Diverging EM assets and currencies, Global investor jitters, AUD Vulnerable

The USD has strengthened since September after trending down for the first eight months of the year. Its gains have stalled in recent weeks, and the jury is out as to whether it will revert to its weaker trend earlier in the year or push on. The rebound in the USD since September has some sound fundamentals; strengthening US economic reports, Fed sticking to its guns, and tax policy reform progress. However, the market is not convinced; US bond yields tried to go up, then slipped back. Equity investors have not yet been overly perturbed by the USD rebound, continuing to drive up global equities. Emerging market currencies have been caught somewhere between following stronger EM equities higher, or falling back against a firmer USD. In the first eight months of the year, the dollar smile theory was playing out with moderate US economic growth and weaker inflation trends sending capital towards EM and other developed market equities where growth was stronger and synchronized. This helped reinforce the USD down-trend and see the market tend to ignore a firming US rates advantage. We are now seeing an unusual divergence in EM bonds and currencies from EM equities. They will probably have to converge at some point either because the USD resumes broader weakness, or EM equities correct lower in a stronger USD environment. Amidst the broader uncertainty, we see downside risk for the AUD as the RBA reinforces a cautious steady monetary policy stance after weaker than expected Q3 CPI inflation, increasing political uncertainty, a slowing housing market, and Chinese commodity demand risks.

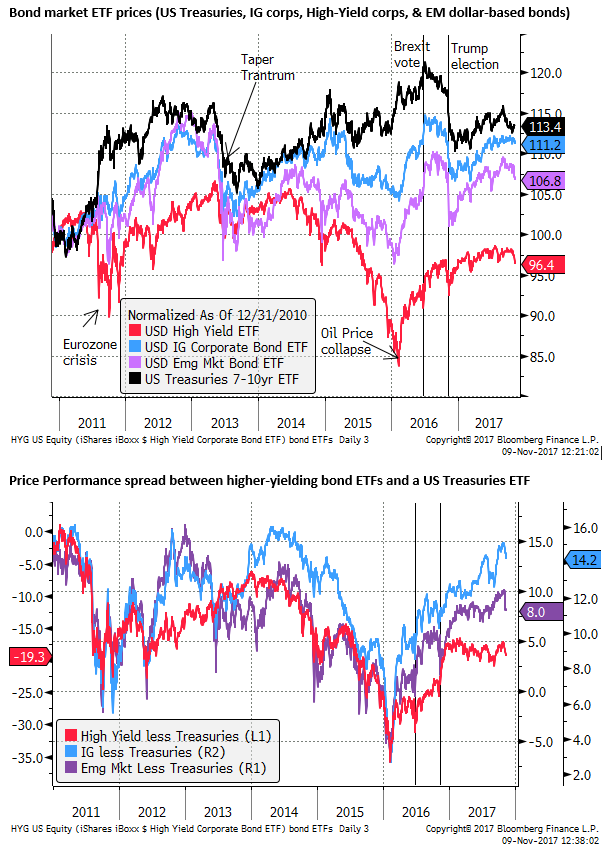

Jitters in high yield bonds

The last two years have been notable for strength in high yield and EM assets. However, in recent weeks we have seen some jitters. The chart below helps put this into longer-term perspective for bond markets. Its shows bond market ETFs (rising values implies lower bond yields).

US Treasury bond (7 to 10yrs) ETFs reached a peak for the year in early-September, a point of heightened USA political uncertainty, fears over the hurricane fallout on the US economy, and low USA inflation outcomes dampening expectations for Fed rate hikes or tax reform.

US Treasury ETFs fell to a recent low on 26-Oct, as tax reform hopes increased and the Fed stuck to its plan to remove QE and rate hike projections. In recent weeks, US yields have slipped again, and Treasury ETFs have recovered some ground.

In Sep/Oct, global investor risk appetite remained buoyant; higher yielding bond markets remained relatively stable even as US Treasury yields rose, narrowing yield spreads over US Treasuries (resulting in out-performance in these higher yielding ETF values relative to US Treasury ETFs). This is illustrated in the second panel of the chart below that shows rising spreads, to recent peaks in late-October, between the value of higher yield ETFs (investment grade corporate bonds, high yield corporate bonds, and emerging market dollar-based bonds) and the US Treasury bond ETF.

Since late October, we have seen some under-performance in high yield bonds relative to US Treasury bonds. However, as the chart below illustrates, in the broader context, so far, this represents a relatively mild correction in global investor risk appetite.

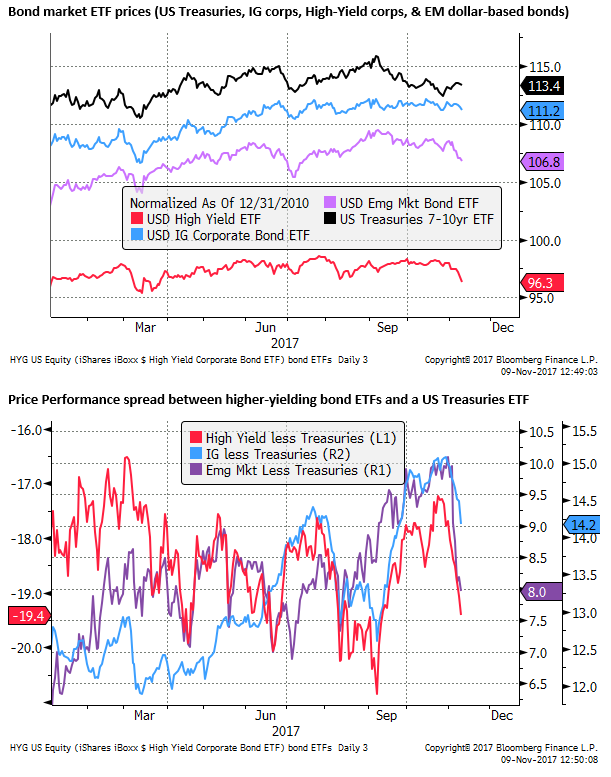

To help visualize the recent events, the charts below zooms in on the above chart to look at only the year-to-date.

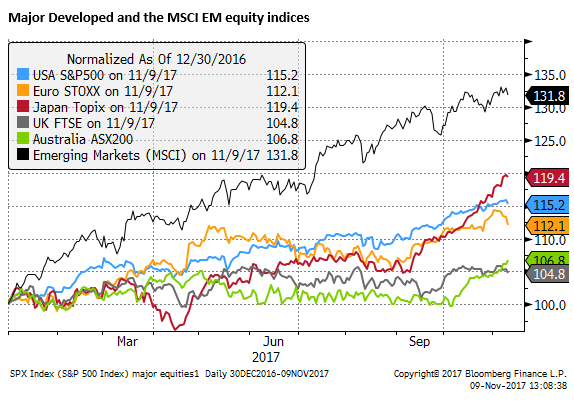

EM and developed market equities remain strong to-date

The mild under-performance in high yield bond markets (since around 26 October for high yield corporate bonds, 30-October for IG corporate bonds, and 3-November for Emerging market bonds) has been less apparent and more recent in global equity markets. The chart below shows major developed markets and the MSCI EM market equity indices.

To help visualize recent events, the chart below re-normalizes the indices starting this year, and shows the year-to-date performance. While softer in the last day, global equity markets are just off long-term highs.

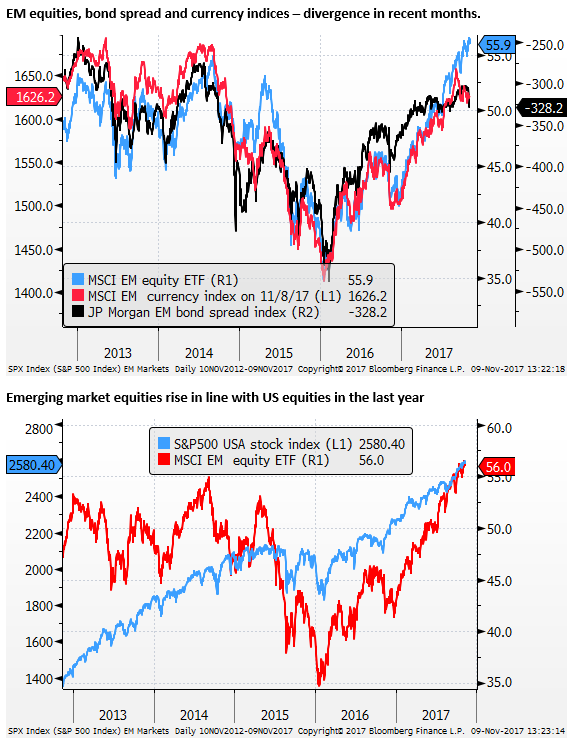

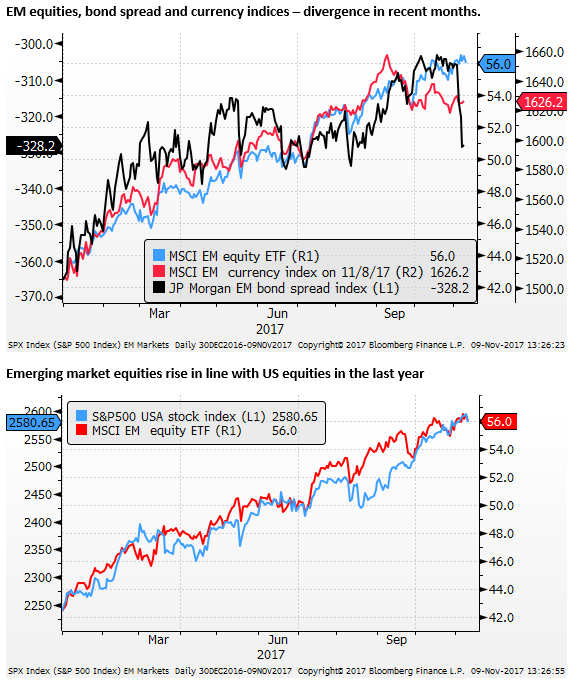

Emerging market equities diverge from currencies and bonds

The rally in emerging market equities has continued in recent weeks, even though emerging market bonds and currencies have tended to fall. EM equities may be moving in line with developed market equities. However, in the past, they have been more correlated with EM currencies and EM bond spreads. The chart below illustrates this divergence.

Again, to hone in on recent developments, the charts below zoom in on the chart above to focus on the year-to-date.

The chart above shows that the MSCI EM currency index peaked on 8-Sep, although it has been relatively stable, or at least trendless, since late-Sep. As discussed earlier, EM bond yield spreads have widened out since around 3-Nov. EM Equities are still firming, in line with global equities.

We might conclude that EM currencies and bonds should reconnect with EM equities soon, either because EM currencies and bonds bounce back from recent weakness, or EM equities correct lower.

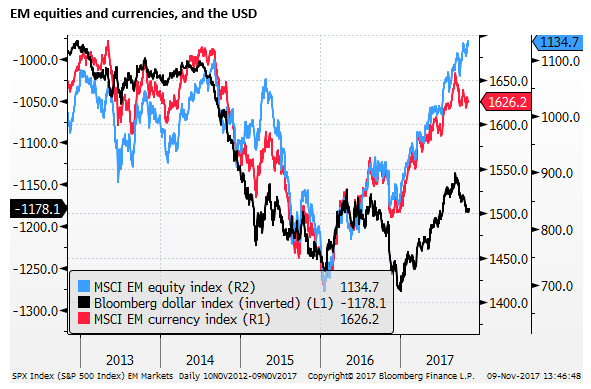

EM currencies torn between EM equities and the USD

While EM currencies tend to be highly correlated with EM bond and equity performance, they might also reflect the broader performance in the USD exchange rate. The chart below brings the broader USD performance into the picture. We find that EM currencies and assets tend to follow broad swings in the USD; in that a weaker USD tends to be associated with stronger EM currencies and assets and vice versa.

However, the recent divergence in EM currencies from EM equities reflects broader strength in the USD (weaker EM currencies). Up until early-September, the USD had been in a falling trend this year, consistent with rebounding EM equities and currencies. However, more recently the USD has recovered; including against EM currencies that have tended to weaken since early-September, even as EM equities have continued to rally.

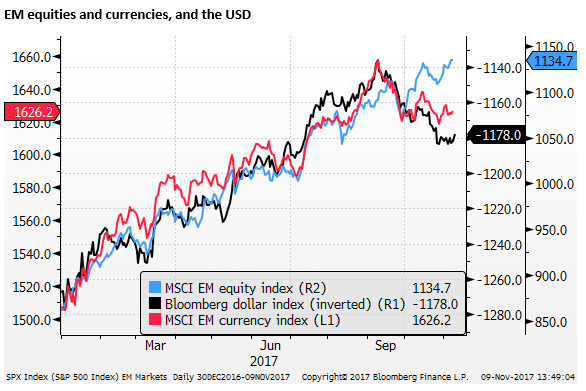

As before, the chart below zooms in on the chart above to focus on the year-to-date. We can see more clearly the recent divergence in EM currencies and EM equities, and the broader USD performance. EM currencies have been torn since late-Sep between following stronger EM equities or being dragged back by broader strength in the USD.

Looking ahead, we might expect this recent divergence to converge again. This might arise either because the USD resumes its weaker trend in the first eight months of the year, or EM equities fall back, and EM currencies resume their weaker trend since early-September.

The USD strength has stalled since around 26-October, operating in a sideways trend in recent weeks. On Thursday, it is showing some weakness, pressing the weak side of its recent range.

Dollar smile theory has played out

The weaker USD for most of this year has been a surprise to many investors, considering the promise of the Trump/Republican control of government, and their tax reform and infrastructure spending policies. And two hikes by the Fed, with a third now almost fully anticipated in December.

The weaker USD narrative this year has followed that of the dollar smile theory. US growth momentum has been moderate, but not stellar, and no more special than a global recovery that has become more synchronized. US inflation has remained low, in fact, it has fallen unexpectedly from a peak early in the year. As such, USA yields have not risen so much to unsettle investor appetite that has been buoyed by stronger earnings growth.

This moderate growth outlook in the USA has encouraged more investment in global equity markets, including other developed and EM equity markets. This has tended to result in capital outflow from the USA, helping generate a self-reinforcing fall in the USD and rise in EM assets and currencies.

Broadly speaking, currency markets, especially EM markets, have paid relatively little attention to US rates or yields than they have in the past. The movement in US rates and yields have not been significant enough to move the dial on global investor confidence in global equity markets.

Looking ahead, we cannot say at this stage whether the dollar smile theory will return to dominance (as it was in the first eight months of the year) and see a return to a weaker USD and stronger EM currencies and equities.

Or whether the market will respond to recent evidence of a stronger US economy in recent months, and the prospect of a Fed continuing to hike rates and reduce its balance sheet. Key to this story is tax reform progress. This might further boost confidence in US growth and assets. It might lift rate hike expectations in the USA and support the USD.

Another factor to watch is inflation and wages in the USA. The USA labor market has tightened significantly, and wage pressures could emerge. This would be a significant surprise to the market that has come to see the global Phillip’s curve as permanently flat and technological disruption and globalization holding inflation perpetually low.

Alternatively, equity markets globally might move into a corrective phase. The equity market could take a lead from high yield bond markets that have weakened recently. This may reflect some concern over valuations in equities and concern that the global recovery may be levelling out, resulting in capital withdrawing from EM markets.

This might support low yielding major currencies like JPY and EUR. However, the EUR has extended well above its negative/low yields this year and may have taken on some of the attributes of EM markets, driven up by net equity inflows. As such, it too might weaken if global risk appetite takes a clearer set-back. In essence, we may move to one side of the USD smile (where it turns up) and see the USD strengthens against most other currencies.

We don’t have a clear view on the outlook at this stage.

US political uncertainty lingers

US political uncertainty continues to be a drag on the USD and is preventing it from benefiting all that much from the tax reform proposals that if passed should significantly boost the USD.

As we discussed in our report (Without tax reform division may swamp the USD; 1 Nov – ampGFXcapital.com) there is something very binary about tax reform. In may present the last opportunity for the Republican Party to pull itself together and generate some badly needed positive momentum going into the November 2018 mid-term elections. A failure to come together on tax reform is likely to see a disintegration in government, led by a highly destructive blame game, fueled by President Trump. The FX market is reluctant to build in the possibility of tax reform because it must also consider the possibility of a highly dysfunctional government.

The Democratic win in the Virginia gubernatorial election last weekend may have undermined confidence in the USD somewhat, providing a reminder of how important tax reform is for stabilizing the Republican Party, the Presidency, and overall government.

The Mueller investigation and counter allegations by Republicans against the Clinton campaign also remains a background threat to political stability. The indictments announced on 30 October are considered to be only the start of a long process that may heap pressure on the President and Congress. At best it could be a distraction that delays tax reform. At worst it could be used to bring down the President and throw the government into turmoil. If tax reform fails to be passed ahead of the mid-terms, the Mueller investigation could completely swamp political discourse.

To the credit of Republicans in Congress, they appear to understand the importance of this tax bill and they are working rapidly and with more purpose to get it moving with ambitious targets. The small milestones being met, despite the inevitable disagreement over the details, is probably helping sustain recent gains in the USD.

AUD vulnerable

In the midst of this uncertainty, we are biased towards seeing downside risk for the AUD. The RBA policy statement on Tuesday revealed that it might be pushing forward the timing of its forecast for underlying inflation returning to its 2 to 3% target band. We should hear more on this today in the quarterly Statement on Monetary Policy. As such, the RBA looks further from raising rates.

Further weighing on the AUD is political uncertainty. Several local pundits are betting on an early election, or a series of by-elections that could result in a shift in the balance of power to the Labor Party early next year. The ruling Liberal/National Coalition is lagging in polls and a number of parliamentarians have been forced out or may be in coming months due to questions over dual citizenship and legal eligibility to hold office.

The citizen distraction has got in the way of serious policy decisions, and the outlook for policy direction remains unclear. For instance, if the Labor party takes power next year, it might push ahead with its policy to remove negative gearing on housing investment, generating a significant risk of a downturn in the housing market and a weaker outlook for the economy.

The AUD also runs the risk of being highly leveraged to the construction and fixed asset investment in China. Growth in China and its property market has been mixed in recent months, as have iron ore prices, and China may be moving into a phase where it is tackling excess leverage, threatening its growth outlook.

The Australian housing market is showing clearer evidence of losing momentum, and while business investment and government infrastructure spending have picked up, Australian consumer demand appears to have weakened. Overall it appears that the RBA will continue to walk a cautious line on its rates outlook.