Australia to deliver on infrastructure

The Australian government budget next Tuesday is set to announce significant debt-financed infrastructure spending. This contrasts with the Trump administration that touted big spending on infrastructure spending and tax reform, but then placed more emphasis on border control, immigration, health care and trade policy. Its more pro-growth tax and infrastructure policies face an uphill battle in Congress. Australian government budget policy is also likely to appear supportive for the housing market. The RBA has already shown its support for infrastructure spending and is likely to sound cautiously optimistic and leave policy neutral. The NZ labour data may be crucial for the RBNZ policy outlook. Any evidence that tightening labour market conditions are starting to lift wage growth will put considerable pressure on the RBNZ to lift its sanguine inflation outlook after its recent stronger than expected Q1 CPI report. The bounce in AUD and NZD on Monday from multi-month lows is at risk of extending. EUR has baulked at the mid-1.09s in the last week, but economic momentum continues to rise relative to other major economies and political risk is easing. UK economic momentum, on the other hand, may be ebbing, and resurgence in the GBP may stall as the EU signals it will play hardball in Brexit negotiations.

Australian government to embark on debt-financed infrastructure spending

The Australian government is expected to announce an increase in infrastructure spending in the annual Federal budget on Tuesday, next week, 9 May. In the process it plans to split the borrowing to pay for spending on infrastructure into a separate part of the budget, allowing a much longer glide path to return to overall budget surplus. (Projects include a second Sydney airport, a rail line between the three major cities on the East coast Melbourne-Sydney-Brisbane).

Federal budget 2017: Reporting shake-up sparks debt spree concerns – SMH.com.au

Government can build better, cheaper infrastructure than private sector: Morrison – AFR.com

It is interesting to note that the Trump administration got the market very excited about big infrastructure spending during and soon after his election campaign. But instead, Trump gave priority to policies on immigration, border control, healthcare, and trade. Policies that are more clearly designed to boost growth face an uphill battle in Congress.

Of course, it will take a year or more before infrastructure spending will begin to significantly contribute to growth in Australia, but the shift in tact by the government is not likely to find much political resistance and will tend to boost economic confidence.

Budget to continue tax breaks for housing investors

The Australian government is also expected to allow first home buyers to access retirement savings, or direct income into a tax-preferred savings accounts, to help them save for a deposit to buy a house. Whereas it has eschewed alternatives that might dampen investor demand for housing by reducing their tax incentives. The result may be seen as a support for the housing market, dampening fear of a peaking in housing prices.

Federal budget 2017: To help home buyers, Morrison might have to push up prices – SMH.com.au

The housing market, more so for apartments that are moving into a period of over-supply in the major cities, is showing signs of peaking, after a renewed surge in the last year. Banks have been tightening credit conditions for investors and foreigners under pressure from regulators in recent months. Fear of fallout from a weaker housing market has probably dampened the AUD somewhat this year. Such concerns remain, but the latest news of an expansionary budget and no significant tax changes for property investors tends to support overall economic confidence and the AUD.

RBA to show cautious optimism

The RBA will announce its latest policy today and its quarterly Statement on Monetary on Policy on Friday, 5 May. RBA Governor Lowe will deliver a speech on Thursday, 4 May on “Household Debt, Housing Prices and Resilience”.

The RBA is widely seen as reluctant to cut rates further despite undershooting its inflation target, due to the high level of household debt, and systemic risks in the housing market. As such, the topic of this speech seems to offer a forum for sounding more hawkish.

Governor Lowe has also been supportive of governments using low borrowing costs to finance infrastructure spending as a way to support the economy. As such, he may offer support for the proposals expected to be in the government budget.

The Q1 Australian CPI data were at or slightly below expected, released last week, but were encouraging in the sense that they showed improvement from year-ago levels and are consistent with RBA forecasts for a gradual return to target. Furthermore, the Melbourne Institute monthly inflation gauge rose in April to 2.6%, a high since 2014, above the middle of the RBA’s 2 to 3% target.

The RBA will continue to have reservations about the strength of the labour market, wages, and consumer spending. But business surveys remain above average and global growth indicators remain on an improving trend. As such, the RBA is expected to maintain a steady course for the policy outlook.

New Zealand labour market data may set tone for RBNZ policy meeting

New Zealand Q1 labour data is due this week, Wednesday 3 May, Tuesday afternoon in the USA, ahead of the RBNZ policy meeting and quarterly statement on monetary policy next week on Thursday 11 May.

The Q1 NZ inflation data were stronger than expected and suggest that there has been a step-up in underlying inflation, approaching the 2% target somewhat faster than previously anticipated, after a number of years of above-trend economic growth.

Any evidence in the labour data that dormant wages growth is starting to respond to tightening labour market conditions may trigger a significant rethink on the neutral policy outlook at the RBNZ.

The NZD has been under pressure recently, falling against the AUD, and sitting near its lowest level against the USD since June last year.

While NZD may appear expensive on longer term metrics (From 20,000 feet, NZD looks set to free-fall this year, without a parachute, 9 March – ampGFXcapital.com), more recently its decline has been somewhat against the grain. NZ economic data has remained on a solid trend, NZ inflation has been strong, dairy prices have firmed since last year, and the USD has tended to be soft compared to a number of emerging markets as global growth indicators have strengthened. Longer term US yields have fallen. Confidence in the ability of the Trump administration and Republican-led Congress to enact the tax reform and infrastructure spending has waned.

Eurozone leading major economies’ recovery momentum

Eurozone, the first of the majors to report inflation for April, showed a solid uptick in core inflation.

PMI manufacturing data showed further strength in the Eurozone in preliminary data reported on 21-April (final data due on Tuesday this week, 2 May). It rose to 56.8, a new cyclical high, whereas USA Markit PMI (52.8) and ISM manufacturing (54.8) reports have declined in the last two months to April. UK manufacturing PMI data for April are due on Tuesday, they have ebbed in Feb/Mar.

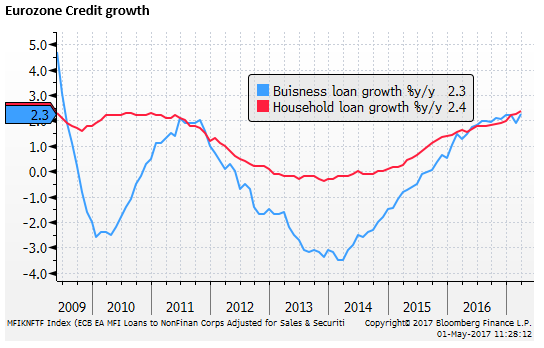

Eurozone credit data released on Friday 28 May, showed further acceleration in loan growth to households from 2.3% in Feb to 2.4%y/y in March; a high 2009. Business loan growth also recovered from a dip in Feb to 2.3%y/y, also a high since 2009.

Eurozone political risk diminishing

The final round of the French Presidential election is this weekend, Sunday 7 May. Betting odds give Macron a 90% probability of winning, and Le Pen a 15% chance. It appears that political risk in the Eurozone has diminished significantly.

Further supporting the case for stability, Former Italian PM Renzi regained leadership of Italy’s centre-left Democratic Party (DP). He won a comprehensive 70% of the vote of party members for party leadership. Renzi is now party leader, but is not currently a member of the Italian government (Chamber of Deputies) since he resigned after the no result in the referendum on constitutional reform he championed in December last year.

Renzi, as leader of the DP, could push for an early election by withdrawing support for the current government led by PM Paolo Gentiloni, also a member of DP. The DP govern in coalition with centrist parties in a fractured parliament.

However, the DP is still running behind the Euro-sceptic, leftist, Five Star Movement in recent polls. Bloomberg reports that a 28 April poll showed Five Star had 28.4% support ahead of DP at 27.3%. And PM Gentiloni polled at 31%, 2 percentage points ahead of Renzi as preferred PM.

An election is due to be held no later than 20 May 2018.

Renzi Faces Uphill Battle to Italy Premiership After Primary – Bloomberg.com

A ‘fresh start’ for Renzi as he recaptures centre-left leadership – FT.com

EU cuts down UK Brexit ambitions

The GBP has bounced since PM May, leader of the Conservative Party, called an election on 18 April to be held on 8 June. The Conservatives are seen as winning the election convincingly, increasing their majority and strengthening the hand of PM May to conduct Brexit negotiations with less discord in UK parliament. Bookmakers’ odds give the Conservatives around a 90% chance of gaining an outright majority of seats and holding government. The next most likely alternative outcome is a Conservative-led minority, given around a 9% chance.

The polls of voting intensions show modest improvement in support for Labour since the election was called, to near 29%, but only after its support had drifted persistently lower since the Brexit vote in June last year. The main pro-EU party, the Liberal Democrats, have seen no improvement, steady around 10%. Conservatives are polling around 45%.

General election 2017: Polls and odds tracker – Telegraph.co.uk

However, the complexity and difficulty of Brexit has not changed and news in the last week point to the challenge ahead, suggesting upside for GBP is still limited. The EU27 showed solidarity at a summit on the weekend, and German Chancellor Merkel warned the UK about harbouring “illusions” over its desired outcomes.

The EU-27 set out their guidelines for Brexit negotiations at a summit on Saturday, 29 May. They insist that “sufficient progress” be made on the terms of the financial settlement (said to be a cost to the UK of up to EUR60bn), the rights of EU citizens in the UK and the future of the Irish border, before commencing negotiations on a new trade deal between the UK and the EU. PM May has said she would much prefer negotiations on trade begin early in the process in parallel with these contentious issue of the costs of exit.

The EU leaders expect a trade deal to take a considerable time after the 2-year time table (ends 29 March 2019) for Brexit set out in Article 50 process for EU exit. PM May has been hoping for one in place when Brexit is complete. Fear of a cliff edge or limited progress on trade are likely to remain high in the UK. Slow progress on a trade deal may be used by the EU as a bargaining chip to get concessions on the price of exit.

Angela Merkel warns Britain over Brexit ‘illusions’ – FT.com

EU calls Theresa May’s Brexit stance ‘completely unreal’ – FT.com

European Council (Art. 50) guidelines for Brexit negotiations – consilium.europa.eu