Where does Trump’s rubber hit the road?

The markets are moving well before the rubber hits the road on the Trump presidency. Trump will have perhaps the most power of any President in decades with Republicans controlling both houses of Congress, but it will take months and even years before many of his wide range of loosely formed policies are implemented.

It appears that some of his more contentious social policy agenda that might threaten growth and confidence have taken a back seat, but he is still facing significant protests in the wake of his election and will need to walk a fine line to placate his supporters that will want quick action on anti-immigration and anti-trade policies, while appeasing the protesters and promoting national unity after a divisive close election.

There is significant scope for market upheaval to continue with competing influences of pro-growth infrastructure spending and weak growth anti-trade, anti-globalization, and anti-establishment politics spreading to Europe. The fall in energy prices also threatens to undermine confidence and reverse some of the recent resurgence in inflation expectations and yields.

There were signs that a global recovery was developing before the Trump election, USA employment data just ahead of the election was solid with higher wages, and consumer confidence released last Friday was stronger with a lift in inflation expectations. Emerging markets, including India, Russia, and Indonesia, have been pursuing reformist agendas that are reaping growth rewards.

The infrastructure expansion message from Trump has been the most forthright since his election. It has struck a chord in the global market with this trend already developing before the election as more nations turn to fiscal expansion as they run out of monetary policy ammunition to boost growth.

As such, we see the rise in global bond yields as durable and likely to have persistent effects on global currency markets. Higher yields will tend to make the Japanese Quantitative Yield Curve Control monetary policy more effective and contribute to a weaker JPY. However, working against the recovery in USD/JPY could be lower energy prices and fears and possible risk aversion that may arise from other aspects of Trump’s policies.

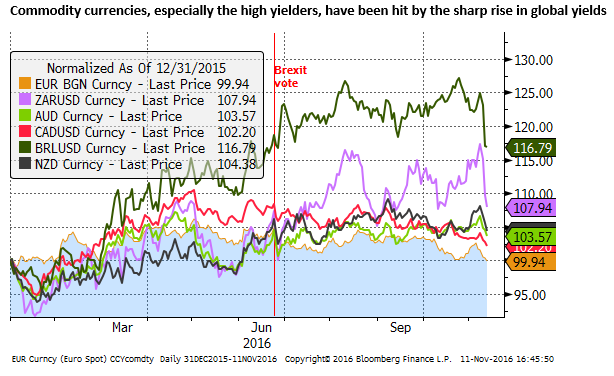

The Fed is likely to move forward with a rate hike in December and sound less dovish this week, keeping some upward pressure on the USD more generally. Surging industrial metals prices may support the AUD more than NZD and other high yielding commodity currencies. However, the USD may continue to benefit against all EM and commodity currencies as fears over anti-trade policies and higher US yields continue to influence investor sentiment.

To the Victor go the spoils

The Trump election has unleashed a range of significant moves in global markets. The USD has risen sharply against most currencies on hopes he will generate rapid growth in infrastructure spending and cut taxes.

He is also expected to move more quickly to change the tax code to encourage USA companies to repatriate offshore earnings.

Global bond yields have shot up, lifting the USD against low yielders (JPY, Gold, and EUR) and weakened a range of high-yield commodity and emerging market currencies on unwinding of carry trades.

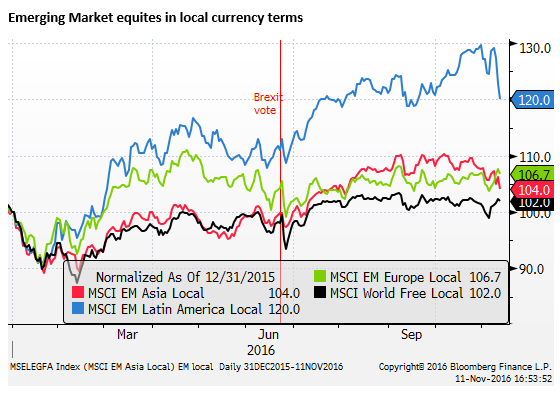

His anti-trade, anti-globalization views have further undermined trade dependent emerging market currencies, more so in Asia and Latin-America. While his conciliatory tone towards Russia has lifted Russian equities.

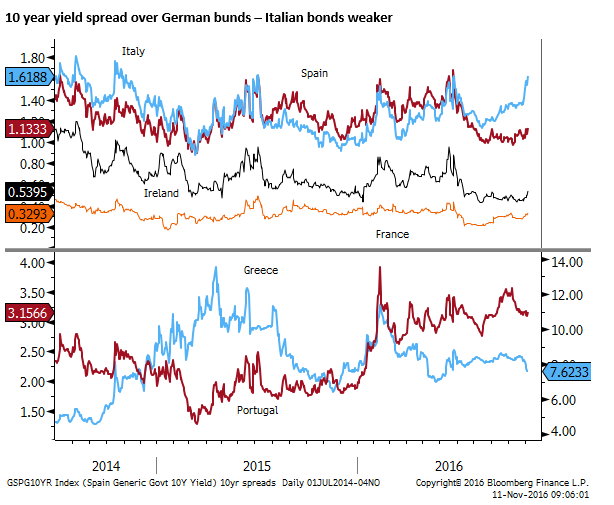

Rising fear of anti-establishment political movements has weakened Italian bonds and the EUR ahead of the 4 December Italian election and national elections next year in several key Eurozone countries, while the GBP has recovered lost ground as the impact of Brexit seems less of a special case.

His support for winding back Dodd-Frank regulations on US banks, and the steeper yield curve has lifted financial sector equities sharply, while his anti-trade rhetoric has undermined Asian equities and multinational info-tech company share prices in the USA.

Industrial metals prices have shot-up in hopes of more infrastructure spending, helping lift material equities, but energy prices are weaker, in part because Trump is a climate change denier that supports the further development of the US fossil fuels sector.

Where does the Rubber meet the road?

Global financial markets have responded quite sharply in anticipation of his policy ideas, of which there are many that may shake up the status-quo, even though these will take months and even years to be implemented, and in what form, there is great uncertainty.

However a key element is that despite the narrow victory by Trump, where in fact he lost the popular vote but won the Electoral College vote, Republicans control both houses of Congress, so Trump will have the rare power to actually implement policies, suggesting that he can indeed shake up the status quo.

It is positive for global investor confidence that he has been much more controlled, including reaching out to mend fences with Paul Ryan, the Republican Speaker of the House of Representatives, and expressing respect for President Obama and the Clintons. However, we are yet to find out how he will handle the inevitable pressure to deliver on his policy promises, most of which are very loosely defined and will require very delicate and detailed negotiations. There will be considerable attention to the administration personnel choices he makes as these will be influential on how policies may evolve.

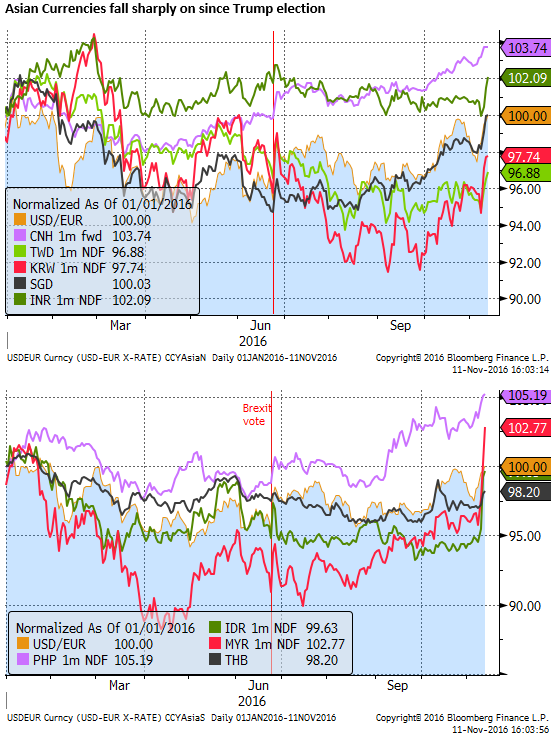

Asian currencies hit the skids

The broad Trump message is anti-trade and anti-globalization, bring back manufacturing jobs to the USA. This has contributed to a significant fall in Asian currencies. The media is asking – will Trump label China a currency manipulator, or slap a 45% tariff on Chinese imports, some of the claims he made during the campaign. While Trump has not revisited these issues as President-elect, presumably he will be pressured to do so at some point.

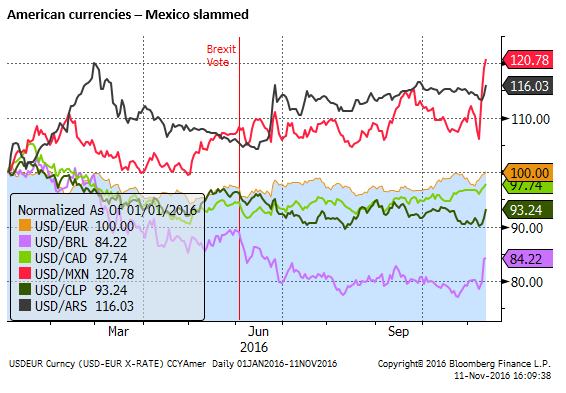

The Mexican peso has fallen more sharply than most on Trump promises that he will build a wall on the Mexican border, and somehow make Mexico pay for it, and claims that NAFTA is a bad trade deal that needs renegotiating and crack down on illegal immigration from Mexico. The US accounts for 80% of Mexico’s exports.

However, one may wonder if the fall in MXN has gone far enough as the realities of messing with NAFTA and the downside of routing out a long tradition of hard working productive immigrants while stoking social unrest lead to an inevitable softening of the hardline campaign message.

The flipside of pursuing tougher trade policy is that the US may end up being left out of trade deals. US companies are trying to make inroads to the Indian economy. And by turning up the heat on China and dealing out of the Trans-Pacific Partnership agreement, the US risks pushing much of Asia into the arms of China and being frozen out of developing world trade pacts. These political realities are likely to force Trump into a more conciliatory tone.

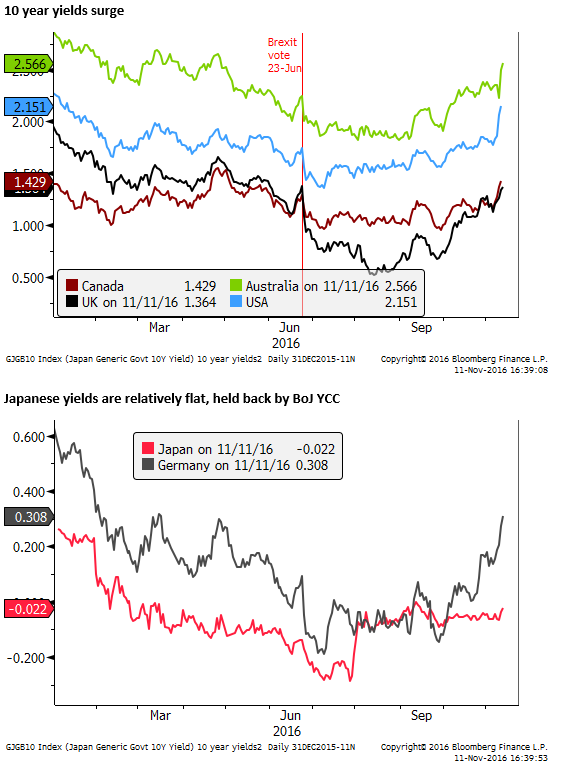

Yield Surge has wide-reaching effects

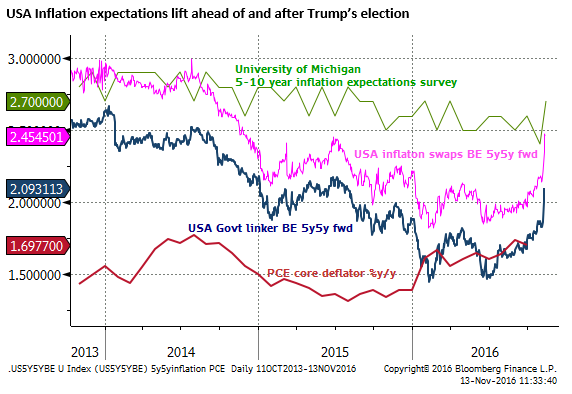

One of the most significant global market developments is a surge in global bond yields. The surge in yields may reflect some pent-up pressure that has been let lose by broader emotional and global market upheaval in the wake of the Trump election. His pro-growth, big infrastructure spending and tax cut promise have provided the rationale for a jump in USA yields.

Yields were already tending to rise for a variety of reasons over recent months – the ECB and BoJ exhibited reluctance to further expand QE policies and have acknowledged costs of negative rates and flat yield curves, industrial commodity prices have generally strengthened this year as Chinese demand has increased, Chinese production of coal and iron ore has been cut, global growth indicators have generally improved since mid-year, and a number of countries have turned towards more fiscal spending to help support growth. Furthermore, headline inflation readings in many parts of the world have been improving since Q2, albeit from low levels, and market-based inflation expectations have been rising in recent months. As such, the Trump election lit a fire under an existing trend.

However, it will not be all smooth sailing towards more fiscal expansion even with full control of Congress, Trump also railed against excessive government debt during the campaign. He implied he could promote infrastructure spending and tax cuts without expanding the deficit by cutting wasteful spending and growing the economy faster. Funding infrastructure spending will be a thorny issue and one he will need to negotiate with many in his own party that are against higher government deficits. It appears that he is hoping for considerable private sector funding to support infrastructure spending. This may be easier said than done. The market is hoping that Trump sees infrastructure spending as a priority and will find a way to make it happen.

The WSJ reported on Saturday that a trend towards more USA infrastructure spending is already developing, and the election has given it a further boost. It said, “State and local governments around the U.S. have issued $149 billion in bonds for new infrastructure projects thus far this year, putting 2016 municipal borrowing on track to surpass each of the past five years, according to Thomson Reuters data.” Much of the borrowing happened in Q2 and Q3. It reported that on Election Day, voters approved another $55.7bn in state and local elections for issuing bonds for new infrastructure spending. (As Donald Trump Plans Building Boom, Cities and States Rush to Borrow – WSJ.com)

The rise in USA yields, spreading to global yields, has had wider implications for high yielding commodity and emerging market currencies and their bond markets. It has generated a significant correction in the so-called ‘search for yield’, so a number of formally strong higher yielding currencies have recently fallen more sharply against the USD. This includes plunges in BRL and ZAR despite stronger coal and metals prices that might support these currencies. The AUD and NZD have also been relatively weak, despite their stronger commodity prices.

Equity markets caught in the cross-fire

The equity market response has been varied. Some but not all emerging market equities have weakened. Latam equities have been weak, led by Mexican equities, reflecting Trump threats to trade and immigration. Asian equities have also tended to be weaker, reflecting the importance of trade in the region directly and indirectly to the USA. However, Emerging European equities have strengthened, led by Russia, on hopes that a Trump led USA will help mend political relations with Russia, perhaps easing trade and finance restrictions.

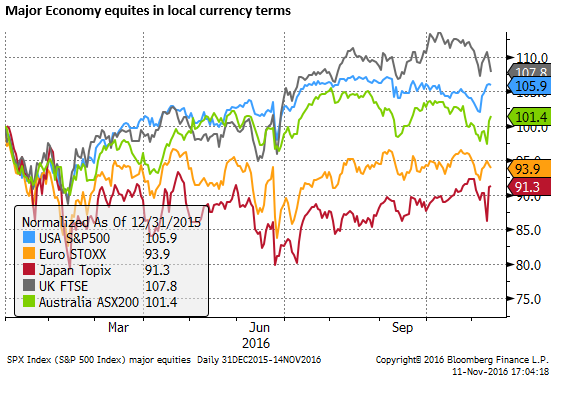

Major economy equity indices are generally stronger since the Trump election. In the case of Japan this, to a large extent, reflects the sharp fall in the JPY. GBP, in contrast, has been stronger, dampening the UK equity market. Broadly speaking, equities are still little changed in recent months.

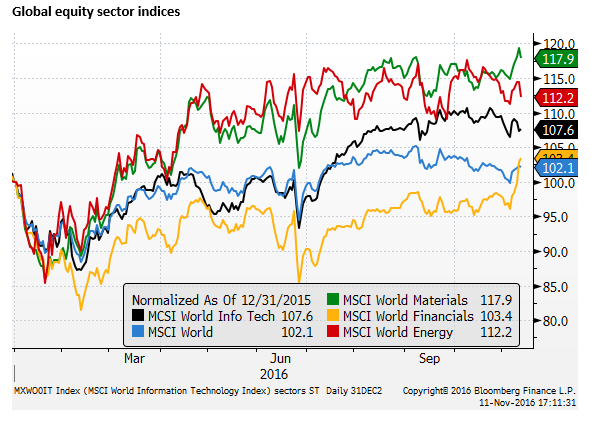

There has been considerable sectoral diversion in the equity market. The big winner has been financial sector equities. This reflects the sharp rise in yields and yield curve steepening that has improved the profitability outlook for banks.

Furthermore, US bank equities have benefited from a Trump policy to revamp Dodd-Frank and ease restrictions on banks. There is speculation that Trump will name Jeb Hensarling as Treasury Secretary. Hensarling has pursued rolling back Dodd-Frank from his position in the House Financial Services Commission. (Trump Team Considering Rep. Jeb Hensarling as Treasury Secretary – WSJ.com). Trump has employed Paul Atkins on his transition team to advise on financial regulation policy. Atkins is seen as favoring less regulation. (Donald Trump’s Point Man on Financial Regulation: A Former Regulator Who Favors a Light Touch – WSJ.com)

Global material equities have also lifted been lifted by the prospect of more infrastructure spending. However, info tech shares have lagged recently, fearing interference to global trade from Trumps anti-trade rhetoric.

Anti-establishment fears in Europe

The anti-establishment trend in global politics has become a bigger influence on financial markets with the Trump victory building on the Brexit vote and leaving investors with a heightened fear that the Italian PM Renzi will fail in his attempt to consolidate power with a referendum on constitutional reform set for 4 December. The reform proposed by Renzi is designed to make it easier for his government to pass legislation by reducing the power of the Senate, and he has threatened to resign if it fails to pass. Anti-EU populist parties oppose the reform. Looking ahead the market is also seeing risks to cohesion in the Eurozone from elections in Germany, France, and the Netherlands next year.

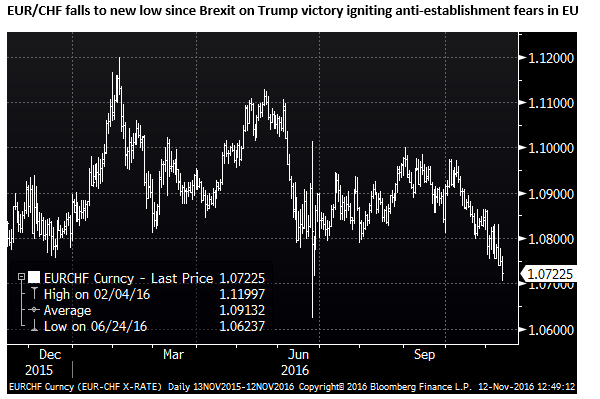

Such considerations may be weighing on the EUR. Although it is difficult as always to disentangle how the EUR should trade in these circumstances. Does the value of the EUR look harder or softer? Does it respond positively of negative to homegrown risks? Certainly, EUR/CHF has weakened.

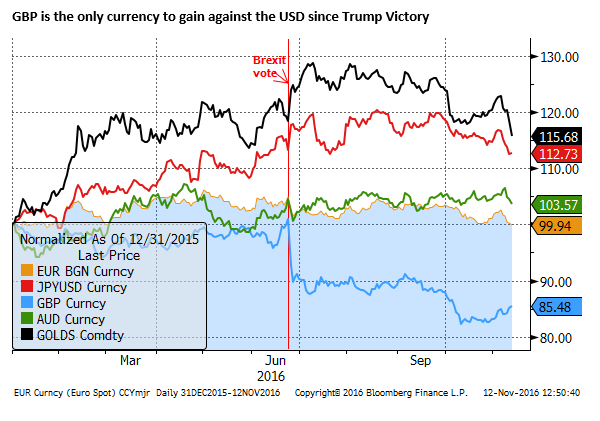

On the other hand, with anti-establishment forces appearing more widespread, the retreat from the EU by Britain no longer appears such a special case; trade deals globally appear under threat as more Western developed countries turn away from globalization. As such, the GBP has recovered some of its lost ground in recent weeks. Since the Trump victory, it is the only currency to gain against the USD.

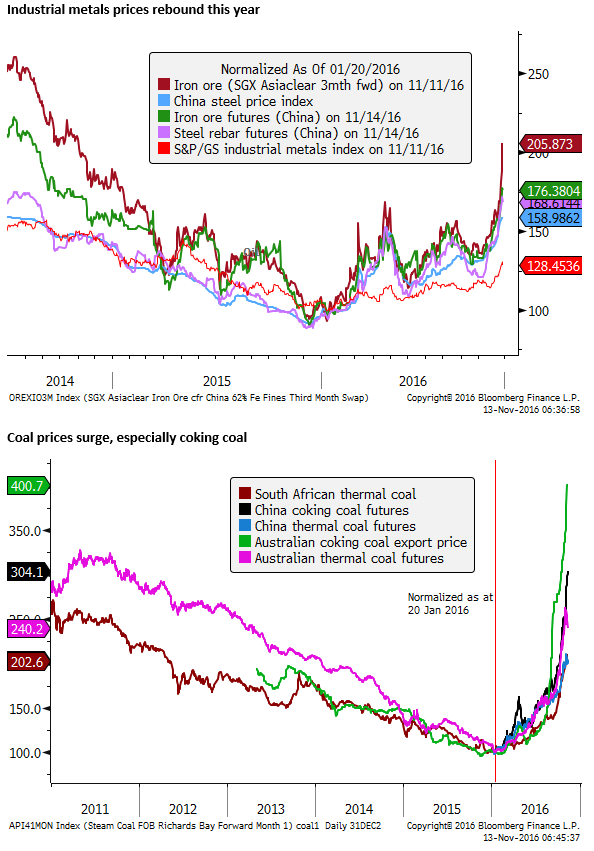

Commodities – industrial metals surge, precious and oil weaker

Gold has fallen sharply towards pre-Brexit vote lows. The sharp rise in bond yields reduces the appeal of low-yielding gold as an alternative store of value. The broad strength in the USD has also weighed on Gold.

Other commodity prices are exhibiting a range of factors. Developments in China include production cuts for iron ore and coal this year to consolidate inefficient over-capacity and address pollution, a recovery in demand led by ongoing rapid infrastructure spending and a recovery in the property market, and easy liquidity conditions that appear to be contributing to excessive speculation on commodity futures exchanges. As a result coal and iron ore have seen remarkable rebounds this year.

Coking coal export price from Australia, used in steel-making, has surged by around 300% this year to return to boom-time highs. Thermal coal, used in electricity generation, has reversed three years of losses to highs since 2012.

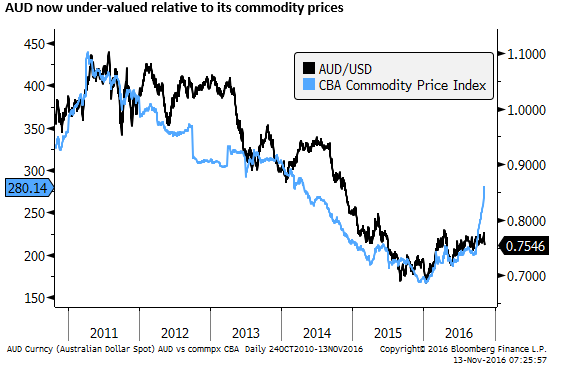

The price of iron ore has doubled this year from its lows to a two-year high. On the back of these two major export markets for Australia, coal and iron ore, the country’s terms of trade has rebounded much more quickly and significantly than the RBA had forecast, and they are beginning to see more of these gains as persisting. It is quite possible that the Australian external trade balance returns quickly to a surplus, providing support for the AUD that now appears significantly below levels consistent with commodity prices. However, Australia’s third largest export market that is set to expand rapidly as new production comes on stream, gas, is experiencing price falls.

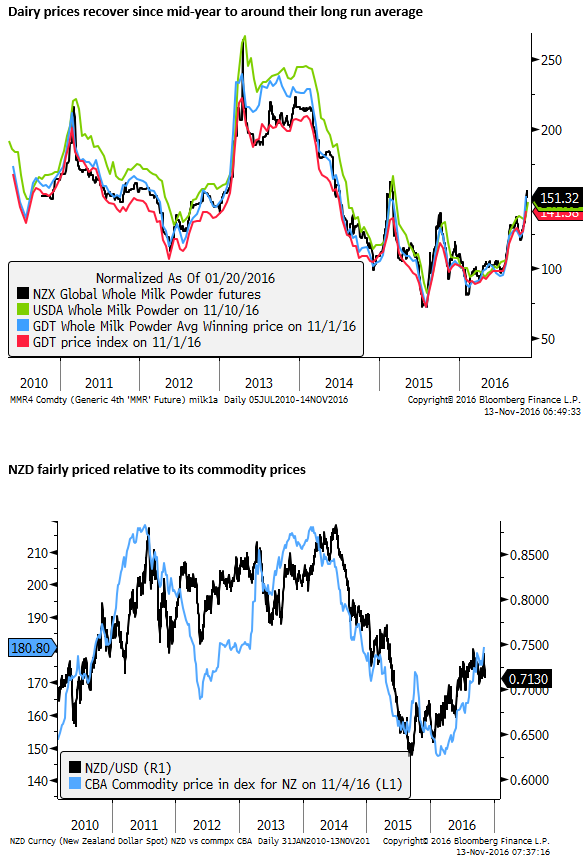

Dairy prices have also recovered since mid-2016 to around their long-run average levels after two years of significantly below average prices. It also appears that a more sustained balance has returned to this market. The NZD appears fairly priced with respect to its commodity prices over the medium term.

The Trump election may have provided some more positive impetus to steel prices and steel-making commodities (iron ore and coking coal). Even though the anti-trade rhetoric may limit the prospects for Chinese steel exports, if overall more steel is required, the price of these commodities should rise.

Hopes for more infrastructure spending also sent other base metals sharply higher, including copper and aluminum. However, copper futures spiked on Friday before closing lower, a sign that the initial Trump euphoria may have peaked.

While industrial metals prices have surged, energy prices have resumed their recent decline over the last month to be at the lower end of their range since mid-year.

Oil prices are the most important for global inflation, and the recent fall places some doubt that the market has stabilized from its over two-decade lows seen early this year. The recovery in oil prices since the beginning of the year has helped to lift from low levels inflation expectations, but there still appears to be significant excess supply that might keep prices capped for the foreseeable future.

The immediate focus is on the 30 November OPEC meeting where its members are supposed to ratify an agreement to cap production. There is considerable doubt that a deal will be reached or be adhered to.

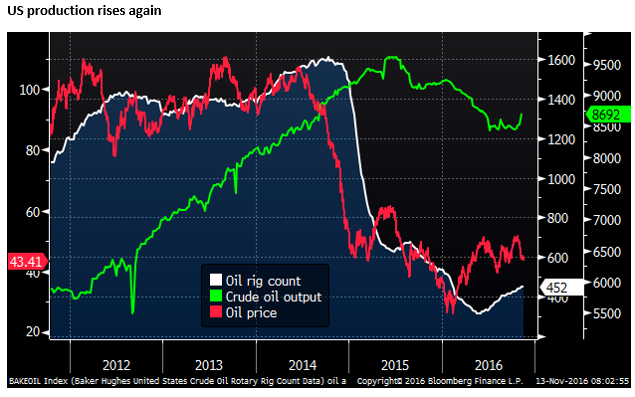

The USA has been a big swing factor over recent years contributing to the rise in production and collapse in prices since 2014. The fall in US production was a factor helping prices recover this year. However, its production has increased in the last month, responding to a lift in oil rigs in operation since a low in May.

The Trump election may also have contributed to weaker energy prices. He is a climate denier and has campaigned to remove restrictions on energy exploration, production, and exports. On the other hand, his pro-energy sector policies have helped underpin US energy sector company share prices.

Nevertheless weaker energy prices may act as a counter-weight on the recent surge in global yields that have had significant broader implications for currency markets.