Stable genius or dumb luck, Trump gets a weak dollar

This won’t necessarily sound ground-breaking for many market observers, but the weak USD reflects the bull market in global equities. Interest rate differentials are playing a very limited role in the FX market, less so than they have for a long time. The divergence between interest rate spreads and many currencies’ exchange rate to the USD is around historical wides. Several factors are accentuating this divergence and may continue to do so for some time.

It’s equities stupid

Equities are rising everywhere, supported by synchronized and stronger global growth. Investors are chasing returns in equities; there is not a lot of focus on alternative strategies; including currencies and their interest rate carry.

EUR turns from rates to equities play

Equity investors prefer to take on the currency risk attached to their equity position; they need a good reason to hedge. In the recent past (before 2017), investors in European equities were inclined to hedge their EUR exposure, seeing it as a weak currency due expansive monetary policy, and political and macroeconomic risk. However, that mentality has changed. The European economy is in a broad, robust recovery, political risks have receded, and monetary policy easing is being gradually unwound.

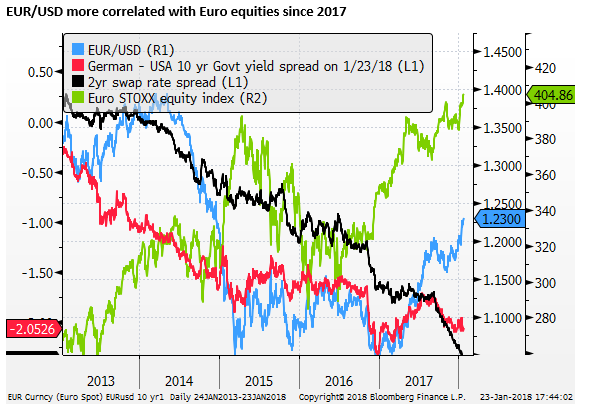

The robust European economic recovery is fueling confidence in its equity market, and equity investors in Europe are no longer so interested in hedging their EUR exposure, notwithstanding the deteriorating EUR/USD yield spread providing increased carry return for selling EUR/USD.

While the EUR/USD was more aligned to its interest rate spreads in the period from mid-2014 to end-2016, and remained correlated with long-term yield spreads into mid-2017, more recently it has become more correlated with European equities.

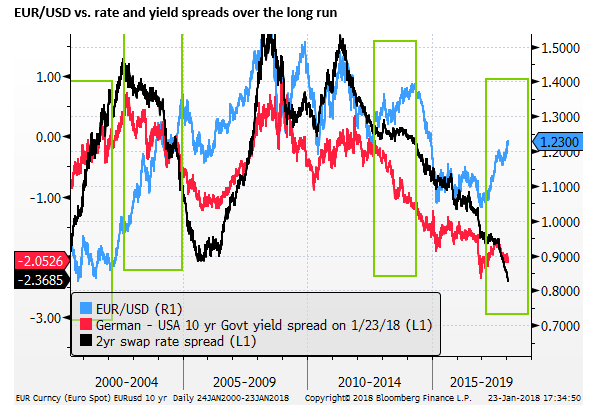

The EUR/USD has diverged for many years at a time from its yield spread. While the recent divergence in EUR/USD from rate spreads is wide, it is not unprecedented.

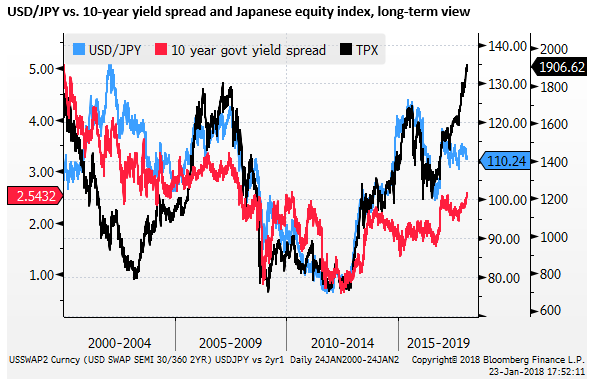

JPY trading more like the EUR

Equity investors are also bullish Japanese equities. They can see Japanese monetary policy easing at its peak, even if it may be some time before it sees any significant unwind in policy easing.

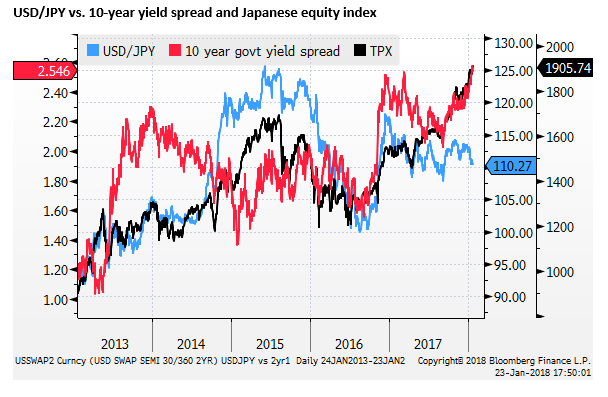

Traditionally, investors, including Japanese investors, used the JPY as a funding currency for bullish, leveraged global investment. As such, JPY tended to be negatively correlated with global equities, including Japanese equities. This negative correlation only increased during most of the quantitative monetary easing era since 2013, as the policy was designed to both boost asset prices and weaken the exchange rate. And the weaker exchange rate tended to enhance equity value.

However, the negative correlation between the JPY and Japanese equities broke down in 2017, and more recently JPY is diverging from its yield spreads.

Investors in Japanese equities are more confident in a sustained recovery in Japan. And they are encouraged by corporate reform, including an increased focus on governance and return on equity. They perceive BoJ policy easing at its peak, and in a long-term sense, the JPY is viewed as relatively cheap. As such, equity investors in Japan are no longer routinely hedging their currency exposure. Furthermore, there is much less interest in selling JPY to fund investments in global assets or pursuing short JPY carry trades.

Investors in Japanese equities are more confident in a sustained recovery in Japan. And they are encouraged by corporate reform, including an increased focus on governance and return on equity. They perceive BoJ policy easing at its peak, and in a long-term sense, the JPY is viewed as relatively cheap. As such, equity investors in Japan are no longer routinely hedging their currency exposure. Furthermore, there is much less interest in selling JPY to fund investments in global assets or pursuing short JPY carry trades.

In light of the recent experience of witnessing a strong rise in EUR in 2017, despite only a very gradual ECB monetary policy easing unwind, investors are now very wary of selling JPY. Japan, like the Eurozone, has a significant current account surplus, and without capital outflow, including carry-trades in currency markets, equity-related capital inflow may continue to boost the JPY.

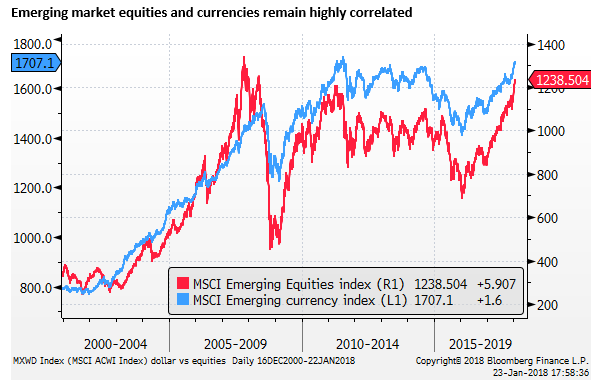

Emerging markets in bull-market

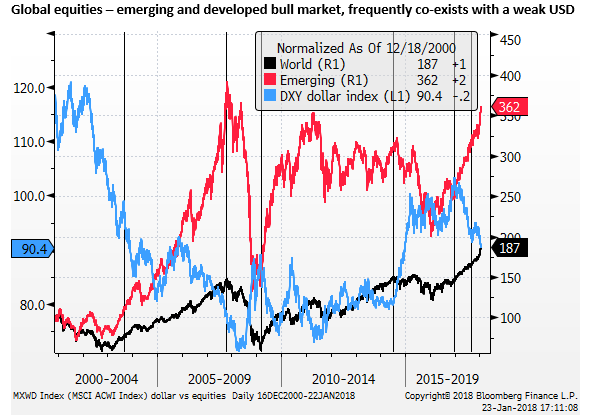

Emerging market equities have been strongly out-performing developed markets since their recent low in early 2016; the MSCI emerging market index has risen to a high since 2008. Emerging market currencies are historically more highly correlated with their local equities. As such, it is less of a surprise to see stronger emerging market currencies in the current environment.

Broad-based USD decline

When you have the two largest non-dollar major currencies rising vs. the USD, in defiance of their narrowing yield advantage, and emerging market currencies rising against the USD, then the USD decline starts to look very broad-based.

As such, the market tends to pay less attention to news that might be bullish for the USD, but react more to positive developments for other currencies.

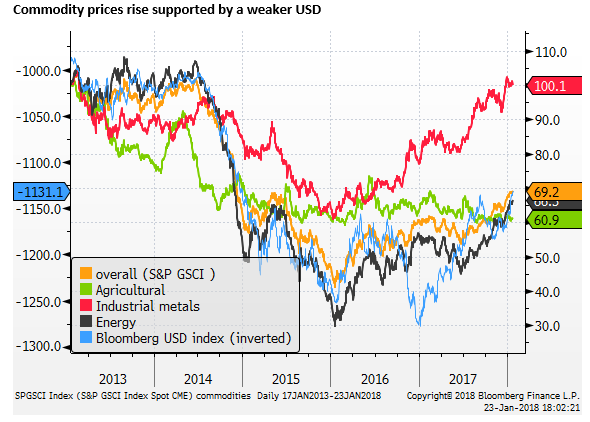

In conjunction with stronger global demand, a weaker USD is also contributing to higher commodity prices. This then tends to support growth, assets, and currencies in commodity-driven economies. Further adding to the breadth and power of the USD decline.

Pre-crisis redux

The market has moved beyond the crisis mentality that defined much of the period from 2008 to 2016, into a more buoyant mood where the global economy and assets are viewed in a sustained growth phase. In many respects, the current market environment feels more like the pre-global financial market crisis era, from 2004 to 2007. Like the current phase, since 2017, the USD tended to weaken against most other currencies in the few years before the 2008 crisis. A notable exception at that time was the JPY. At that time, carry trades, funded out of the JPY, were very popular.

Risks are being built into the global markets that will eventually cause a correction in equities and the associated fall in the USD. We are reluctant to sell the USD at this juncture but admit that it can continue to fall for some time.

The market is in a mood to look past developing risks; including tariffs implemented by Trump on Solar and Washing Machine imports. Individually these measures may not be significant, but they point to a protectionist trend that might undermine confidence in emerging markets, and raise inflation expectations in the USA, prompting higher yields that might undermine equities and strengthen the USD.

Perhaps the most obvious risk to the sanguine view in global equity markets is rising inflation pressure in the USA. The weaker USD itself will tend to raise inflation pressure in the USA. (Multiple upside risks for US bond yields; 18-Jan – AmpGFXcapital.com)

Stable Genius

The fact that Trump is achieving a weaker USD at the same time as big tax cuts and protectionist rhetoric, both of which should boost the USD, is a win-win for Trump.

The tax cuts should boost US growth, are inflationary, and are designed to draw in capital investment. The trade policy is also directly inflationary, and might tend to narrow the trade balance. These policy developments, all other things equal, should boost the USD. However, the genius of Trump is that he has been able to implement these policies and weaken the USD. The weaker USD also tends to boost US equities, a metric by which Trump asks the Amercian public to judge his leadership success.

The increased political uncertainty in the USA since Trump was elected is probably also contributing to a weaker USD. Rolling threats of a government shut-down, closely tied to the immigration debate, are adding to political uncertainty and helping keep the USD weak.

Whether by design of a stable genius, or dumb-luck, the weak USD is helping Trump claim he is a brilliant economic manager.