Warning signs for EUR and JPY, EM rally mature, gold may be poised for renewed strength

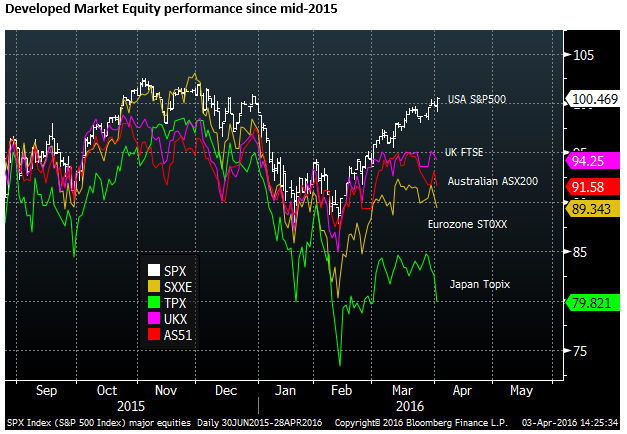

The recent rebound in global assets has been driven by emerging market and USA assets, while other developed markets, particularly Japanese and Eurozone assets have lagged behind and indeed their bank stocks have sagged. The rise in US assets is supported by resilience in US economic data, a dovish turn by the Fed and a weaker USD. Stronger EM assets have been supported by a recovery in oil and other commodity prices, policy easing by China, Europe, and Japan, a dovish Fed, and improved outlook for Chinese growth, currency and asset markets. Weaker growth indicators in Japan, weaker inflation expectations in Europe, weaker bank equites, and overall sluggish equity performances suggest policymakers will work hard to prevent further strength in EUR and JPY. It is hard to get behind the further rally in these currencies. If risk aversion returns they may rise, but even then these gains are likely to be limited and gold should be favored as the alternative safe haven. The outlook for EM assets is now more balanced after investors have piled back in over the last month. The recent down-turn in oil prices may return as a dampening influence on EM assets and currencies. Investors may also start to consider the Fed coming back into play by mid-year.

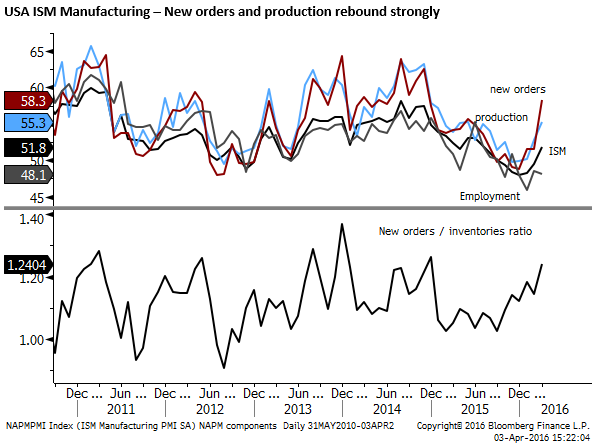

USA assets and economic performance pulling away from other developed markets

The accepted wisdom is that the Fed has taken a dovish turn and it is hunting season for riskier assets and the USD now in a falling trend.

The problem with the new theme is that the US data is looking perkier with a hint of wage growth, while other developed market assets; those in Europe, Japan, UK and Australia, for example, are sagging.

The evidence suggests that investors are getting a put-off by the strong currencies in many developed countries, including Japan, the Eurozone and Australia.

The US stock market and corporate bonds, on the other hand, have performed much better recently than other developed markets. US equities shook-off the weak lead from Europe and Japan on Friday to post a new high for 2016, on the first day of the second quarter, when investors start to throw-off the shackles of performance reporting.

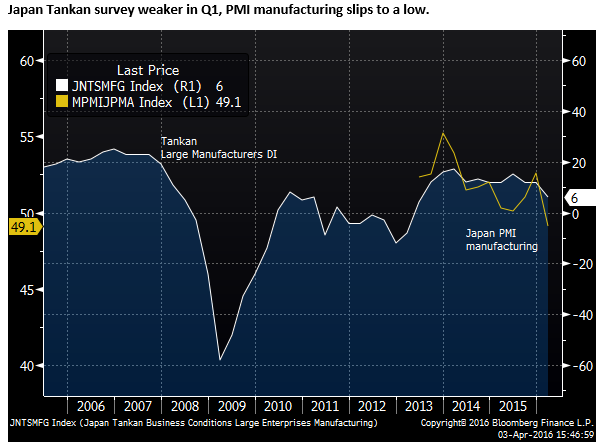

Economic data in Japan is also looking gloomy and it all points to the BoJ steering off-course in getting to its 2% inflation target. Fiscal policy tweaks may help, but it appears that more BoJ policy action is required, which may mean even more negative Japanese yields. Policymakers would be advised to not let the JPY continue to strengthen. (Japan Needs Economic Boost Later This Year, LDP’s Komura Says – Bloomberg.com).

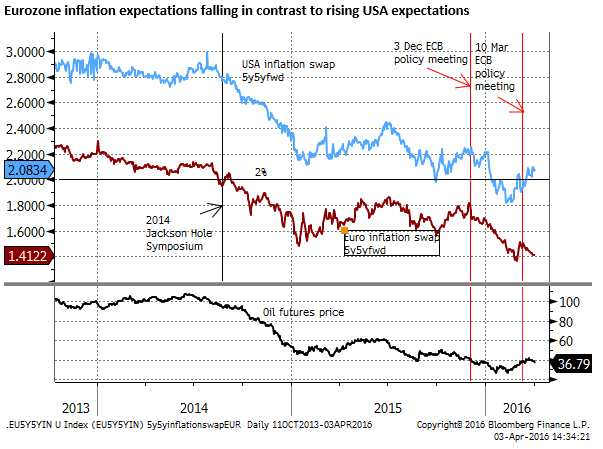

In Europe, the recent economic data has not been bad and there may be more hope that policy measures employed can get the economy back on the path to its 2% inflation target. Core inflation rose back to 1.0%y/y in March (up from 0.8% in Feb and above 0.9% expected), the PMI data firmed in March and remain modestly in growth territory above 50.

However, in contrast to the US where market-based measures of inflation expectations have been firming, they have sunk back to the lows in the Eurozone. The ECB will hardly think their job is done and will not be pleased with further appreciation of the EUR.

Bank share prices pose global risks, but more so in Eurozone and Japan

The performance of bank share prices generally is posing a risk to the more buoyant global mood, but their particularly weak performance in the Eurozone and Japan, indicative of the pressures of negative interest rates, is more worrisome to the authorities in those nations.

On one hand it points to problem associated with negative rates, and makes it harder for these central banks to cut further. On the other hand it also increases pressure on the central banks to ease policy further, putting them in a catch-22.

Pertinently for currency markets this makes it more important that the other channels through which negative rates can boost growth and inflation are working effectively, and this includes weakening exchange rates.

For instance in Japan’s case where the government has made some moves to front-load fiscal spending and lay the groundwork for additional stimulus and the BoJ has already cut rates recently, it becomes more essential that they now turn their attention to at least preventing further strength in the JPY, if not encourage it to reverse course.

Bank equites in Australia are also performing poorly (the chart above shows an equal weighted index of the big four). As a major chunk of the Australian stock market, favored by many domestic investors for the stable relatively high dividends, their laggard performance is a restraint on the outlook for the Australian economy and in turn rates and the AUD.

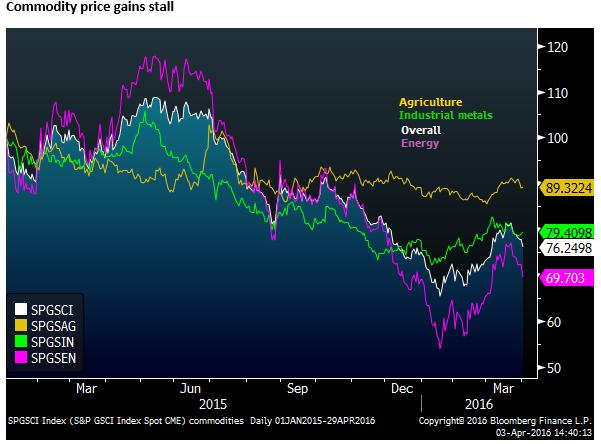

Commodity price recovery stalls, more so for oil

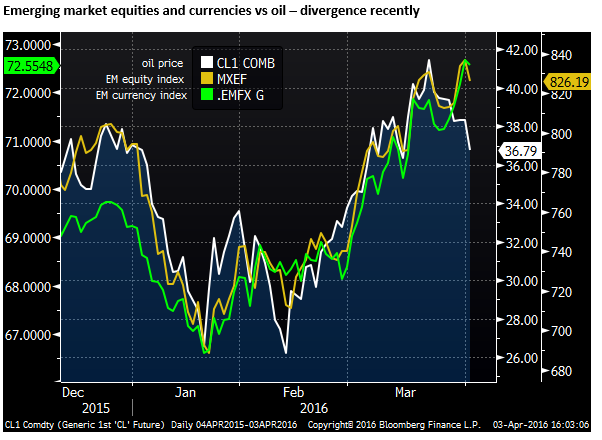

The rebound in commodity prices that has provided a comforting companion to the rebound in emerging market assets and commodity currencies against the USD have also stalled recently. Oil prices in particular look shaky.

In the last week or so global risk assets, equities, and EM and commodity currencies have shaken off their tight correlation with oil prices most apparent around the turn into 2016. However, should oil prices continue to retreat they might yet drag on global investor confidence.

The good vibes running up to the 17 April Doha meeting of oil producers appears to be fading. Saudi Arabia has thrown some cold-water on expectations, claiming they will only freeze production if Iran complies, at the same time discussing increasing its own production by re-opening a field it owns jointly with Kuwait.

Hedge funds are reported to have established a large net long position in oil at a time when the price action and recent news is less encouraging. As such, we may be on the cusp of a period of weaker oil prices sufficient to infect broader global investor confidence again. Perhaps not enough to return the markets to their severe panic early in the year, but sufficient to take the steam out of the recent rebound in EM equities.

Hedge funds bet on higher oil prices – FT.com

Global investors are no longer very underweight EM assets, rebound is mature

The Institute of International Finance (IIF) capital flow monitor, backed up by the EPFR Global flow data, illustrate that global investors have piled back into EM equities and bonds over the last month.

Emerging market portfolio flows hit 21-month high – FT.com

As such they are no longer clearly underweight this sector, suggesting risks are at least more evenly balanced, opening the door to renewed weakness.

The technical (chart) picture would also suggest risks are returning to the downside for many global asset markets after two months of rebound and downtrend resistances now in view; investors may be less inclined to continue their buying spree.

It may be premature to call time on the global equity market rebound, but it is looking mature. It is evident that it has been led by EM and USA markets. The former reflecting a rush back in by under-weight investors on a confluence of supporting factors (policy easing in China, Europe, Japan and a more dovish Fed, more stable Chinese assets and currency and higher oil prices). The later on a more dovish Fed, ongoing USA recovery in the face of global risks, and a weaker USD.

What is standing out is the lack of go-forward in other key developed markets, and this reflects weak bank equities, stronger currencies (notwithstanding negative rates), weaker economic trends in Japan, ongoing legacy problems with debt and structural rigidities. In the case of the UK Brexit fears are dominating.

Perhaps the market will continue to take confidence from a Fed holding rates steady for the time being, prepared to look through evidence of ongoing recovery and some renewed signs of inflation pressures, and this will spill over to still firmer emerging market assets and currencies. However, renewed weakness in oil prices may also return as a factor capping their recent strength. The market may also start to see the Fed coming back into play around mid-year if US data remain buoyant.

Developed markets, in particular Japan and the Eurozone, are flashing clearer warnings that may soon detract from their currency performance.

But if globally assets start to stall and risk appetite ebbs, the JPY and EUR could find support as the risk haven currencies.

There are, as is often the case, competing influences that make it difficult to act with confidence in any assets or currency trades. But overall, it appears the potential for further gains in JPY and EUR are limited as safe-haven demand for these currencies will be questioned when they increasingly appear to the primary source of risks.

Gold may soon resume a rising trend

As such, we continue to look on gold as a potential long trade. It has struggled recently stalling even as the USD has faded. As such, gold has dropped back significantly against the EUR, JPY, AUD and EM currencies. We can see a case for it soon resuming its rally as an alternative store of value if global equities begin to stall and EUR and JPY fail to make much headway.

Fed Minutes, U.S. Services, Masters Golf: Week Ahead April 4-9 – Bloomberg.com

Australian Week Ahead by Commsec economist – businessspectator.com.au