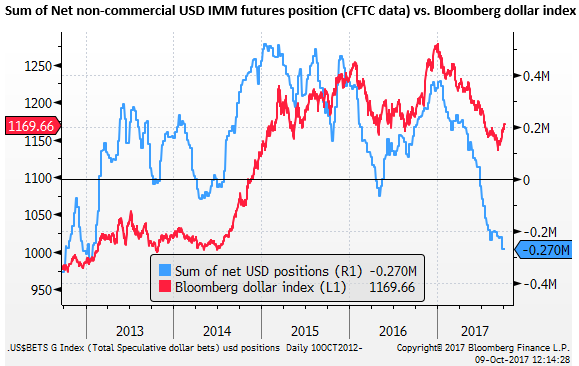

Skeptical market is very short US dollars

Surprisingly, futures positioning in the USD moved to a new high in net shorts on 3-Oct, despite the rebound in the USD over the last month. It seems the market is sceptical that the recent rise in the USD will last, and has been in a ‘sell-the-rally’ frame of mind. However, the rise in the USD has been consistent with a higher short and long-term yield advantage. US economic reports, including the labor data on Friday, support the notion that the USD can rise further. The USD has rallied in part due to a rejuvenated push for tax reform. However, it appears that the market retains a significant risk premium (discounting the USD) to account for US political uncertainty.

Market sold into the USD rebound

Positioning in the IMM FX futures market became more net short USD, measured on Tuesday last week, which is interesting in light of the renewed push for tax reform in the USA and a stronger USD trend in the last month.

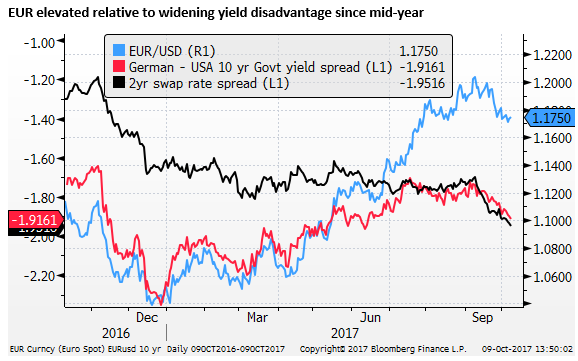

Net long EUR positions remain near their high; yet to show any major reaction to the weaker EUR in recent weeks or the increased political risk associated with the Spanish separatist threats.

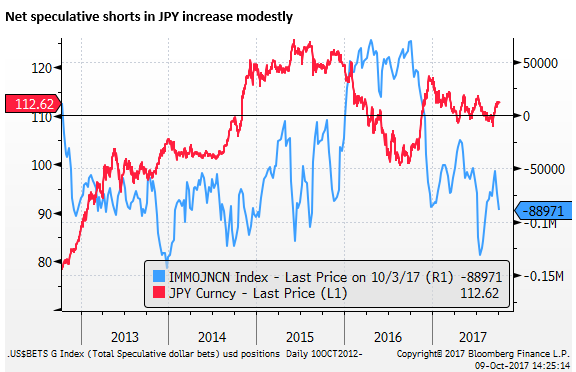

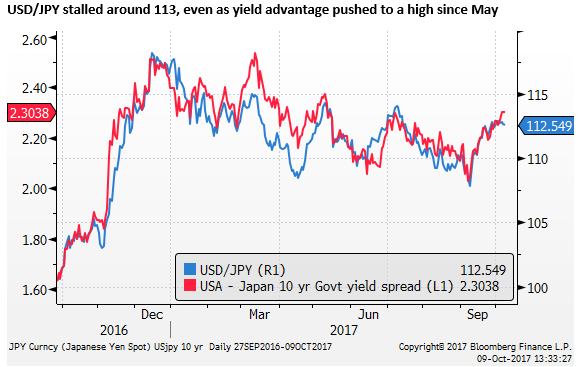

One currency where the market did express some increased confidence in the USD was against the JPY. The IMM market is net short JPY, and this short position increased in the week to 3-October, perhaps in reaction to some increase in US yields. However, the increase in net shorts was relatively modest, and the total net short position is less than its recent peak in late-July.

USD/JPY upside momentum has been muted, perhaps keeping traders from building larger net JPY shorts. NKorea geopolitical risk appeared to knock USD/JPY off its highs last week after the stronger than expected US labor report.

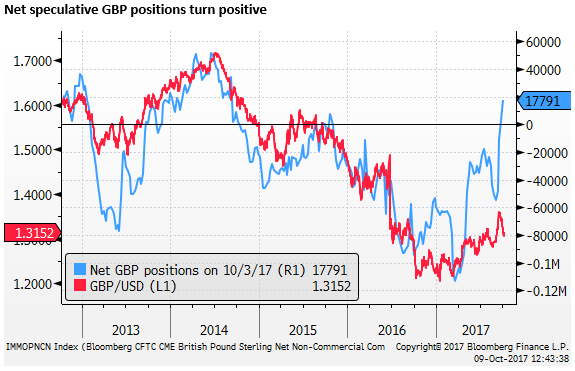

Positions in GBP have moved from a large net short (at a peak in March this year) to a small net long position in the last two weeks to 3 Oct. The shift to a tightening bias by the BoE in early-Sep and surge in GBP to a high for the year in mid-Sep generated GBP short-covering.

However it is interesting that IMM traders increased their net long GBP positions, even as it fell in the last week; their first inclination was to buy the dip, perhaps feeling caught under-weight GBP as a rate hike appears likely on 2 November.

GBP volatility increased after 3-Oct, falling sharply throughout last week on increased political uncertainty in the UK; in particular on speculation that PM May’s position as Tory party leader may soon be challenged. However, it has bounced sharply on Monday, continuing to be buffeted by political uncertainty and the prospect of a rate hike soon.

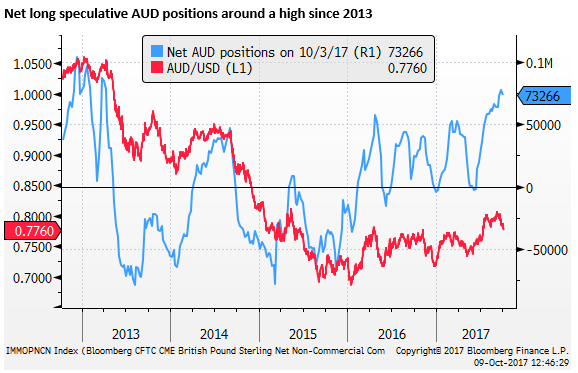

The net long position in the AUD eased a bit last week, but only after making a new high since 2013 a week earlier on 26-Sep. The AUD has been falling, in line with a stronger USD since early-Sep, and the first inclination of the market through September was to use the modest retreat in the AUD to build a longer net AUD position.

Sentiment towards the AUD may have deteriorated last week, after the 3-Oct position report, in response to much weaker than expected Australian retail sales, released on 5-Oct.

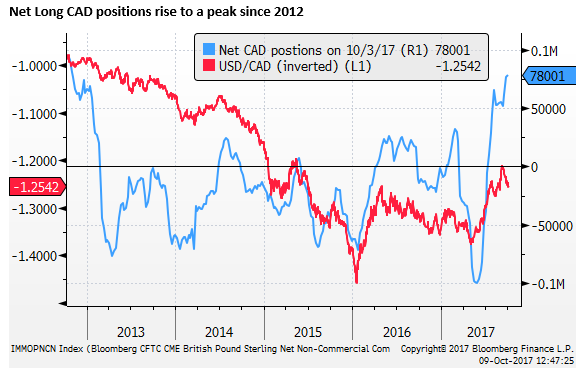

Net long positions in the CAD climbed a little further to a new high on 3-Oct since 2012. Like the AUD and GBP, the market’s first inclination during a period of weakness in the CAD since early-Sep was to build a longer net position in CAD.

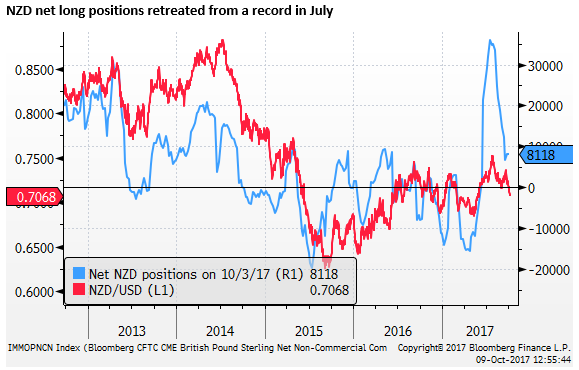

Positioning in the NZD has been quite volatile this year, rising to a record net long position in July, falling to a more modest net long position, more in-line with its range over the last few years.

Political uncertainty is heightened in New Zealand. After waiting for the delayed return of special votes for the 23 September election, the market is now awaiting coalition talks to see who will form the next government.

NZ first, a populist party that wants to restrict foreign ownership of NZ property holds the balance of power and will decide whether the next government will be the Labour/Greens, left side of politics, led by Ardern, or the incumbent Nationals, right side of politics, led by English.

Overall, the market, so far, is not buying the recovery in the USD in the last month. It is treating it as a correction in the USD downtrend, anticipating that the USD will soon resume its fall. There appears to be a large degree of scepticism in the potential for an upside surprise in the US economy that might result from tax reform. Or an additional boost to the USD that might arise from a tax break for US companies to repatriate their large stockpile of retained earnings from offshore operations.

(Trump tax plan is a big dollar booster; 29 Sep – ampGFXcapital.com)

The market appears more confident in the sustainability in the rising trend in the EUR, CAD and a range of other currencies, including many emerging market currencies. And is seeing more upside risk for the GBP.

USD underperforming its improving yield advantage

The lack of confidence in the USD recovery is at odds with the recent rise in US short and longer term yields relative to other major economies, improving the USD yield advantage. The market has moved to price in an 80% probability of a 25bp hike in the December FOMC meeting.

The market remains skeptical over the pace of USA hikes next year, with only two rate hikes (50bp) priced into the curve between now and the end of next year. Nevertheless, 2yr swap rates have crept to a new high in recent weeks, whereas rates have been stagnant or falling in other major countries.

US rates have bounced sharply from their recent lows on 8-Sep when hurricane uncertainty, NKorea geopolitical risks, and low US inflation data were depressing yields.

The EUR is out-performing its widening yield disadvantage. This is especially true at the short end (2yr swap rates). And it is also true for the long end since July (10-year German-US government yields).

USD/JPY has been closely aligned with the 10-year government yield spread this year. But even here there is a hint of divergence in the last week, with the US yield advantage rising to a high since May. But the gains in the USD stalling out around 113 in recent weeks. The market may be building in a bit more risk of a flare-up in the NKorea related geopolitical risk.

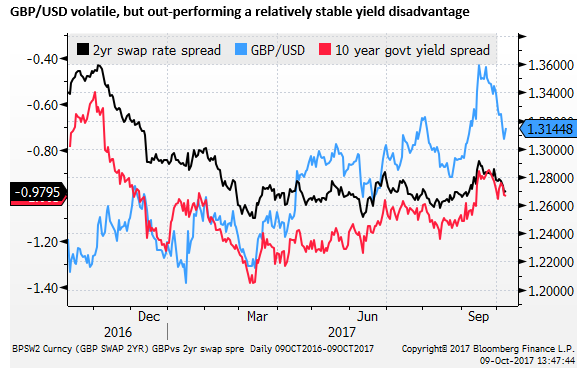

The political risk associated with Brexit and the gyrating fortunes of PM May as Tory leader have been buffeting the GBP for some time. Speculation over a possible rate hike by the BoE has also caused some gyrations. Since early-Sep, and especially following the 14 Sep BoE policy meeting, the probability of a rate hike at the 2-November has risen to 77%. Nevertheless, the GBP/USD has tended to out-perform a relatively stable US-UK 2yr swap rate spread.

Its gains are more consistent with a narrowing in the 10-year government yield spread. However, it appears that despite the ongoing and substantial uncertainty in UK politics and Brexit, the political risk premium in the UK has eased relative to that in the USA.

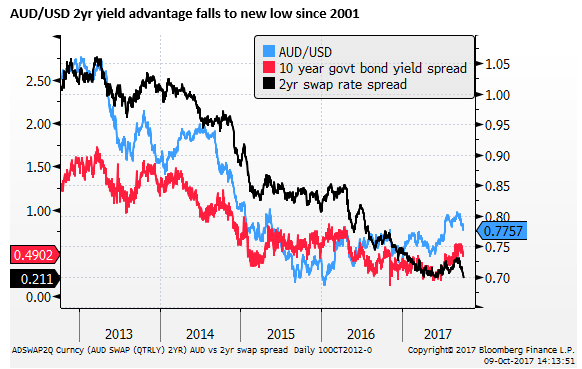

The AUD 2yr swap rate spread has fallen to a new low since 2001, falling sharply since mid-Sep. Australian rates rose tepidly along with higher rates in the UK, Canada and the US in early-Sep. But this petered out after the RBA Governor reiterated a largely neutral policy outlook on 20-Sep, and recent data, including a weak retail sales figure last week, further dampened hope of an RBA rate hike anytime soon.

The AUD has fallen since early-Sep, but remains higher than might be consistent with short-term yields. The long-end spread has been more supportive of the AUD.

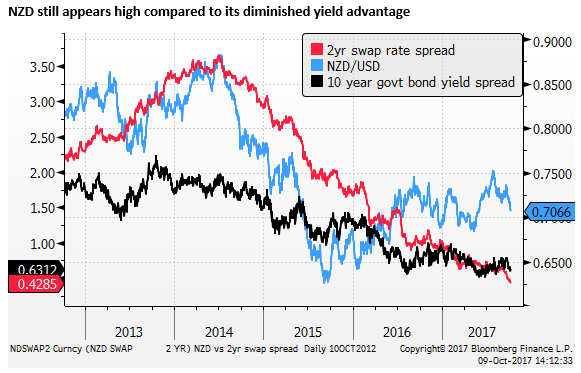

The NZD was surprisingly strong in July, despite little change in its yield advantage that was around its lows since 2001. It appeared to reflect strength in emerging market assets. In August and leading up to the national election on 23 Sep, The NZD appeared to pay more attention to its political risk that has resulted in a hung parliament.

Like Australia, New Zealand rates have failed to follow the uptrend in US, UK and Canadian rates, resulting in a further significant narrowing in its 2yr swap rate advantage to a new lows since 2001. The fall in the NZD over the last two weeks appears more consistent with this narrowing. But its relationship to rates has been very inconsistent over recent years, and the NZD remains well above its historical average, well above levels consistent with its diminished yield advantage.

Political risk in the USA remains high, due to the erratic tweets from Trump that continually lurch back to antagonizing NKorea and his Alt-right agenda, threatening to distract Congress from tax reform.

However, economic data, including the sharp fall in unemployment and underemployment to around long-term cyclical lows, and evidence of creeping wage growth is supporting the case for higher US rates. The recent ISM reports were very strong. And while they are to some extent boosted by hurricane disruption, they still point to stronger economic activity and higher inflation in coming months.

The dollar has made a habit of year-end rallies; 4 Oct – ampGFXcapital.com

Rates are firming in the US, and may well rise further, with only two hikes between now and the end of next year in the yield curve.

There is also upside risk to rates in the near term related to the choice of the next Fed chair. The Administration appears to be looking for a Fed Chair that will be amenable to easing financial regulation. These candidates are also those that are likely to pursue faster policy normalization. We see Kevin Warsh as the most likely pick for Fed Chair.

The significant net short USD positions suggest that there is more risk of gains in the USD, on short covering, as the market pays more attention to an improving USD yield advantage.