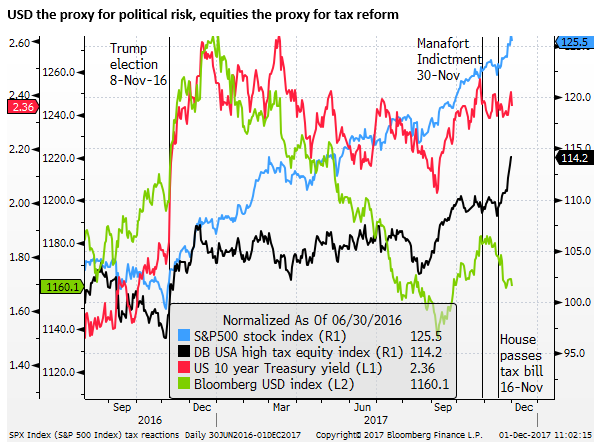

USD: political risk proxy / US stocks: tax reform proxy

There has been a wide divergence between the performance of US equities and the USD in the last year, accelerating in the last month. The USD also has underperformed US rates and yields. It appears that equities have responded positively to the faster pace of progress on tax reform, while the USD has responded more to political uncertainty related to the Mueller investigation and the provocative style of president Trump. We have been surprised at times this year that the USD has remained so weak. The competing factors of tax reform progress and Flynn’s plea deal pull the USD in different directions. However, if the pattern this year that has intensified in the last month persists, the USD may continue to slide despite tax reform. Rolling medium-term political uncertainty has weighed on the USD so far this year. It may continue and intensify in the next year, dragging down the USD, or at least dampen its positive response to stronger economic confidence and rate hikes if tax reform helps sustain and boost the pace of US growth.

USD has been the proxy for political risk

US markets have been buffeted on Friday by competing stories, one positive for US assets (the tax bill’s likely passage through the Senate) and one negative (former National Security Advisor Flynn’s charges and plea deal).

This is making it very difficult to trade the USD. In fact, it does appear that these competing stories of tax reform vs. the Mueller investigation have been buffeting the USD for much of the year.

One observation is that, throughout the year, the USD appears to have been more influenced by the political uncertainty generated by the Mueller investigation and Trump’s highly provocative style of Presidency, than by progress on tax reform.

If we look at the chart below, we see that the US equity market, and even the bond market, to a lesser extent, have tended to take more confidence out of tax reform prospects and the sustained strength in the US economy, while the USD has struggled through much of the year.

If we look at the last month, a period where tax reform progress has been rapid, we see a significant divergence between the USD from US equities and bond yields.

It is noteworthy that the USD was struggling even before the Flynn revelations on Friday. On Thursday, the USD appeared to dip in response to a barrage of Trump tweets criticizing the New York Times and CNN, and calling for investigations into the Clintons. Many people commented in the chain from these tweets that the timing of Trump’s tweets might indicate that there was bad news about to be released related to the Mueller investigation and Trump was trying to get out in front of it. These thoughts may have been prescient.

In general, the lack of positive reaction in the USD to rapid tax reform progress over the last month appears to reflect fear in the market that the Mueller investigation was taking shape since the indictment of Manafort and charges against Papadopolous on 30 October.

If this pattern continues, the USD may continue to weaken, or at least struggle to rise, even if the tax reform bill continues to move forward to completion.

The more significant response in the USD to political uncertainty, to be fair, may also relate to stronger economic growth abroad. We and others have argued that the weaker USD this year suggests that the FX market is paying more attention to equity-related capital flows than relative interest rates.

There is no clear answer to what are the most important drivers of the USD this year. However, it does appear that the heightened, rolling, and recently accelerated political uncertainty related to the Meuller investigation, has helped the market pay less attention to rising US rates and tax reform progress, and more attention to stronger growth fundamentals abroad.

US bond market reluctant to price in tax reform

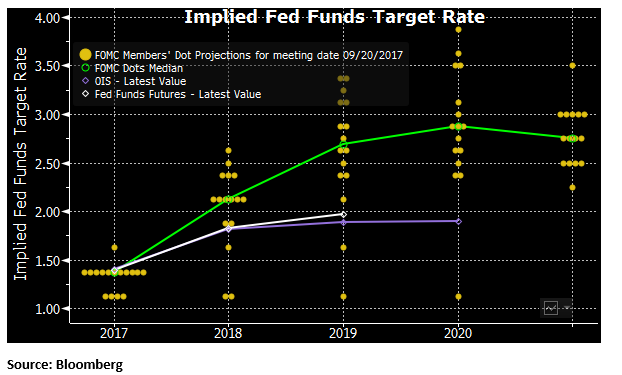

The Fed is still projecting four hikes by end 2018; the market is pricing in only around two and a half hikes. And Fed FOMC members have said that these projections do not include any expectation that tax reform will be passed.

Our impression from following the financial press is that many bank economists have raised their rate forecasts for next year, based on stronger US economic data, a tightening labor market, and the increasing probability of rate hikes. Most are in line with the Fed projections.

It is surprising, therefore, that US bond yields have not risen more than they have in the last month. The significant flattening in the USA yield curve has bemused many investors. Rate expectations are rising, but they still sit well below the Fed’s projections. As such, the entire yield curve might be regarded as slow to rise in response to economic indicators and tax reform progress; particularly longer-term yields.

It may be the case that bond yields are also building in some political risk in the USA.

Equities build in tax reform

The US equity market, on the other hand, has continued to rise strongly, in line with global equity markets. The global nature of the equity rally may help account for the lower reaction of US equities to political uncertainty. Nevertheless, it does appear that high tax equities. which have the most to benefit from tax reform, have moved up significantly in the last month as tax reform progress has been more rapid.

Judging by commentators in the financial press, most equity analysts believe that US equities have strengthened this year, in part at least, due to the expectation that tax reform will be passed sooner or later.

The evidence suggests that US equities have been more influenced by progress in Congress towards tax reform, bond yields are caught somewhere in the middle, and the USD appears less reactive to tax reform progress and more reactive to political uncertainty related to Trump and the Mueller investigation.

What happens next

Looking at the developments on Friday, we cannot be sure which factor will drive the USD. The Senate passage of its version of a tax bill should support the USD, while the Flynn story should weaken the USD. The USD performance so far this year leads you to think that it may respond more to the Flynn news and resume a weaker trend. But much may depend on what happens next.

Republicans in the House and Senate will still need to agree to the same tax bill. They will be aiming to do this by year-end. There are distractions that may delay progress including the need for a new Continuing Resolution to allow government spending beyond 8 December. Debate on this issue may bring into the mix contentious Trump policies on immigration, DACA and border wall funding. There is a risk of a shut-down in government departments in December.

How Trump and members of Congress respond to the Flynn revelations may also be a distraction to the passage of a Continuing Resolution and tax reform. While the probability of tax reform by year-end or early next year appears to have increased significantly, there are still hurdles and distractions that may impact on financial markets expectations.

We do not yet know what Flynn has said to the Mueller investigation, and where it goes next. Flynn is reported by ABC news to be “prepared to testify that Donald Trump directed him to make contact with the Russians, initially as a way to work together to fight ISIS in Syria.” (Flynn has promised special counsel ‘full cooperation’ in Russia probe: Source – ABCnews.go.com).

This raises many questions. It might a smoking gun, but is not yet clear evidence of collusion between the Trump administration and the Russian government related to manipulating the election. It may imply that Trump and his team have violated the Logan Act (undermining the policies of the sitting government as a private citizen). Or it may be part of a case that Mueller is attempting to build against Trump arguing that he attempted to obstruct justice in the firing of former FBI director Comey.

At the very least, this investigation is likely to be a cloud that continues to hang over the stability of the US administration. In the past, Trump has responded to this pressure by firing up his Alt-Right base claiming that the investigation is a witch-hunt orchestrated by the Washington elite, and that the Clintons and Democrats need to be investigated.

Over his first year as president., Trump has also attempted to distract the electorate and the media by tweeting about a range of policies that appeal to the Alt-Right. During these episodes, the USD has weakened, perhaps because it appeared that the administration would lose focus on more economic relevant policies such as tax reform and infrastructure spending.

Perhaps now that Congress has got ‘the bit between its teeth’ chasing down tax reform, the market will worry less if Trump loses focus on tax reform. But the market must also now start to worry more that the Mueller investigation will influence the results of the mid-term elections in November next year. It may help Democrats gain seats and increase the risk of impeachment proceedings into 2019.

Rolling medium-term political uncertainty has weighed on the USD so far this year. It may continue and intensify in the next year, dragging down the USD, or at least dampen its positive response to stronger economic confidence and rate hikes if tax reform helps sustain and boost the pace of US growth.