New Zealand GDP post-mortem – NZD still vulnerable

Q2 was a good quarter after a lacklustre three quarters. Government spending is starting to kick in and may help support the economy, but business activity and consumer confidence surveys suggest growth will sag through the rest of the year. The RBNZ is likely to retain a neutral policy message in its statement next week, waiting for clearer evidence on the economy from Q3 labour and inflation reports. The ANZ business activity survey next week may be important for near-term sentiment. NZD gathered momentum from the GDP report and a broad rebound in global assets. The market continues to seek a big-picture top in the USD, but rising US inflation and tariff policy remain key supports for the USD.

New Zealand GDP Post Mortem

The New Zealand GDP report helped spark a further rebound in the NZD, one of the leading gainers (over +1.0%) in the major developed currency space on Thursday, although the gains in EUR and GBP are not far behind.

While the GDP data suggest that the economy is running fast enough for the RBNZ to retain its forecast that rates have bottomed, albeit likely to remain steady at 1.75% for some time, we are not convinced. The business and consumer survey data suggest that growth will be weaker in the second half of the year; keeping average growth over the year below potential.

New Zealand reports headline GDP on a production basis (in contrast to most other nations that focus on expenditure-based GDP).

The production-based GDP rose 1.0%q/q and 2.8%y/y in Q2-2018, above 2.5% expected. On a year-ended basis, the result is still below the RBNZ’s perceived potential growth rate of 3.1%.

The expenditure based GDP rose 1.2%q/q and 3.0%y/y. Using either measure it was a strong quarter after a lacklustre three quarters.

Private consumption rose in-line with overall GDP, up 1.0%q/q and 3.0%y/y.

Government spending is helping drive the economy; Government consumption rose 2.2%q/q and 5.6%y/y, Government capital investment rose 9.1%q/q and 6.3%q/q. It appears that the government’s fiscal expansion has started to kick in, and this might continue to be a bright spot for growth in the next year.

Private sector capital investment took a break in the quarter (-0.3%q/q) but is up solidly over the year (+3.9%y/y).

Total capital investment fell 0.1%q/q and rose 4.5%y/y. Residential (0.5%q/q; 3.0%y/y) Non-residential (-0.2%q/q; 5.1%y/y).

External trade was a boost in the quarter (exports +2.4%q/q, imports -1.5%q/q), but was a drag over the year (exports +3.3%y/y, imports -8.9%y/y). Gross National Expenditure (GDP excluding external trade) rose 4.6%y/y; suggesting domestic demand has risen faster than potential growth over the last year.

On the production-based measure, growth was supported by broad-based growth in the service sector, which accounts for over 70% of the economy, up 1.0%q/q and 3.3%y/y. The goods sector rose 0.9%q/q and 2.4%y/y. Primary industries rose 0.2%q/q and fell 1.7%y/y.

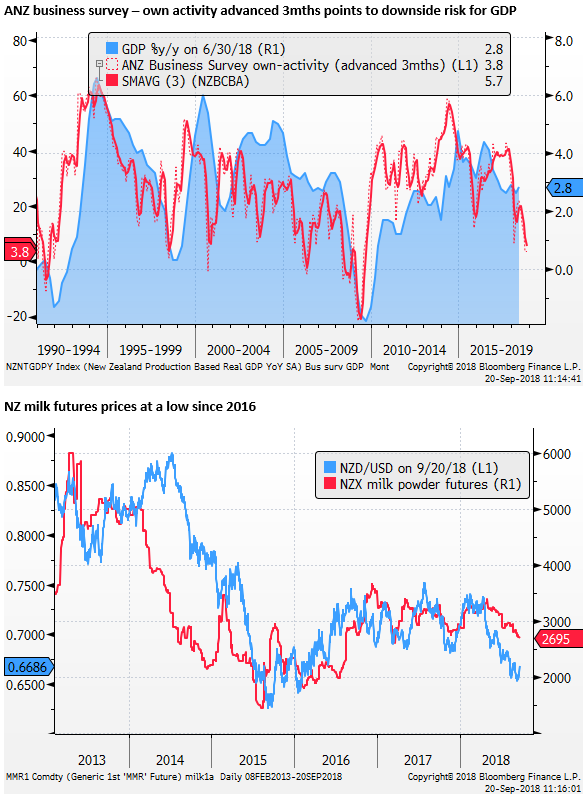

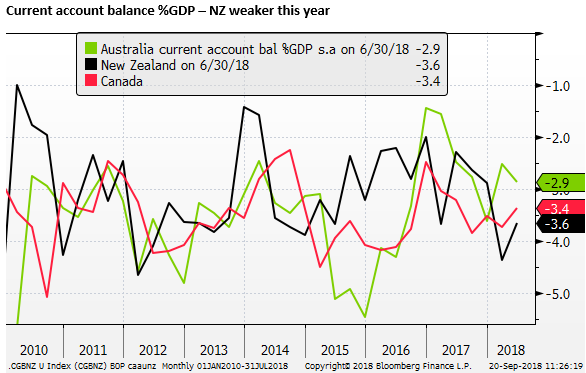

We would be looking to fade the strength in the NZD with recent business and consumer surveys pointing to a weaker growth outlook. And dairy prices weaker over the last six months; as we discussed in our report earlier this week (Risks for AUD and NZD coming to the surface; 19 sep – AmpGFXcapital.com)

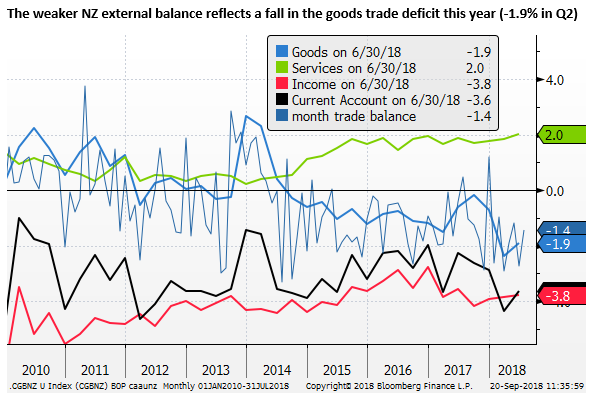

Another negative consideration for the NZD is a deterioration in its external balance in the last few quarters to around its lows since 2012 (-3.6% current account deficit in Q2), falling behind Australia (-2.9%).

NZ business survey and RBNZ statement

Important for the near-term direction for the NZD may be the next monthly ANZ business survey out on Wednesday next week. If it continues to languish near recent lows, fears for a weaker economy in the second half should build. On the other hand, a rebound in the survey might contribute to a further squeeze of short NZD positions.

The RBNZ policy statement on Thursday next week will be closely watched for clues on the policy outlook. However, this statement comes between the quarterly MPS, and we suspect the RBNZ will leave the key messages in their statement unchanged at this stage, waiting for clearer evidence from key reports such as the Q3 labour market and inflation reports.

Conflicted USD

The difficulty at this time is finding the right currency against which to sell the NZD. The broad correction lower in the USD in recent days in the context of a rebound in global asset markets may extend in the near term, and NZD/USD is a long for the ride.

We are conflicted on our view on the USD at this time. We continue to see rising inflation pressure in the US pushing up US rates. And US trade policy towards China continues to escalate. Both of these factors may return before long to undermine global asset markets and boost the USD.

But the USD has been rather choppy in recent years, despite persistent rate rises. The market appears to be constantly looking for the peak in US rates, and worrying about long-term structural problems; including twin deficits. As we discussed in our report: Short-term USD up-cycle clashes with approaching long-term down-cycle; 29 August – AmpGFXcapital.com.

If the USD is not best option to buy against the NZD, others we have considered are SEK and CAD where rate hikes are expected relatively soon. However, SEK seems far removed from NZD, and it has rallied significantly in recent weeks as rate hike expectation build. At this stage, the Riksbank is still sending mixed messages, and core inflation is not clearly rising. NAFTA negotiations are still in the balance for CAD. Inflation and retail sales on Friday are a near-term risk for CAD.

EUR is on the move, breaking above its recent range. Risk-metrics in Europe have improved as emerging markets recover, European equities rally and Italian bonds recover on expectations that the Italian government will keep its budget inside EU guidelines. However, the European economy has not recovered as much as expected and inflation remains subdued. GBP remains highly uncertain as Brexit negotiations remain fraught.

JPY might benefit from a strengthening Japanese economy, strong Japanese company profitability, the reduced political risk with Abe retaining his LDP leadership. However, JPY tends to be weak in a ‘risk-on’ market, although its correlation to risk-on metrics has weakened in the last year.

AUD/NZD also looks relatively good value against yield and commodity price spreads. If tariff risks remain on the back-burner and housing market and political risks in Australia do not flare up, the AUD might out-perform the NZD in the near-term.