Uncertainty and contradictions

There are ongoing high levels of global uncertainty related to Brexit, uncertain US government policy direction, modest policy tightening in China, and central banks that are sending mixed signals. There are contradictions in the market with very high consumer confidence in the USA, but a deteriorating approval rating for President Trump. Strong surveys, but modest economic activity readings. Ongoing optimism for tax reform in the US equity markets, but doubts apparent in somewhat lower US bond yields. We continue to see risks of the Trump aura in equities fading on the tough road to tax reform. This could undermine the USD further in coming months. The EUR may benefit as evidence of recovery builds and French political risks fade.

USA Consumer most confidence since the Dotcom bubble

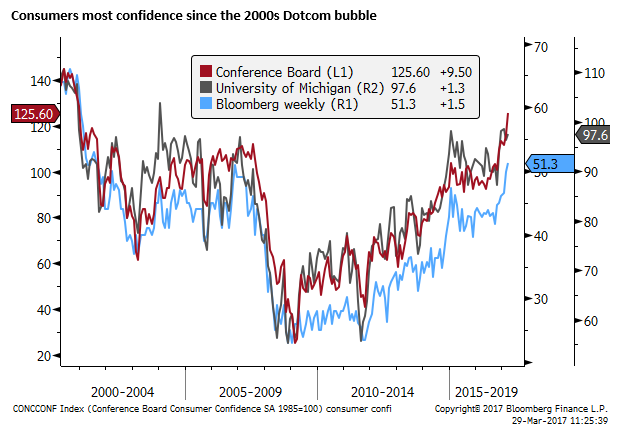

The Conference Board Consumer Confidence survey showed a surprising further gain in confidence and a range of sub-measures including on employment.

The chart below shows three different consumer confidence surveys, the Conference Board measure rose to a high since December 2000 (not long after the peak of the dotcom bubble). Apart from this period around 2000 of extreme optimism, this is the highest reading since the late 1960s.

The lift in the result was heralded by the Bloomberg weekly consumer comfort index (last data point 19-March); at a high since 2001.

The University of Michigan preliminary confidence reading in March was somewhat below its peak in January. This level is around the peaks in 2004/2007, essentially around the highs since early-2001.

The cut-off date for the Conference Board survey is 16-March. The survey covers the first half of March. The US equity market was relatively stable through the first half of March.

These consumer surveys do not cover the last weeks of March when the Republican-led House of Representatives failed to pass the Trump-endorsed Healthcare bill.

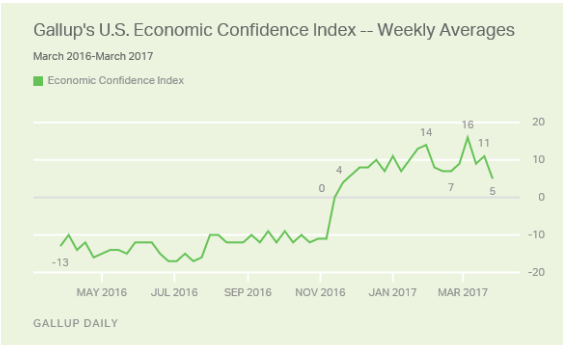

It does appear that confidence has taken a hit since this failure. The following weekly Gallup poll of US economic confidence slipped in the week ended 26 March, taking in the bill’s failure.

(US Economic Confidence Drops to Lowest Level Since Election – Gallup.com)

How much of a hit has confidence taken? The starting point suggests that consumers were very confident in early March. They were buying into the idea that the US economy was on a solid growth path and that the government, led by Trump and Republicans, would further support growth with tax cuts, infrastructure spending, reduced regulation, and bring jobs back.

The Healthcare bill was seen as an important first test of the Trump/Republican government. If Trump could ‘fix’ healthcare early in the administration, the public may be able to overlook controversies such as his campaign’s alleged links to Russia, and it would enhance the perception that he is a deal-maker that can control Congress.

The Healthcare bill failure takes considerable gloss off this perception. The risk is that the public turns its attention to Trump’s foibles, of which there are many.

How Teflon-like is Trump?

So far this week, we have not seen further correction in US equities, a barometer of confidence. Trump and Republicans have said they will now concentrate on tax reform. This is more important for boosting the growth outlook. Trump has said he is prepared to work with Democrat to push through his agenda. He and his press supporters did try and deflect blame a bit to the right-winged Freedom Caucus, House Speaker Ryan and Democrats. But Trump has not gone on a Twitter storm turning on his own.

Trump has, however, continued to run his own spin on twitter; arguing that Democrats will soon come to him to renegotiate healthcare when Obamacare fails, deflecting the Russia controversy to the Clintons and their aides, taking credit for a new investment by Ford in Michigan, promoting his media supporters on Fox and Friends, and taking swipes at the New York Times and other “fake” media. He tweeted, “If the people of our great country could only see how viciously and inaccurately my administration is covered by certain media!”

@realDonaldTrump – Twitter.com

However, Trump spins it, the market must now wonder how successful Trump/Republicans will be in crafting a tax policy that will pass Congress. Many believe this will be just as difficult, if not more so, as finding agreement on healthcare.

A key issue is how to pay for tax cuts. The controversial border tax is supposed to raise revenue, but lacks widespread support. The reform of healthcare itself was supposed to make some budget savings, but this has failed.

A further problem is that Trump has promised so much with respect to tax reform that he can’t possibly deliver. Part of the reason the Healthcare bill failed was that House Republicans could not draft a bill that could meet the lofty conflicting promises made by Trump.

Furthermore, one must wonder at the Democrats willingness to work with Trump on tax reform or Healthcare after the large number of executive orders since taking power, many of which they disagree with, affecting immigration, climate policy and family planning.

Time to Redo the Math on Tax Reform Prospects – WSJ.com

Think tax reform will be easy for Trump? Ha, ha – Washingtonpost.com

Tax reform, the next Trump debacle – FT.com

One of the confusing contradictions in the market is that consumer confidence appears so strong, and yet the approval rating of Trump appears so low. The chart below shows that Trump’s job approval rating has dropped to around 35%, a new low, in the wake of the Healthcare bill failure. This is amongst the lowest for past Presidents

Gallup Daily: Trump Job Approval – Gallup.com

It remains the case that the Republican’s control both houses of Congress and the Presidency and, theoretically, should be able to pass more legislation, which is a source of optimism. But at its first major test it has failed, and the signs are that bipartisan support will be required to make substantial reform. An unpopular and divisive president, facing allegations of inappropriate links to Russia, will struggle to drive negotiations across the aisle.

The risk is that economic optimism still apparent in US surveys fades as the aura around the Trump presidency fades.

Hard vs. Soft USA data shows a different economy

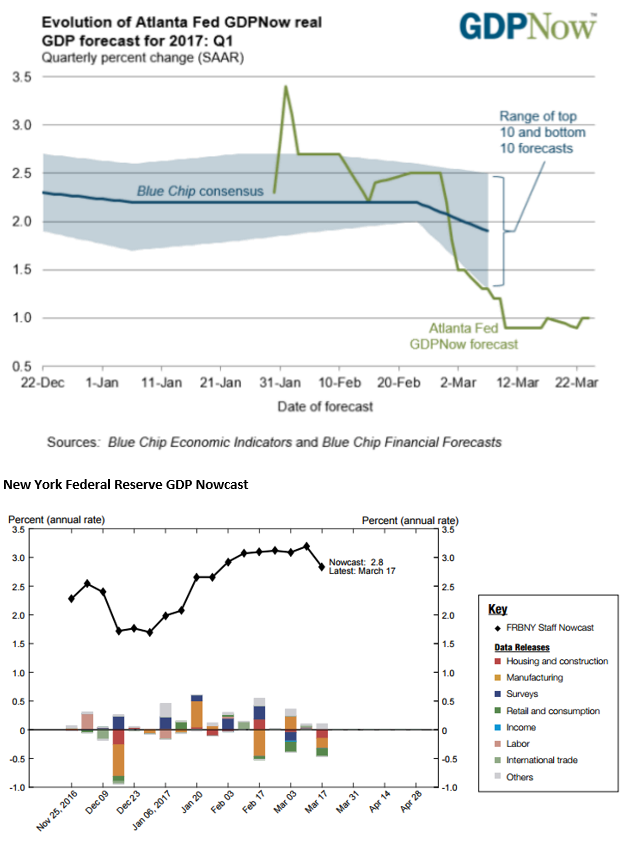

Another contradiction is that so far there has been little flow through from strong US measures of economic confidence to hard economic data. The softness in the hard data is apparent in the Atlanta Federal Reserve’s GDPNow forecast for Q1 of only 1.0% q/q SAAR (as at 24 March).

In contrast, the New York Federal Reserve’s GDP Nowcast is 2.8%q/q SAAR in Q1 (as at 17-March). Their forecast includes some up-beat surveys, such as the ISM and other regional manufacturing surveys.

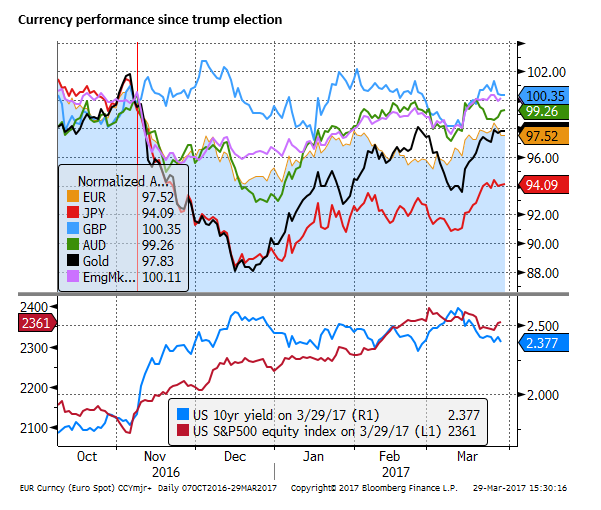

FX market lacking direction

It is hard to find clear direction in FX markets, although we are seeing some swinging moves. The USD appeared to weaken broadly as the healthcare bill failed last week, but bounced back this week. The EUR poked its head above 1.09 on Monday, a high since November last year, but has slid back to the mid-1.07s.

The fall seems at odds with the solid polling by Macron in the French election and strong PMI and IFO data on Friday and Monday.

There was a report today in Reuters citing unnamed ECB members, saying they were surprised that the market had projected rate hikes might occur early next year, and thought it had over-interpreted the 9 March ECB policy meeting. They said there was unlikely to be any further change in the ECB policy guidance in April, and the March meeting was meant to convey only less tail risk, not a step towards exit from the ultra-easily policy. This probably helped knock back the EUR, but sounds like standard jawboning by doves to prevent a rapid up-move in EUR. The market is likely to keep speculating about QE tapering and/or higher rates in 2018

Exclusive: Spooked by yield rise, ECB wary of changing message again – source – Reuters.com

The UK triggered article 50 to begin the Brexit process, and the Scottish parliament voted to press ahead with its call for a referendum to exit the UK. This news may have undermined the GBP modestly. The news is not a surprise, but underlines the long and uncertain process that may keep GBP cycling around a wide and directionless range for the foreseeable future.

We described anxiety in Australia over housing, electricity, Government budget and Chinese steel demand as undermining the AUD early in the week. However, it has bounced back in recent days on firmer commodity prices and stable US and global equities. Australian equities also rose strongly.

USA confidence fades, EUR fortunes rise, AUD angst builds – ampGFXcapital.com

The market is grappling with ongoing high levels of uncertainty related to Brexit and increased uncertainty over US economic policy direction. Equity markets have built in a relatively optimistic scenario for global growth. Global economic indicators have increased supporting emerging market currencies.

US bond yields remain lower this week, perhaps reflecting more doubts over the scope for effective policy reform in the USA, prevent a more positive response in USD.

Chinese corporate bond yields have been largely steady this week, but have been creeping higher, suggesting some tightening in Chinese monetary conditions.