Yellen greenlights March, emphasizes gradual, but risks have shifted toward more hikes this year

In a speech that was largely an historical account of the evolution of policy, Chair Yellen emphasized a gradual pace of policy tightening, while sending a clear signal that, barring a surprise, a hike on 15 Match is planned.

The USD has weakened on the speech mainly because Yellen has given no indication that the Fed has changed its mind since December on the pace of rate hikes (three this year). And she reiterated that this was the position of the FOMC in December.

Nevertheless, since they are close to mandated goals (“The economy has essentially met the employment portion of our mandate and inflation is moving closer to our 2 percent objective”), it is time to take another step to hike (“at our meeting later this month, the Committee will evaluate whether employment and inflation are continuing to evolve in line with our expectations, in which case a further adjustment of the federal funds rate would likely be appropriate”)

The speech went over the evolution in the Fed’s projection for the “neutral real interest rate”. The USD was quite weak in Q3 last year as Fed speakers were discussing their downward revisions to this rate.

(“In response to this growing evidence, the median assessment by FOMC participants of the longer-run level of the real federal funds rate fell from 1-3/4 percent in June 2014 to 1-1/2 percent in December 2015 and then to 1 percent in December 2016.”)

(“In the Committee’s most recent projections last December, most FOMC participants assessed the longer-run value of the neutral real federal funds rate to be in the vicinity of 1 percent.”)

So Yellen still thinks that the long run “neutral real interest rate” is still only one-percent. Which is low, and many would argue is pretty pessimistic. It suggests that the neutral long run nominal interest rate is only 3% (adding 2% for the Fed’s inflation target).

But that is in the Long run. The current neutral rate is lower still.

(“Moreover, the current value of the neutral real federal funds rate appears to be even lower than this longer-run value because of several additional headwinds to the U.S. economy in the aftermath of the financial crisis, such as subdued economic growth abroad and perhaps a lingering sense of caution on the part of households and businesses in the wake of the trauma of the Great Recession.”)

The current neutral real rate is seen at zero.

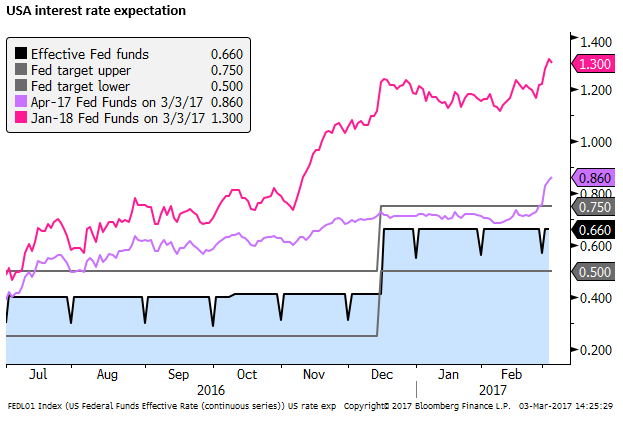

With the cash rate (effective fed funds rate) currently at 0.65%, and the core PCE deflator (excluding food and energy) at 1.7%, the current real rate is about -1%

As such, the current rate setting has the real rate about one percent below the neutral rate. Seen as moderately accommodative.

(“Some recent estimates of the current value of the neutral real federal funds rate stand close to zero percent. With the actual value of the real federal funds rate currently near minus 1 percent, a near-zero estimate of the neutral real rate means that the stance of monetary policy remains moderately accommodative.”)

This degree of policy accommodation is justified because inflation is still a bit below target.

In December, the FOMC median projection was for core inflation to rise from 1.7% at end 2016 to 1.9% at end 2017. Still a smidge below the 2.0% target, consistent with three projected hikes.

Yellen gave no indication that the FOMC would be upgrading this forecast for inflation at the 15 March meeting.

Beyond 2018, the Fed’s projected hikes reflect an expectation that the current neutral real rate (zero) will rise towards the long run estimate (one percent), and inflation rises that smidge further from 1.9% to 2.0%. About a three hike pace in 2018 and 2019 essentially reaching the neutral 3% rate.

Nevertheless, one might conclude that the fact that Yellen’s Fed thinks a hike in March is desirable, then it may be leaning toward seeing more than three hikes this year.

Perhaps, at the margin, the Fed is seeing a little more inflation risk, and some increase in their perception of the current and long-run neutral real rate.

This would be consistent with an improved outlook for the global economy (one of the headwinds) and less domestic caution as it recovers from the trauma of the Great Recession (another headwind).

But Yellen did not suggest that this was the case. Her speech only outlined the thinking that was in place at the end of last year, implying that the Fed hadn’t materially changed its view.

As we discussed in our report on Thursday (Fed already behind the curve, USD looks cheap compared to yield gaps, NZD expensive) alternative underlying inflation indicators are above 1.7% and in a rising trend, suggesting upside risk to the inflation forecast. Recent economic indicators also appear to be gliding above trend and the labor market is tightening.

As such, it would not surprise to see a strong employment report next Friday, and a high risk of an upward move in wages growth.

Furthermore, the risk is that then FOMC does upgrade its forecasts on 15 March to include four hikes this year, consistent with a rise in the inflation outlook from 1.9% to 2.0%.

Yellen said that, “we realize that waiting too long to scale back some of our support could potentially require us to raise rates rapidly sometime down the road, which in turn could risk disrupting financial markets and pushing the economy into recession.”

“Having said that, I currently see no evidence that the Federal Reserve has fallen behind the curve, and I therefore continue to have confidence in our judgment that a gradual removal of accommodation is likely to be appropriate.”

“However, as I have noted, unless unanticipated developments adversely affect the economic outlook, the process of scaling back accommodation likely will not be as slow as it was during the past couple of years.”

When someone has to say “I see no evidence that….” It is abundantly clear that there is indeed some smoke if not actual fire….. that the Fed is behind the curve.

Yellen seems firmer in her view that rates will be raised more frequently this year than the last couple of years. This may not be very hawkish. Rates were raised only once in each of the last two years. But it does appear to at least narrow the risk that the Fed will again stall its tightening cycle this year.

This whole speech was backward looking and appears aimed at warming the market up for a hike on 15 March without disrupting financial markets. The part aimed at softening the blow (still gradual) tended to cause some retracement in the rebound in the USD and rates.

Nevertheless, the economic and inflation trends suggest that pressure should still be in favor of further gains in the USD and USA rates. The market is pricing in a hike on 15 March, but beyond that it is still not projecting even two more full hikes this year.

It still appears to be the case that the USD and rates market are building in more risk of a set-back in the growth outlook, while the equity market is building in upside risk.