AUD and Australian property facing a perfect storm

Australia property is facing a perfect storm of an apartment glut, tight bank lending especially to buyers of apartments when they may be most needed and a close fought national election with property taxation a major policy battle-ground. It is no longer a matter of whether apartment prices will fall but what will be the fallout to financial stability and the rest of the economy. Add in a sudden reversal of fortune for commodity futures prices in China and intense scrutiny over financial stability and policy direction in China and the risks are all lining up for deeper rate cuts by the RBA and steeper fall in the already wounded AUD. The NZD looks more stable given rapid immigration underpinning its property market. But its central bank is preparing more macroprudential measures and a weaker AUD and lower RBA cash rates are likely to pressure the RBNZ towards more rapid action.

A reversal of fortune

The AUD has taken quite a bath lately and it may be in for a further dunking yet. The good news stories of the economy over-coming its mining sector down turn and rebounding Chinese metals prices only weeks ago have been over-run by fear over a glut of apartments and tightening bank lending conditions for foreigners that are the mainstay buyers of those apartments, and a rapid reversal in Chinese metals prices.

Preoccupied Australian banks

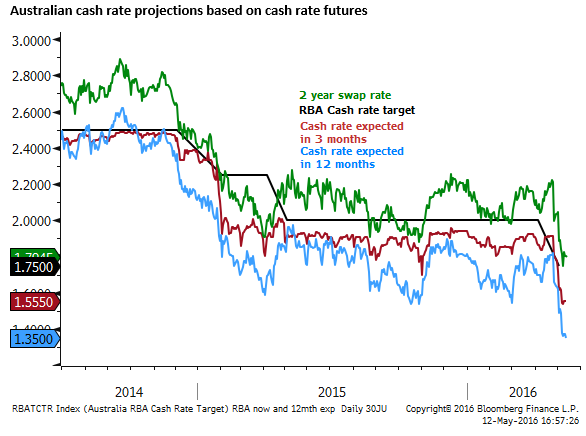

Of course the trigger for a rethink by many on the AUD was the RBA rate cut earlier this month that caught many local bank economists napping. One wonders if the local banks are so pre-occupied with preparing for litigation over alleged domestic money market rate rigging, on-top of several other scandals that have the opposition Labor party calling for a Royal Commission, dealing with rising loan loss provisions and scurrying to close off lending to foreign investors in apartments, that they lost focus on forecasting RBA policy.

Now suddenly after the RBA has updated their inflation forecasts, the banks are all forecasting at least one more rate cut, probably after the 2-July national elections.

Complex relationship between Australia and China

Broader sentiment about China has deteriorated in recent weeks with growing concern over its financial stability. Key economic data due later today from China may generate some volatility, but even if it is better than expected the market is likely to treat it with skepticism.

Australia has in part been able to grow solidly over the last year even as its mining sector has deteriorated in part because of rapid capital outflow and spending from China on its property, tourism, education and agriculture sectors. Perhaps even the down-turn in Chinese property, fears of financial and economic stress, and a Chinese government corruption crack-down helped boost Chinese capital outflow and spending in Australia.

Most had thought that the AUD was a proxy for Chinese growth and investment via its demand for Australia’s iron ore and the broader impact on global demand for other commodities. But the rebound in the AUD to recent highs probably owed much to increasing Chinese influence in non-mining sectors.

The influence China now has on Australia is immense but also complex and the two are as linked as any country in Asia to the fortunes of China. It is fair to say that the AUD would have fallen much further below 70 US cents perhaps into the 50s if it were not for bourgeoning Chinese demand for non-mining sectors in Australia.

Perfect storm brewing for Australian property market

However, the flood of capital from China fueled a surge in apartment building in Australia, and now the goods news side of this boom is over and the bad news is there is a glut. Prices are falling, generating problems that may drag on confidence in Australia.

Corelogic research estimates that there are 92,102 new units set for completion over the next 12 months, more than doubling to 231,129 over the next 24 months. Corelogic Researcher Cameron Kusher said, “The large volume of new stock, coupled with an ever-growing supply of existing stock, means that historic high levels of unit settlements are due to occur over the next two years in most cities,”

He said, “Even a recurrence of the peak year for sales in Melbourne and Brisbane over the next two years wouldn’t represent enough demand to cater for all of the new units set to settle over the coming 24 months.”

The Corelogic data on previous sales vs new supply are not as out of whack in Sydney, but it is still not pretty.

Brisbane, Melbourne face rising apartment settlement risk – AFR.com

Significantly compounding this risk is that Australian banks have all abruptly tightened lending to buyers of apartments precisely because, it seems, they are worried that these loans may turn bad if apartment prices fall. The biggest demand for these apartments comes from foreign, mainly Chinese investors. Banks are worried that these buyers that mostly reside and earn income abroad will be out of legal reach if loans go bad. The incentive not to pay will grow if prices fall leaving investors in negative equity. Australian bank lending to this sector had been growing rapidly and banks have suddenly awoken to the risks.

Furthermore, banks have also been found out for poor verification of loan documents this year, and a great deal of this has been on foreign investor loans. Only in recent months have they tightened up this process and appear to have made a decision that the whole business of lending to foreigners for apartment purchases is too risky. It started with ANZ and has quickly spread to all the banks as they responded to surges in loan enquiry.

(Discussed in detail in our report AmpGFX – Elevated and rising risk factors for AUD, 28 April, and in the following news report: Why the banks stopped funding Chinese investors – AFR.com, 12 May).

While many foreign buyers may still have the cash to pay-up without getting a loan from Australian banks, it is highly likely that this sharp and sudden tightening in lending conditions will kill a good part of the demand for apartments just at the time when more buyers are needed.

A weak apartment market may trigger problems for developers especially if buyers off-the-plan decide to pull-out of the deal leaving developers with assets they can’t move and debts to pay.

A weaker apartment market may spread to the broader housing market and discourage domestic investors that may want to unload highly leveraged property investments. A weaker housing market may undermine broader household economic confidence as well as lead banks to further tighten lending conditions, creating a vicious circle.

Election Wild Card

A wild card is that if the Labor opposition win the 2 July election their policy of limiting negative gearing to new properties and reducing the capital gains concession on investment properties is likely to further weaken sentiment for housing.

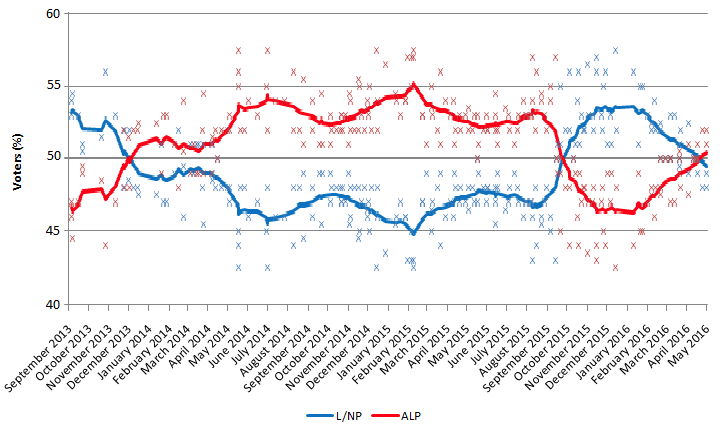

Polling for the election appears neck and neck, although the betting market is favoring a return of the Liberal National Coalition. In any case, property taxation is turning out to be a major election issue and the debate/scare campaign on this issue is likely to dampen investor sentiment in the lead up to the election.

The following are links to the main polls:

Newspoll Data – TheAustralian.com.au

The Poll Bludger – Crikey.com.au

ReachTEL polling – reachtel.com.au

The chart below shows aggregated data on polling for the Australian election. When PM Malcolm Turnbull took over from Tony Abbott as leader of the Liberal National Coalition and Prime Minister in September last year, polling for his government improved sharply from likely to lose the next election to a solid lead. However, his position has slid rapidly since around Feb/Mar such that the race now looks very tight.

The betting market still significantly favors re-election of LNC led by Turnbull. With implied probability of about 75% that he is returned to power, while the odds for the Labor Party imply a probability of about 30% it wins.

Australian Government betting odds – oddschecker.com.au

The Trouble in the Bubble

It has all the hallmarks of a market that has over-extended and on the verge of a major down-turn. The main questions are not whether apartment prices fall, but how far and how big a fallout to the wider housing market and economy.

The RBA will be called on to step in as a circuit breaker by cutting rates to offset the fallout. Lower rates may encourage support for other segments of the housing market and help limit the fallout. A lower exchange rate may help reboot demand from more cashed up foreign buyers. But it remains to be seen how effective lower rates and exchange rate will be in stabilizing the outlook for the Australian economy.

As important in this equation may be how easy it is for Chinese buyers to get capital out of their own country and achieve sufficient finance from other sources. And this also depends on Chinese government policy on cross-border capital controls and lending conditions in China.

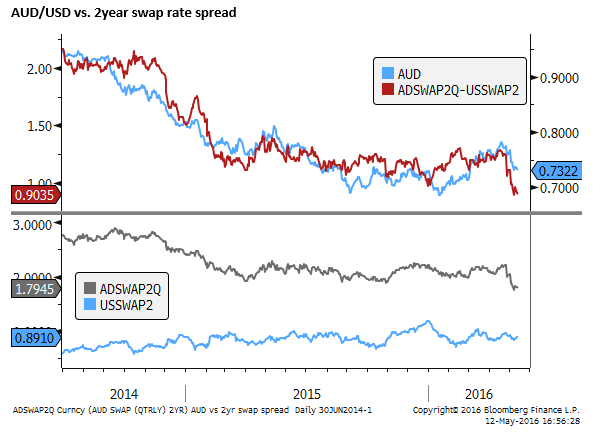

In most respects the risks are much larger to the downside for the AUD for the foreseeable future.

Rapid immigration a key point of difference in New Zealand

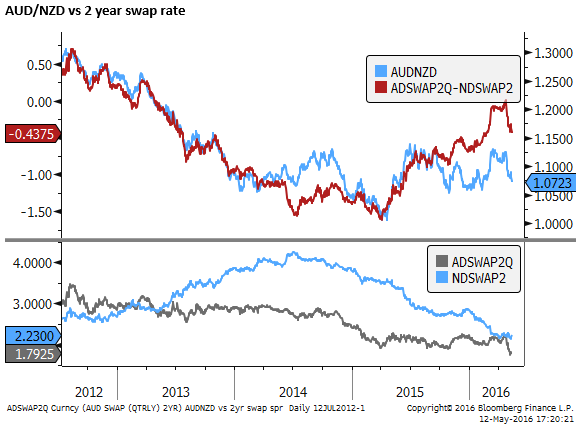

The AUD has already fallen sharply compared to its commodity currency peers in recent days including the NZD.

The fall in the AUD/NZD exchange rate and the prospect of further RBA rate cuts will place some additional pressure on the RBNZ to follow up its March rate cut. The odds of a cut at its next policy meeting on 9 June, also a quarterly Monetary Policy Statement release date, are 56%, although this fell from 78% just before the RBNZ released its Semi-Annual Financial Stability Report earlier this week.

A key point of difference between Australia and New Zealand is record rapid immigration to New Zealand generating an under-supply of housing especially in its capital city Auckland. House prices continue to rise sharply.

The RBNZ has enacted loan-to-valuation ratio restrictions on bank lending to contain house prices in Auckland. But after a brief pause in house price growth in Auckland, prices have begun to rise too rapidly again, and more broadly across the country.

This is making it difficult for the RBNZ to cut rates again, even though they have indicated further cuts may be required to achieve a rise in inflation back to its 2% medium term target.

Nevertheless, the RBNZ have essentially indicated that it plans further macro-prudential measures to contain housing price and credit growth. These are likely to open the door for further rate cuts.

However, the market was disappointed that the RBNZ did not announce specific measures in its FSR, and it may take many months to set up the framework for new measures. The question is whether the RBNZ is prepared to cut rated in advance of new macroprudential measures. It may prefer to wait until more progress is made on new measures that appear likely to replicate the UK policies of placing a limit on debt to incomes.