Trump equity rally resumes; UK industry defies Brexit fears; Australia’s relatively low inflation

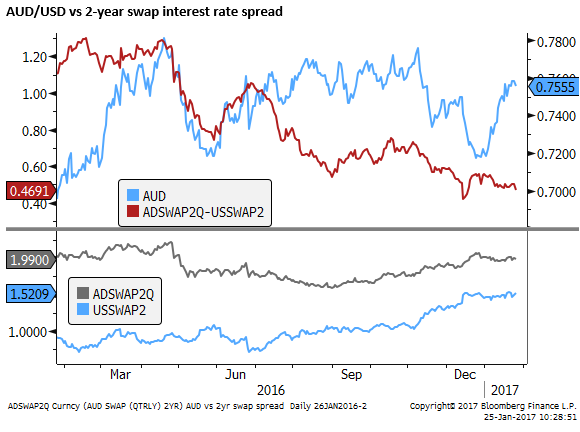

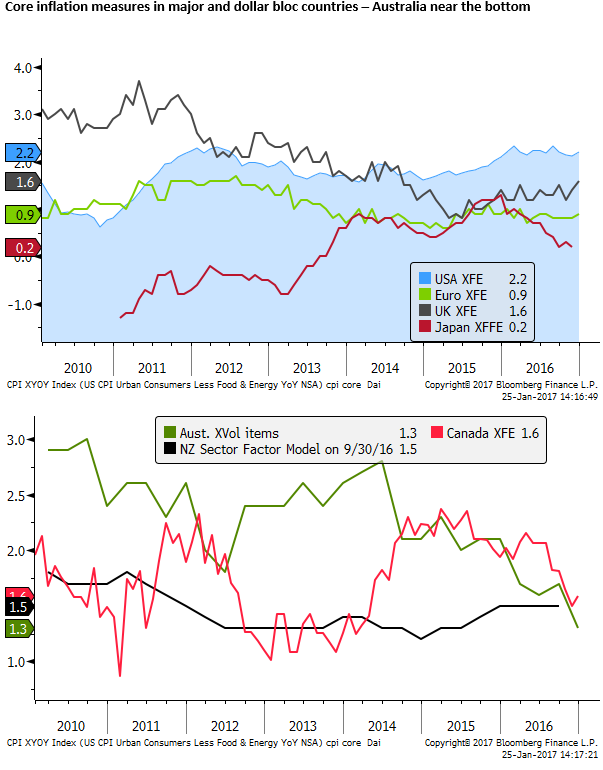

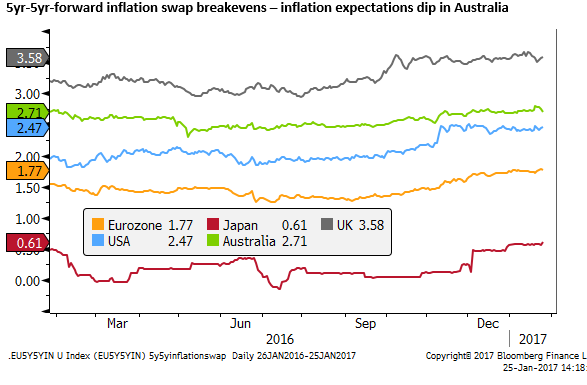

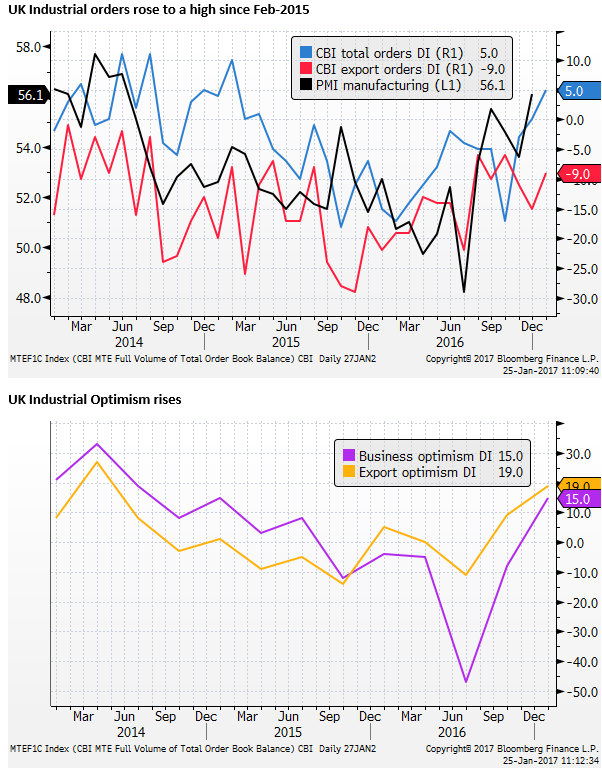

Australian inflation momentum wanes and makes it the lowest inflation country in major and dollar bloc countries after Japan and the Eurozone. Market-based long-run inflation expectations also dipped in Australia. The relatively strong AUD continues to weigh on the inflation outcomes. The RBA is unlikely to rush to cut, but appears further away from raising rates. Higher commodity prices continue to help support the AUD, but downside risks are significant with Trump policies set to support the USD and increase risks for Asian exporters. Rising global yield trends also pose a risk to highly indebted Australian households and its expensive housing market. US equities resume gains, led by homebuilders, construction materials and construction and engineering. As Trump moves forward on his agenda to build walls and pipes, his policies may be reasserting their positive impact on equities and yields. The USD has so far been slower to resume its rally. USD/JPY is diverging from its recent positive correlation with US yields, but it may soon resume its rising trend. US economic data continue to show improvement. Mortgage applications for home purchase rose despite higher mortgage rates, consistent with confidence in homebuilder equities. The UK Industrial trends survey showed strength and optimism, continuing to defy fears of Brexit. The lower GBP appears to be boosting exporter optimism. The prospect of a love-fest between Trump and UK PM May on Friday may be generating further gains in GBP. A softer German IFO survey and concerns over political risks in Europe may keep EUR capped.

Australian inflation slows below peers

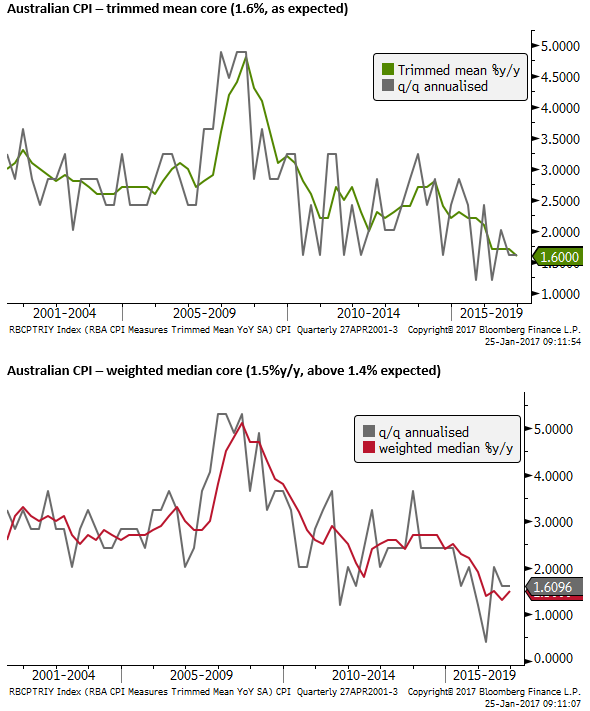

The main underlying core inflation measures were flat in Q4 from Q3 in quarterly terms (0.4%q/q), suggesting that the impulse for inflation is still significantly below the RBA’s 2 to 3% medium-term target range, supporting the case for more or, at least, more prolonged accommodative monetary policy.

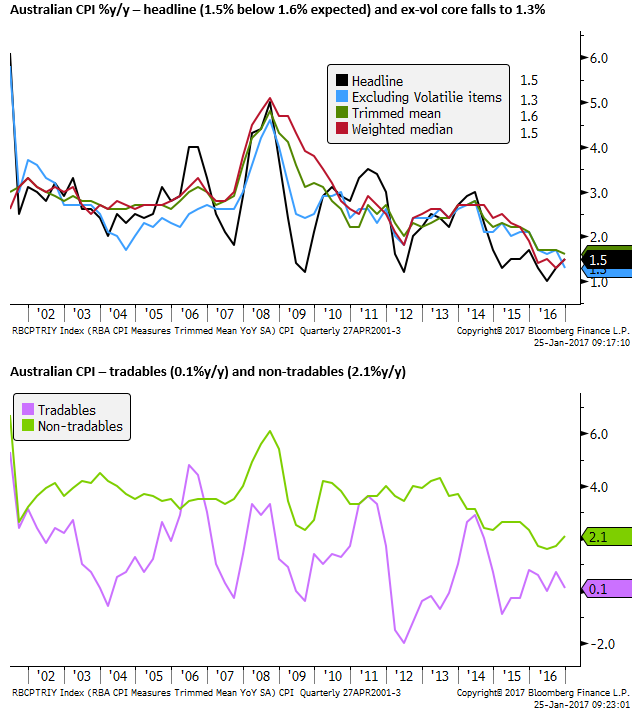

The tradable component remained weak at 0.1%y/y, consistent with ongoing strength in the AUD exchange rate. The non-tradable component, more indicative of core inflation trends, rose to 2.1%, although this was boosted by an increase in the excise tax on tobacco, and a shift in tobacco from the tradable to the non-tradables category. Tobacco prices rose 13.2%y/y.

Furthermore, “market goods and services excluding volatile items” was up 0.5%q/q and only 0.8%y/y. And, “all groups excluding volatile items” (shown in the chart below) was up 0.3%q/q and only 1.3%y/y. These lesser watched underlying measures fell further below target.

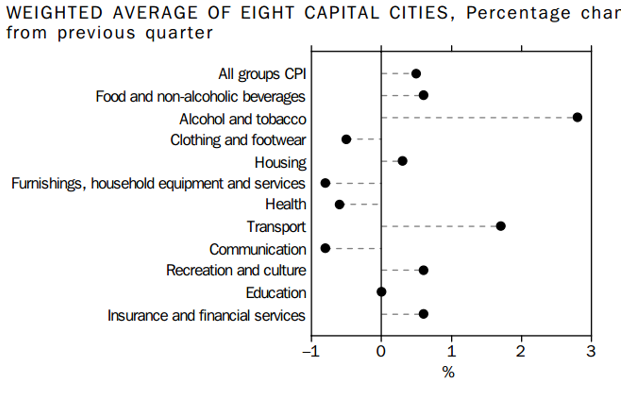

The main increases were driven by tobacco (+3.4%q/q) and fuel prices (+6.7%q/q)

Following the data, June 3mth bank bill futures yields fell 3bp to 1.80%. Cash rate futures are projecting a slight risk of a rate cut in the first three-quarters of the year, suggest that the RBA is likely stay with a stable 1.5% rate setting for the foreseeable future.

Core inflation readings in many other countries, including the USA, UK and Eurozone are exhibiting rising trends. Given the sharp fall in JPY in recent months, we might expect it to increase soon in Japan. However, Australian core inflation appears to be in a more protracted slow-patch, suggesting that it may be longer before Australia resumes tightening monetary conditions.

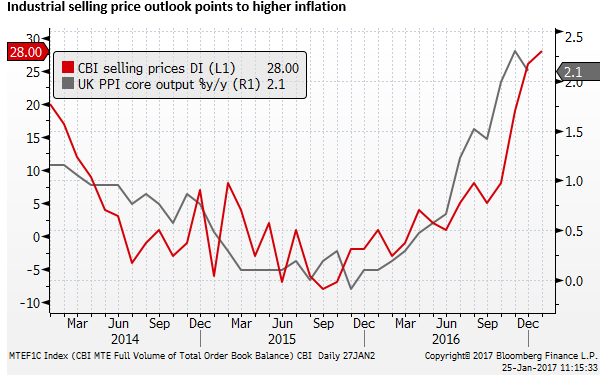

UK industry continues to defy Brexit fears; May set to be the first to embrace Trump

GBP firms ahead of UK PM Theresa May’s visit to the USA to be the first foreign leader to meet USA President Trump, to reaffirm the greatest bilateral relationship God ever created, it’s going to be great trade deal, it really is, it’s true.

The UK CBI survey of industrial trends showed a rise in its total orders diffusion index to +5, a high since Feb-2015, more than +2 expected. The export orders balance also increased, although, at -9, is not as high as it might be considering the weaker exchange rate.

The CBI quarterly business optimism survey (+15) rose much more than expected (-8); export optimism outlook (+19) rose to a high since April-2014.

The CBI diffusion index for selling prices in the next three months rose to a high (+28) since 2011, even though not quite as high as expected (+30), pointing to more inflationary pressure ahead

The trends continue to suggest that the ravages of Brexit are yet to make a mark on the UK economy. The economic and inflation trends place upward pressure on UK rates and may put upward pressure on GBP.

The UK Supreme Court on Tuesday ruled that UK PM May must pass a bill in parliament to proceed with Brexit. May therefore must do so before end-March to meet her target date for triggering the so-called “Article 50” process. This increased uncertainty somewhat, but was expected. The Article 50 bill will be published on Thursday. Debate is supposed to begin on Tues/Wed next week. The full process towards passage is likely to last until mid-March.

On Wednesday. May also made a concession to critics of Brexit, agreeing to release a ‘White Paper’ on her government’s approach to Brexit negotiations. A PM spokesperson said the paper is “a separate issue” to the Article 50 bill, and it is unclear if it will be published before the Article 50 bill is passed.

Theresa May promises white paper on UK’s Brexit plans – FT.com

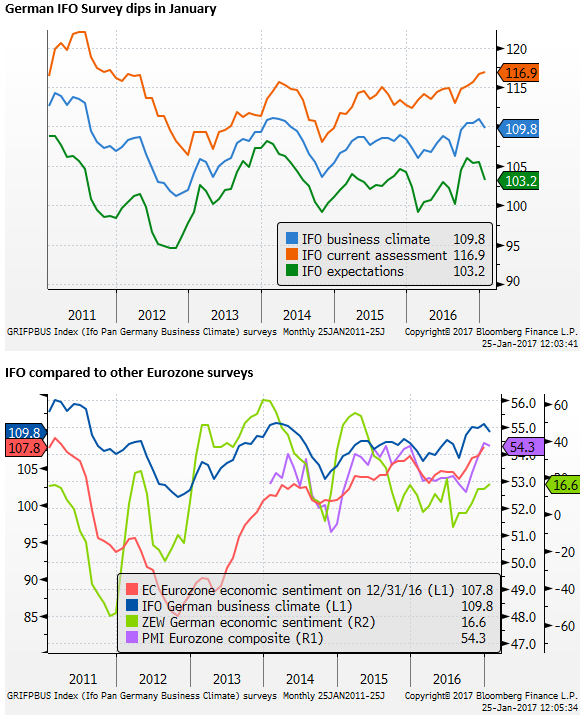

German business confidence wanes

The German IFO survey of manufacturing, trade, and construction was less optimistic. Business climate fell from 111 to 109.8 in Jan, led by the expectations component that fell from 105.5 to 103.2. The current conditions component still rose, although a little less than expected.

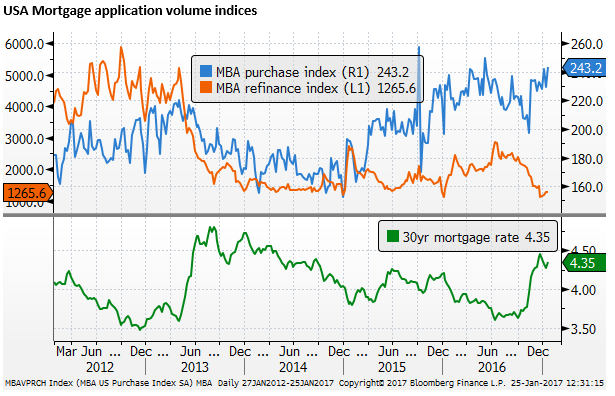

US mortgage applications rise despite higher rates

USA MBA weekly mortgage data showed a rise in the index for home purchase to around the highs in Q2 last year, the highs in the index since 2010. These are not high levels compared to pre-global financial crisis levels, but it is noteworthy that mortgage demand has firmed despite the rise in mortgage rates since Q3 last year.

This may reflect easier lending conditions applied by banks and confidence in the housing market. House buyers may still view the level of mortgage rates as historically low, even though they have risen significantly in recent months, and may be more willing to borrow, sensing rates are now in a rising trend.

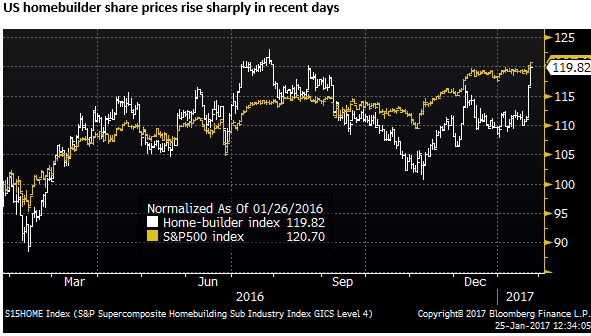

Consistent with evidence of firming mortgage demand, homebuilder share prices have searched in the last two sessions, supported by the earnings report from the largest builder DR Horton on Tuesday.

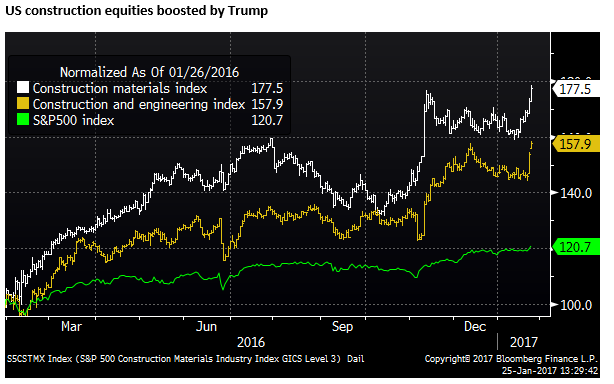

Trump equity rally resumes

USA construction and building material sector equities have also risen strongly in recent days. Market commentaries suggest they are drawing support from Trump’s plans to build a wall on the Mexican border. He has also revived the Keystone XL pipeline into Canada and the Dakotas Access pipeline.

His vision for toughening trade, promoting manufacturing at home and boosting infrastructure spending are likely to boost confidence in heavy industry and construction industries.