another view I am developing is that the strong USD and rise in US interest rates is going to prove stickier in the year ahead and contribute to downside pressure on US equities. We are seeing this unfold in the first week of the year – while US rates have come down somewhat this week, they remain significantly above levels through much of last year. In light of relatively soft US economic data in the last month, and a fall in the US equity market to a low since the Q3 slump last year, US 2yr rates are relatively high and sticky.

US 2yr swap rates and US S&P500 equity index

FX Reserve managers need more dollars

We may be moving into a phase where the USD is receiving more external support from a weaker trend in CNY and weaker commodity prices undermining resource producer currencies.

More rapidly declining central bank and sovereign wealth fund FX reserves are likely to support the USD. The build-up in these reserves generated demand for alternative reserve currencies like EUR & AUD up to 2012/13 as reserve managers diversified growing USD reserves. The decline in reserves should now result in the sale of these alternative reserve currencies as reserve managers attempt to replace dollars lost during intervention to support their own sagging currencies. The much weaker oil price and more intense selling pressure on CNY suggests that FX reserves are likely to have declined more rapidly in recent months and will continue to fall more rapidly in 2016.

The chart below looks at the proxy for intervention in China (net sales of FX by Chinese banks). It points to record sales of FX and purchase of CNY by the Chinese central bank in July, August and September last year and significant sales in November (the last data point available).

Net FX purchases by Chinese banks (US$bn)

(Source: Bloomberg, AmpGFX)

Upward pressure on the USD and sticky US interest rates are likely to undermine US equities. We might find that weaker US equities contributes to a sense of risk aversion in global markets that might have the roots in uncertainty in China and weak energy prices.

Higher Global Risk Premia

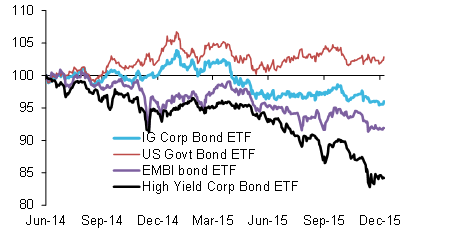

Global risk aversion or risk premiums have been rising since mid-2014, picking up pace from mid-2015. This reflects several factors. Initially it may have been mostly related to an approaching US rate hike, major central bank policy diversion and the rapid rise in the USD from mid-2014 to Q1-2015. This spilled over to much weaker oil prices over the same period exacerbated by Saudi Arabia’s decision not to continue its traditional role as price stabilizer. Weak oil prices have undermined several large emerging market economies and energy sector assets in 2015, contributing to much higher risk premiums in emerging market and high yield bond markets.

The chart below shows weaker trends and widening under-performance of US corporate, particularly high yield, and emerging market bond exchange trade funds relative to a US government bond ETF since mid-2014 (accelerating since mid-2015)

(Source: Bloomberg, AmpGFX)

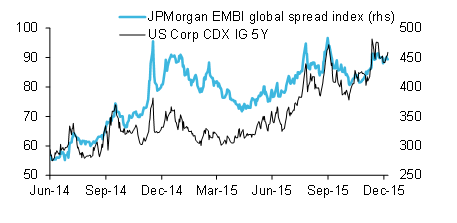

Similarly the chart below shows rising risk premiums embodied in the US corporate investment grade CDX index and the JPMorgan Emerging market bond spread index (over US Treasuries).

(Source: Bloomberg, AmpGFX)

EUR struggles to benefit from risk aversion

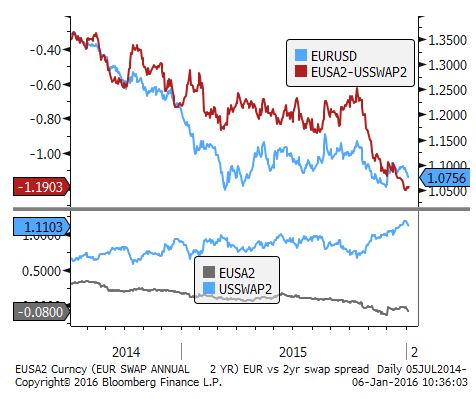

The JPY is one of the few currencies to have strengthened against the USD in the first week of the New Year, whereas the EUR has fallen modestly. We are in a ‘risk-off’ mode where traders are inclined to reduce leverage, which should support the lowest interest rate currencies; including both EUR and JPY. But only JPY has strengthening suggesting that EUR may be more fundamentally challenged.

EUR is firmer against most commodity and Asian currencies, but its lack of bounce in recent days suggests that if risk appetite improves it might fall more rapidly against the USD.

Even though the ECB didn’t live up to expectations for more aggressive easing on 3 December, it still pushed rates further below zero and extended the projected time-frame for its QE policy.

In the broad-frame, EUR consolidated throughout most of 2015 and it does not appear to have yet reacted to a significant further widening of its interest rate disadvantage against the USD since October last year.

It may be the case that the EUR has not been as reactive to interest rate differentials in the last year in an environment of widening risk premiums (weaker investor risk appetite). And it needed to consolidate after its sharp falls from mid-2014 to Q1-2015 in anticipation for the ECB QE and US policy tightening.

We expect risk appetite to remain contained this year, but it is likely to wax and wane, and after a long period of consolidation and further central bank policy diversion, the fundamental case for a weaker EUR/USD should play out this year.

EUR/JPY has already decisively broken its 3-Dec ECB level, highlighting the difference between the policy stances of the ECB and BoJ that we discussed late last year in several AmpGFX reports. The BoJ may at some stage revert to worrying about strength in the JPY, but they are seeing progress on generating inflation expectations and are much more reluctant to adopt negative interest rates.

EUR/JPY falls below sharply below 3-Dec ECB date