Trading and comments in AUD/NZD from 20 July to 4 August.

The section covers the trading in AUD/NZD from 20 July to 4 August. The notes are in order from latest to oldest, so you may wish to review from the bottom up for chronological order.

It includes comments on RBA Deputy Governor Debelle (dovish), NZ Finance Minister (hawkish); Australian CPI data, RBA Governor Lowe’s Labour speech; RBA 1 August policy statement – Australia no longer in transition; NZ Q2 Labour Data, Australian PMI, NZ job ads.

Real Time AmpGFX – AUD/NZD comment; Wed 8/2/2017 7:51 PM; Fri 8/4/2017 6:31 PM MST

Australia services PMI rose to 56.4 in July. 3mth average at 54.2, high since Jan of 54.4. Australian economic indicators continue to print relatively strongly.

The trade balance was weaker than expected. Although it remains in surplus, and might be expected to rise next month in light of resurgent commodity prices.

NZ job ads were a bit softer, consistent with labour market in NZ losing moment this year.

Australian retail sales and RBA policy statement tomorrow. We should have a good idea what is in the statement after the policy statement on Tuesday. But the tone of the statement may be more upbeat in light of data improvement and tone of July minutes.

https://ampgfxcapital.com/reports/construction-commodities-and-politics-build-case-for-audnzd/

Positions

Long half unit EUR/NZD at 1.5680; s/l 1.5873; t/p 1.6500

Long 1.5 units AUD/NZD at 1.0711; s/l 1.0647; t/p 1.1223

Real Time AmpGFX – bought AUD/NZD to add to position; Wed 8/2/2017 7:35 PM MST

Bought half unit of AUD/NZD at 1.0718

Positions

Long half unit EUR/NZD at 1.5680; s/l 1.5873; t/p 1.6500

Long 1.5 units AUD/NZD at 1.0711; s/l 1.0647; t/p 1.1223

Real Time AmpGFX – NZ labour data not all bad; s/l orders raised; Tue 8/1/2017 5:23 PM MST

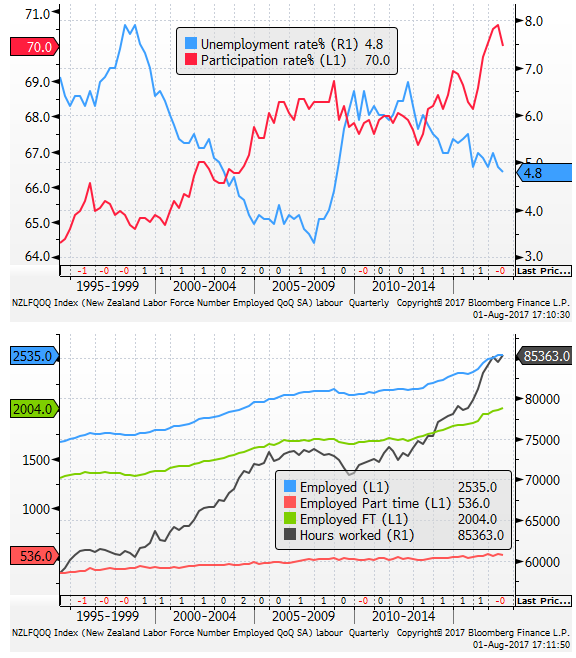

New Zealand employment growth in the quarter was significantly weaker than expected, falling 0.2%q/q, but still up 3.1%y/y (below 4.1% expected).

The unemployment rate was down from 4.9% to 4.8%, as expected, reflecting a sizable fall in participation.

However, the mix in the data was better, with full-time up 0.7%, part-time down 1.8%, and hours worked up 1.0%.

Private sector wage growth was as expected, although public sector wage growth is firming from a year ago levels, reflecting bigger quarterly gains in Q4/Q1.

The data are not all that bad, considering the mix, and rise in hours worked. The wages growth data are as expected, still subdued overall.

I added to the AUD/NZD position in part due to the recent resurgence in Australian commodity prices, the broader evidence that activity and housing market in NZ is slowing, whereas both are resilient in Australia, the political risk in NZ, and the relative current account performance.

Positions

Long half unit EUR/NZD at 1.5680; s/l 1.5787; t/p 1.6500 (s/l raised)

Long one unit AUD/NZD at 1.0707; s/l 1.0647; t/p 1.1223 (half unit trades consolidated, s/l raised)

Real Time AmpGFX – bought to add to AUD/NZD; Tue 8/1/2017 4:48 PM MST

I bought half unit at 1.0719

Positions

Long half unit EUR/NZD at 1.5680; s/l 1.5737; t/p 1.6500

Long half unit AUD/NZD at 1.0695; s/l 1.0633; t/p 1.1223

Long half unit AUD/NZD at 1.0719

Real Time AmpGFX – Australian economy no longer in transition; Mon 7/31/2017 11:50 PM MST

The AUD is traveling quite solidly after the RBA statement. It does appear that the RBA has changed up its comment on the exchange rate to attempt to talk the exchange rate down. But this has had little impact.

Rates steady, labour market slack and low wages growth

Otherwise, the statement suggests that the outlook for the economy has changed little since the May Statement on Monetary Policy. The RBA appears to be suggesting that rates are likely to remain steady for some time.

The key here is forecasting slack in the labour market and low wage growth. It said, “The unemployment rate is expected to decline a little over the next couple of years. Against this, however, wage growth remains low and this is likely to continue for a while yet.”

Lowe’s speech on the labour market last week sets out the details here – unemployment is around ½% above neutral, and there is under-employment (people that want to work more hours).

The views on the housing market remain little changed, and we know from Lowe’s speech last week that he is patiently waiting for further slowing house price growth.

GDP forecast little changed

The outlook for GDP growth is little changed since the May policy forecast round. The statement said, “The Bank’s forecasts for the Australian economy are largely unchanged. Over the next couple of years, the central forecast is for the economy to grow at an annual rate of around 3 per cent.”

Inflation higher near term, same medium term

The RBA appears to have raised its forecast for inflation over the next year. It said, “Higher prices for electricity and tobacco are expected to boost CPI inflation.” However, the RBA added a new medium term factor that may hold down inflation (The Amazon effect). It said, “A factor working in the other direction is increased competition from new entrants in the retail industry.” The RBA repeated its broad assessment that, “Inflation is expected to pick up gradually as the economy strengthens.” This suggests that the inflation forecasts for 2 to 3 years out will also be unchanged; basically in the target zone in 2019.

Commodity prices higher, forecast to fall

It acknowledges that “Commodity prices have generally risen”, but downplays this by predicting that “Australia’s terms of trade are still expected to decline over the period ahead.”

Little guidance

The RBA retained its final statement that offers little guidance. It said, “the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.”

The RBA could have emphasized its neutral stance by adding some guidance that policy is likely to be steady for some time. It has done this in the past, but not since Lowe has been Governor. He seems to prefer the flexibility to act if conditions change.

Exchange Rate – Economics 101

The comment on the exchange rate has removed the line about appreciation complicating adjustment. Perhaps the RBA is no longer viewing the economy in transition. The mining investment boom/bust is largely over, and the economy is moving beyond this so-called adjustment.

On the basis of current forecasts, the exchange rate comment suggests that an appreciating exchange rate may reignite rate cut expectations if it goes too far. But we know from other statements that the RBA is likely just to remain patient if the AUD rises, and accept a lower glide-path back to medium term target inflation. As such, beyond a knee-jerk reaction, the new comment on the exchange rate may have little lasting downside influence on the AUD.

The statement said, “The Australian dollar has appreciated recently, partly reflecting a lower US dollar. The higher exchange rate is expected to contribute to subdued price pressures in the economy. It is also weighing on the outlook for output and employment. An appreciating exchange rate would be expected to result in a slower pickup in economic activity and inflation than currently forecast.”

Iron ore price surge

We have re-entered a long AUD/NZD position. This reflects the surge in iron ore prices in the last day.

NZ Labour data tomorrow

Our sense is that the New Zealand labour data due tomorrow will tend to be stable or a bit weaker, after its surge in employment growth in the last year, but some moderation in activity indicators in recent quarters. Immigration remains high, so wage growth and unemployment should not show obvious tightening in the labour market.

NZ election looms

The NZ election is coming into focus. The latest polls show a lift in support for NZ First and the Greens, with a dip in support for the ruling Nationals, and the largest opposition party, Labour. As it stands, NZ First is likely to hold the balance of power and will demand some policy changes that will be seen as detrimental to immigration and foreign investment in the housing market. A loss of the outright majority of the Nationals and their closely allied small parties/independents would be seen as raising political uncertainty.

Australian economy showing stronger momentum

Recent economic reports suggest that the Australian economy has gained some momentum, and the market may not be as calm as the RBA may be about higher electricity/tobacco prices and higher commodity prices.

Positions

Long half unit EUR/NZD at 1.5680; s/l 1.5473; t/p 1.6500

Long half unit AUD/NZD at 1.0695; s/l 1.0633; t/p 1.1223

Real time AmpGFX – bought AUD/NZD; Mon 7/31/2017 10:55 PM

I have bought half unit of AUD/NZD at 1.0695

Positions

Long half unit EUR/NZD at 1.5680; 1.5473; t/p 1.6500

Long half unit AUD/NZD at 1.0695

Comment to follow.

Real time AmpGFX – sold to closed AUD/NZD long; Sun 7/30/2017 3:59 PM MST

I sold half unit AUD/NZD at 1.0635

Positions

Long half unit EUR/NZD at 1.5680; 1.5473; t/p 1.6500

Comment.

I can’t be confident that the RBA will not attempt to talk the currency down in its policy statements this week, and/or introduce guidance into their policy statement. As such, I have closed the long AUD/NZD position.

See my preview in the AmpGFX report for further discussion.

Real Time AmpGFX – RBA Lowe speech; Tue 7/25/2017 10:25 PM MST

Overall, Lowe’s speech left an impression that the RBA is quite a distance from considering a rate hike.

Under questioning, he also said a lower exchange rate would be better. And he said he sees a slowing housing market.

Lowe reiterated the message from the Debelle Speech used to dampen any expectation of rate hikes in the foreseeable future. He said,

“Elsewhere in the world, some central banks are now starting to increase interest rates and others are considering when to withdraw some of the monetary stimulus that has been put in place. This has no automatic implications for monetary policy in Australia. These central banks lowered their interest rates to zero and also expanded their balance sheets greatly. We did not go down this route. Just as we did not move in lockstep with other central banks when the monetary stimulus was being delivered, we don’t need to move in lockstep as some of this stimulus is removed.”

Under questioning on the neutral policy rate, he also reiterated the Debelle message, that the market should not have read anything into the discussion in the minutes. That this was just a special topic, in a series of special topics that have and will be presented to the board.

In his speech, he thought wages were unlikely to accelerate much in Australia for some time.

He noted that some other countries are closer than Australia to using up excess slack in the labour market (this might include the USA, UK, and Japan, although he did mention names).

He said it was possible that wages could pick up in these countries, but, “It would seem, though, to have a fairly low probability in Australia, especially in light of the continuing spare capacity in our labour market. The more likely case here is that wage growth picks up gradually as the demand for labour strengthens.”

Under questioning, he further said that liaison with business reveals that wages growth is likely to continue at the same subdued rate for some time.

On the less dovish side, Lowe indicated that the RBA is also concerned about household debt, generating financial stability risks. He said that the RBA is flexible, patient and prepared to live with a longer period of below target inflation, while still aiming for inflation in the 2-3% target over the medium term.

He said:

“Over recent times you would have noticed that we have been paying close attention to the risks in household balance sheets. Household debt is high and rising faster than the unusually slow growth in incomes.

These developments have had a bearing on the setting of monetary policy. We have not sought to stimulate a rapid lift in inflation. The fact that the labour market has been generating sufficient jobs to keep the unemployment rate broadly steady has allowed us to be patient. Our judgement has been that seeking a more rapid pick-up in inflation through yet further monetary stimulus was likely to add to the medium-term risks. Our central scenario remains for underlying inflation to pick up gradually as the economy strengthens.”

Under questioning, about competitiveness, Lowe noted that the RBA has stated that it would be better if the exchange rate were lower to help generate faster growth

Under questioning, he also reiterated Debelle’s comments that the discussion about the neutral rate was not intended to signal anything about policy.

Under questioning on the housing market is said:

It looks like some of the heat is coming out of the Sydney and Melbourne markets. A lot of extra supply is coming onto the market this year, rent growth is weak, there is less foreign demand, the Chinese government has restricted capital outflows, Australia has higher taxes on foreign investment, banks have tightened up lending conditions, and there greater investment in infrastructure that should help lower house prices.

There are quite a number of negative factors mentioned here, it’s any wonder why house prices aren’t tumbling. The take out is that the RBA is not feeling it necessary to hike rates to help control debt growth that is still faster than income growth.

The 2yr swap rates in Australia is down around 2bp after the CPI, and is down around 2bp on the Low speech.

The AUD is so far holding up pretty well to what on balance is a more dovish speech, once we take into account the Q&A section. As such, in the interest of keeping out risk in check, we reduced our position size again; as discussed below.

Real Time AmpGFX – sold half AUD/NZD to reduce position, Lowe speech dovish; Tue 7/25/2017 10:02 PM MST

Sold half unit of AUD/NZD at 1.0640

Position

Long half unit AUD/NZD at 1.0644; 1.0533

Comment to follow.

Real Time AmpGFX – CPI comment and orders; Tue 7/25/2017 8:28 PM MST

The AUD/USD doesn’t normally react much to headline CPI

The underlying were pretty much right on expected.

The annual increase in the more closely watched trimmed mean and weighted median were essentially right on expected, up 0.5%q/q. Both were up 1.8%y/y; in fact the annual increase for the weighted median came out a tick above 1.7% expected.

It is also worth noting that both have been up 0.5%q/q for the last two-quarters. As such they have annualised at 2.0% for the first half of the year, illustrating that while inflation is still below target, underlying measures are now at the low side of the 2 to 3% target range over the last six months, and inflation has picked up since last year.

If the RBA wanted to, they could argue that the emergency rate cuts delivered last year are no longer needed. I don’t expect them to do that, but inflation is up from last year and the economy has regained solid momentum.

Metals and energy commodity prices have increased significantly this week. The Australian resource sector equities are up strongly today, leading a solid rise in the Australian equity market, following a sharp rise of over 5% in the US S&P500 metals and mining sector on Tuesday.

As such we decided to increase our position size to a full unit on this trade.

Next up is Lowe speaking on the Labour market and monetary policy. There is scope for both dovish and hawkish comments here. I suspect that Lowe will sound balanced. The market may be disappointed if he doesn’t make a big deal about the exchange rate. Doing so would be forced, and Lowe seems too intellectually honest to spend much energy trying to talking it down.

Position

Long half unit AUD/NZD at 1.0635; 1.0533

Long half unit AUD/NZD at 1.0644; 1.0533

Real Time AmpGFX – added to AUD/NZD long; Tue 7/25/2017 7:37 PM MST

Bought a second half unit at 1.0644

Position

Long half unit AUD/NZD at 1.0635

Long half unit AUD/NZD at 1.0644

Real Time AmpGFX – bought to re-establish AUD/NZD; Tue 7/25/2017 7:33 PM MST

Bought AUD/NZD at 1.0635

After stop was triggered

The underlying CPI data is as expected, so this data not that bad.

Real Time AmpGFX – raising AUD/NZD s/l; Tue 7/25/2017 3:54 PM MST

Ahead of the Australian CPI report and Lowe speech, which naturally present near term risks for this trade, I have raised s/l

Position

Long AUD/NZD 1.0638; s/l 1.0633

Real Time AmpGFX – bought AUD/NZD; Thu 7/20/2017 9:54 PM MST

Bought half unit AUD/NZD at 1.0638

We have seen a correction on an unusual combination of a dovish speech from an RBA official and a hawkish comment from a NZ finance minister,

There has generated a significant correction in the AUD.

The comments from Debelle were obviously designed to take the heat out of the AUD and speculation of a near term rate hike.

However, I think there is still a case for seeing prospects improving for the Australian economy relative to NZ. And this provides a better entry level to enter a long trade.

Position

Long AUD/NZD half unit at 1.0638; s/l 1.0528